Introduction

NS Partners is pleased to share its fifth annual Responsible Investing (RI) Update, which highlights progress and initiatives from RI efforts over the last year. This report includes features of the firm’s stewardship, engagement and integration activities as they relate to financially material environmental, social and governance (ESG) issues.

As a global asset manager, NS Partners takes its fiduciary responsibility seriously, demonstrated through its fundamental stock selection and comprehensive RI approach. NS Partners believes that ESG factors can have a material impact on investment performance and present unique risks and opportunities for investee companies. As such, ESG factors that are financially material are considered, along with traditional financial factors, as part of the firm’s bottom-up research and stock selection approach.

The evolution of RI at NS Partners

Since inception, NS Partners has considered material ESG factors in its investment process. NS Partners became a signatory to the United Nations Principles for Responsible Investing (PRI) in 2016 and has since developed an RI Policy that aligns with its commitment. NS Partners continues to look for ways to enhance the risk-adjusted returns for its clients, while further developing its approach to integrating material ESG factors in its investment process.

Evolution of NS Partners’ approach to responsible investing

* Task Force on Climate-Related Financial Disclosures.

As of September 2025. Chart is for illustrative purposes only and is not drawn to scale.

Source: NS Partners Ltd

ESG integration in the investment process

By ensuring that financially material ESG factors and their trajectory over time are captured in the investment process, the firm’s policy on RI aligns with the duty to seek the best returns for clients.

Industry Collaboration

NS Partners participates in collaborative engagements and initiatives to pool resources and speak with a stronger unified voice to protect the interests of shareholders in the companies in which it invests on behalf of its clients.

![]()

NS Partners is a supporter of the Task Force on Climate-Related Financial Disclosures (TCFD)* recommendations. In May 2025, NS Partners published its inaugural TCFD-aligned disclosure outlining the firm’s approach to identifying, assessing and managing climate-related risks in its investment process.

*The TCFD disbanded in 2023, having been incorporated into the IFRS’s ISSB standards.

![]()

Since 2020, NS Partners has been a member of Climate Action 100+, an investor initiative to engage the world’s largest corporate greenhouse gas emitters on their action on climate change. As part of this initiative, NS Partners continues to participate in the collaborative engagement with Lockheed Martin Inc.

![]()

NS Partners is a supporter of the International Corporate Governance Network (ICGN) through its affiliation with member Connor, Clark & Lunn Financial Group (CC&L Financial Group).

![]()

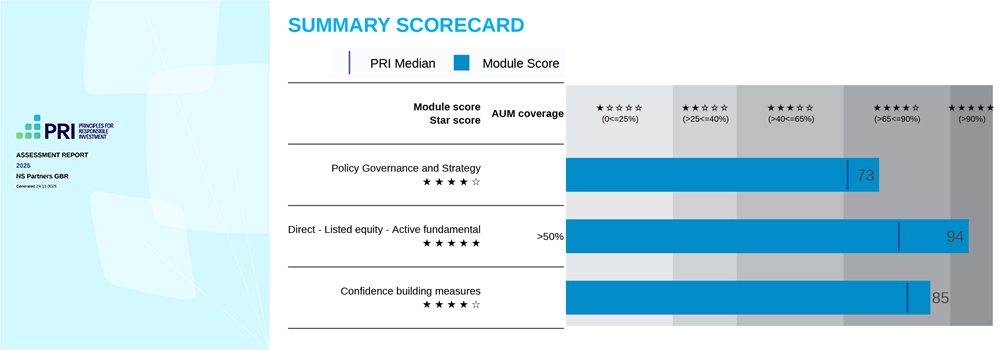

In February 2016, NS Partners became a signatory to the PRI initiative. As signatories, NS Partners has committed to adhering to the six principles and to transparent reporting on its ESG activities in accordance with the PRI reporting framework.

NS Partners is pleased to share its 2025 PRI Assessment Summary Scorecard, which reflects the progress made in its ESG activities. NS Partners is ranked at or above the median in all measurement categories, and improved on the Policy Governance and Strategy module score from 2024.

Source: PRI Association

*The Assessed Modules provided are based on the UN PRI scoring methodology for the 2025 Reporting Framework. The PRI Reporting Framework is based on responses provided by signatories for the preceding calendar year which are captured in their PRI Transparency Report. NS Partners’ PRI Transparency Reports are available at unpri.org. NS Partners’ 2025 PRI Assessment Report is available on request. More information on the 2025 reporting period is available here.

Climate change

Carbon footprint report – Sustainable Global Emerging Markets (GEM) Fund

As supporters of the TCFD, NS Partners is committed to measuring and disclosing the carbon footprints of its core funds.

In addition to NS Partners’ ESG integration process, the Sustainable GEM Fund excludes companies that derive a meaningful portion of revenue from fossil fuel investments, among other screens for issuers with high externalities or social costs. The Sustainable GEM Fund has outperformed the benchmark in terms of its carbon intensity and weighted average carbon intensity (WACI). While the carbon footprint of the portfolio is an outcome of its investment process, it is not specifically targeted. NS Partners believes its investments in high-quality issuers and industry leaders has contributed to its lower carbon footprint relative to the benchmark.

Figure 1: Sustainable GEM Portfolio vs Benchmark Carbon Intensity

Source: ISS for the reporting period 01 October 2024 – 30 September 2025, in USD.

In addition to the fund’s overall lower carbon footprint, the Sustainable GEM Fund has seen lower emissions versus the benchmark in most industry sectors. This is shown in figure 2 below by the positive issuer selection effect, particularly in the energy sector, and across most sectors in Q3 2025. Similar positive selection effects across most sectors were also seen over the previous three quarters.

Figure 2: Sustainable GEM portfolio issuers selection effect by sector

Source: ISS as of 30 September 2025, in USD.

Proxy voting

Over the past year, the Sustainable GEM Fund voted at 104 company meetings, voting against management on 10% of the proposals NS Partners was eligible to vote on.

Proxy Voting Highlights

104

number of meetings

869

proposals voted

10%

votes against management

20

countries voted

Figure 3: Total proxy votes – Sustainable Global Emerging Markets

Total

Proxy Votes

869

Proxy Votes

869

Source: ISS for the reporting period 01 October 2024 to 30 September 2025.

Table 1 – Votes against management and ISS by proposal category

Source: ISS for the reporting period 01 October 2024 to 30 September 2025.

*Votes against ISS indicate where NS Partners’ custom voting policy deviated from ISS’ benchmark voting policy.

Figure 4: Votes against management by category

Source: ISS for the reporting period 01 October 2024 to 30 September 2025.

Proxy Voting examples

Bangkok Dusit Medical Services Public Co. Ltd.

In April 2025, NS Partners voted against management on several director election proposals at the annual meeting of Bangkok Dusit Medical Services, a Thai private health-care group. There were various governance concerns related to the composition of the board including several non-independent nominees and the board being composed of less than 50% independent directors. Additionally, NS Partner voted against the election of the chair of the board given further concerns on board composition, particularly over an executive director’s suitability to serve on the board due to past financial misconduct at another company, putting shareholders at risk.

Hexaware Technologies Limited

NS Partners voted against several compensation-related proposals at the 2025 annual meeting of Hexaware Technologies, an India-based IT service company. There were concerns over the company’s proposed discounted stock option plans which risk the alignment of interests between the company’s employees and shareholders. Additionally, the company had not provided adequate disclosure of vesting conditions, nor disclosed performance metrics, targets and weights of performance metrics. The absence of such compensation-related information would make it difficult for shareholders to assess the potential linkage between pay and performance.

Industrial and Commercial Bank of China Limited

In June 2025, NS Partners voted against management on various director-related proposals at the annual meeting of the Industrial and Commercial Bank of China. Management’s proposed amendments to the company’s Articles and Board Rules, including changes to provisions concerning the bank’s Party Committee, were deemed insufficient in ensuring accountability and transparency for shareholders. The proposed changes could introduce significant governance risks by compromising the independence and objectivity of the board – specifically, granting the Party Committee legitimate authority which may enable undue influence over the board and its key committees.

Engagement examples

SK Square Co., Ltd.

NS Partners engaged with SK Square, a Korean asset manager specialising in high-tech growth sectors, by sending an engagement letter requesting the company to meet certain considerations, such as refreshing management KPIs to pursue a narrower discount, prioritise share buybacks and increasing and committing to a progressive dividend. While NS Partners commended the company on management’s ambitious targets and delivery of value-enhancing initiatives ahead of schedule, NS Partners also expressed that this engagement is just the beginning of a sustained push to maximise value creation for all shareholders. NS Partners outlined that it looks forward to working with the Board to sharpen targets and sequencing, and also a refreshed value-up plan and additional details at the company’s upcoming annual meeting.

Tencent Music Entertainment Group

NS Partners met with Tencent Music, a music entertainment platform, in Shenzhen, China in late 2025. During the meeting, NS Partners requested that the company increase the share buyback. The company explained that the cash is required for future investment as they are building a Live Nation-like business, focussing on offline concerts, creating a stronger ecosystem for users. The company was receptive to the shareholders’ request and mentioned that they will provide an update in the near-term.

Governance summary

As advocates for good corporate governance, NS Partners continues to monitor various governance metrics and performance of investee companies. Below is a look at the progression in female representation on boards, average board independence and the proportion of companies with separate CEO and chair roles.

During the reporting period, director independence and separate chair and CEO on boards of companies and saw progression, while average female representation slightly decreased in the Sustainable GEM Fund.

Figure 5: Board statistics over time

*Source: MSCI as of 30 September 2025 in USD.

MSCI ESG ratings

An analysis of our Sustainable GEM Portfolio based on MSCI ESG ratings suggests scoring across all rating categories is better than its respective benchmark. In addition, the proportion of “ESG Leaders” in our representative portfolio is higher than that of its respective benchmark.

Figure 6: Weighted average ESG score

Source: MSCI as of 30 September 2025 in USD.

Figure 7: ESG ratings distribution

Source: MSCI as of 30 September 2025 in USD.

Corporate Social Responsibility

CC&L Financial Group is committed to being a responsible corporate citizen and strives to have a positive impact on the communities where its employees live and work. Its business practices should consider the impact on the workplace, community and society. In addition, through Connor, Clark & Lunn Foundation (CC&L Foundation), there is a focus on philanthropic and volunteering initiatives. Below is a summary of some of the initiatives undertaken by CC&L Financial Group over the last 12 months.

Culture of inclusion at CC&L Financial Group

To ensure employees feel a sense of belonging, the firms strives to foster a culture that unites people of diverse backgrounds and perspectives, in an environment where everyone has the opportunity to achieve personal and professional success. Over the last 12 months, CC&L Financial Group focused on education, communications and events to promote a culture of inclusion, celebration and learning throughout the year. Some examples include:

- Observed and celebrated Black History Month, Lunar New Year, International Women’s Day, LGBTQ2S+ Pride Month and National Day for Truth and Reconciliation.

- Promoted the 4 Seasons of Reconciliation Course across the company. This course describes the foundation of the relationship between Canada and Indigenous peoples and promotes a renewed relationship through education.

- Communicated and encouraged voluntary participation in the demographic data collection project. About 50% of employees across CC&L Financial Group have completed the survey.

- Updated employee engagement survey to begin linking employee data while ensuring anonymity of responses. This approach will increase the ability to evaluate how different groups see their work experience with the firm.

Environmental stewardship at CC&L Financial Group

CC&L Financial Group believes that actions contribute to the vitality of the environment, and is committed to undertaking initiatives that support ongoing environmental stewardship. Over the last 12 months, the Environmental Stewardship Committee has focused on the following initiatives:

- Continued to measure and monitor the GHG emissions generated through our business activities.

- Continued to monitor developments around collaborative initiatives.

- Provided education regarding the sustainability practices of our major travel partners so that individuals can consider this information in making travel choices.

- Provided education on low-emission commuting solutions and centralised information on office service amenities to create awareness of environmentally friendly options.

- Delivered events and communication circulars to promote a culture of environmental consciousness such as the Earth Month Personal Carbon Footprint Faceoff and Bike-to-Work Week.

- Continued to develop a paper waste reduction strategy relating to trade confirmation receipts and other materials provided by third-party partners and vendors.

Health and Wellness at CC&L Financial Group

CC&L Financial Group believes the health and well-being of the people who work at the firm is critical to maintaining collective performance. The firm is committed to undertaking initiatives that support a safe and healthy work environment within a culture where everyone feels secure and supported. The Health & Wellness committee focused on the following initiatives over the last 12 months:

- Hosted Health and Wellness Month, which included workshops on topics such as “the power of embracing failure” and “the benefits of meditation.” In addition, a company-wide fitness challenge was held where participants collectively took over 23 million steps to travel 16,895 kilometres. This challenge was a fantastic way to motivate employees to get active.

- Launched CC&L Financial Group’s inaugural Canada-wide participation in the Terry Fox Run, with over 100 enthusiastic participants. Thanks to participant efforts, over $31,000 was raised for cancer research, including generous donation matching from CC&L Foundation.

- Promoted Mental Health Month, by learning from experts about ways to manage stress, talk about mental health and be present in your body to connect mental and physical health through a variety of in-person and virtual workshops.

- Supported several employee-led health and wellness activities, including teams of participants in the Bay Street Hoops charity basketball tournament as well as the Ontario Ride to Conquer Cancer.

Connor, Clark & Lunn Foundation

CC&L Financial Group aims to enrich the communities in which its employees live and work by creating opportunities for both philanthropy and volunteerism through CC&L Financial Group and its affiliates in support of causes that are important to clients, employees, partners and stakeholders. CC&L Foundation provides support to a broad range of organizations that focus on promoting a better environment, improving education, advancing science and medicine, creating stronger communities and encouraging the arts. Over the last 12 months, CC&L Foundation supported a broad range of philanthropic and volunteer opportunities, some of which are highlighted below:

- Participated in The Grand Défi Pierre Lavoie 1000 km team cycling event in Quebec, a fundraising initiative that aims to promote healthy life habits among young people and to support research on orphan hereditary diseases.

- Provided support through the Canadian Red Cross and the Jasper Community Team Society to those impacted during the Alberta wildfires.

- Organized an employee-led Week of Giving campaign focused on strengthening communities, alleviating poverty and addressing food insecurity. This initiative supported CC&L Financial Group’s community partners, including the United Way. This firm-wide initiative has raised almost $8 million over 20+ years.

- Made a multi-year commitment to BC Children’s Hospital Foundation and its Heart Centre program to purchase essential medical equipment to support children across the province who face serious injuries and illnesses.

- Participated in the CanSupport Dragon Boat Race to raise awareness and funds for the Cedars Cancer Foundation to improve the quality of life of cancer patients and support fundamental research initiatives.

- Aided students through bursaries and scholarships, including Concordia University and Carleton University’s Women in Finance programs, Indspire’s Building Brighter Futures program, the National Educational Association of Disabled Students and the Onion Lake Education Trust Fund.

- Held an internal fundraiser to support inclusivity and allyship during Pride Month, with donations directed to Rainbow Railroad.

- Participated in a Canada-wide blood drive campaign in partnership with Canadian Blood Services.

- Provided support to the United Way British Columbia Kapwa Strong Fund, created to provide immediate and long-term support to those directly impacted by the tragic events at the Lapu Lapu Day Festival on April 26, 2025.

For additional information on NS Partners Ltd, please contact:

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)

Jean-Philippe Lemay

Managing Director,

Head of Institutional Sales, Global

Eric Hasenauer

Senior Vice President,

Co-Head of Institutional Sales, USA

John Ricketts

Senior Vice President,

Co-Head of Institutional Sales, USA

Please take the time to carefully read the following as it contains important information regarding certain restrictions imposed by statute and the applicable securities regulatory authorities on the distribution of information through this website.

Material presented on this website should be considered for background information only and should not be construed as investment or financial advice. Further, information on this website should not be construed as an offer or solicitation by the Connor, Clark & Lunn group of companies to provide investment management services or to buy or sell any products.

The NS Parters Ltd. (NS Partners) website may contain hyperlinks to websites operated by parties other than NS Partners. Such hyperlinks are provided for your reference only. NS Partners does not control such websites and is not responsible for their contents. The inclusion by NS Partners of hyperlinks to other websites does not imply any approval or endorsement of the material on such websites or any association with their operators.

The Connor, Clark & Lunn group of companies includes a number of entities that may be registered as investment advisers, investment fund managers and exempt market dealers in various provinces and territories of Canada. A number of entities are also registered with the Unites States Securities and Exchange Commission as advisers in that country and the Connor, Clark & Lunn group of companies also includes a number of investment advisers and fund managers that are authorized and regulated by the Financial Conduct Authority in the United Kingdom. The information provided on this website regarding each entity is directed solely towards qualified investors in jurisdictions where the appropriate entity is registered. Services offered by any of the entities in the Connor, Clark & Lunn group of companies are offered solely to qualified residents of the jurisdictions where the entities are qualified to do business.

Certain securities regulations prohibit the publication of specific registration information about the registered entities in the Connor, Clark & Lunn group of companies. For more information, please contact the Connor, Clark & Lunn Compliance Department at [email protected] or 604-685-2020.

NS Partners Ltd.

December 14, 2023