Commentary

Warlordism undermines state power in Russia

July 13, 2023

Summary

- Improving politics and continued economic strength in Greece propelled strong returns, the market up nearly 10% in USD terms over the month.

- More cyclical markets caught a bid, boosting Brazilian and Chilean equities. Given the deterioration of money numbers globally, we are not tempted to chase rallies across materials and energy as the likelihood of a sharp recession increases.

- Indian stocks have been beneficiaries of reallocation by foreign investors abandoning China in recent months, with portfolio names across Industrials, Financials and Health Care posting modest gains. The challenge in India, as ever, is weighing up India’s incredible development story with rich valuations. However, we know that relying on mean reversion tables can be a fraught exercise when structural change is occurring. An economy is not a zero-sum game, or a closed loop where everything must revert to the mean. India’s ascent up the development ladder will expand the domain of the economy, and often in ways that are underappreciated and underestimated by the market.

- Chinese equities were steady, capping off a poor quarter overall. We maintain a slight overweight in China, with positive money numbers continuing to support a modest recovery, low inflation, incredibly cheap real exchanges rates, and modest valuations for a host of high-quality businesses. However, more support from the authorities is needed to ensure weakness in the property sector does not feed into a vicious economic cycle that spills into other sectors.

Greek summer

Greek stocks continued their strong run into summer, boosted in June by the re-election of conservative leader Kyriakos Mitsotakis. The result vindicates the decision by Mitsotakis to call a snap election after his party fell short of a clear majority in April elections. His New Democracy party commands 40.5% of the national vote, almost 23 percentage points ahead of Alexis Tsipras’ Syriza party. The result marks an incredible turnaround from the brutal downturn of the European financial crisis, three IMF bailouts and painful economic restructuring, to Greek government bonds shedding junk status earlier this year, with the yield discount to Italian counterparts at its highest level since 1999. Further improvement to investment-grade status would unlock greater foreign investment, and lower borrowing costs for government and businesses. If Mitsotakis can deliver on campaign promises to boost salaries, lower taxes, restructure the healthcare system and upgrade Greece’s infrastructure, then the future is bright.

Thailand’s post-election limbo

Political risk following Thailand’s national elections appears to be rising, as uncertainty grows over whether the progressive Move Forward party will be allowed to form government despite its strong showing in recent national elections. The Thai electoral commission announced that it is investigating whether party leader Pita Limjaroenrat broke campaign rules through ownership of shares in a media company. The presidential candidate has denied any wrongdoing. However, the investigation may threaten the chances for Move Forward to garner enough support in Thailand’s unelected Senate (appointed under the previous conservative military-aligned government) to confirm a ruling coalition led by Pita. Failure to confirm the Move Forward coalition would represent a significant step backward for Thailand’s institutional quality and damage the trust of voters, and would limit the country’s development trajectory. It is likely that the post-election political wrangling and horse trading to form government has only just begun.

China’s authorities need to get creative to end the slump

Xi Jinping faces some monumental challenges both at home and abroad. High youth unemployment has the potential to become socially destabilising if it continues to worsen, and a renewed slump in property prices threatens to further dent the already brittle psyche of consumers and corporates. We agree that meaningful stimulus is needed to break consumers and corporates out of this coma. It needs to be a fiscal and/or monetary bazooka, and not the sniper shots we have seen over the past few months. The big question is whether this message is getting to the man at the top? Economic tsar Li Qiang has been talking up support for the private sector in recent months, and he is right to do so given it generates 95% of jobs in China. But this positive rhetoric does not appear to have been embraced by Xi, who has stuck to pledges of deleveraging at all costs, limiting policy options for dealing with China’s slump. Given Xi’s directive to avoid resorting to excessive leverage in property and infrastructure to boost the economy, authorities may need to get creative. If meaningful stimulus can charge the recovery, sentiment for Chinese equities will turn quickly.

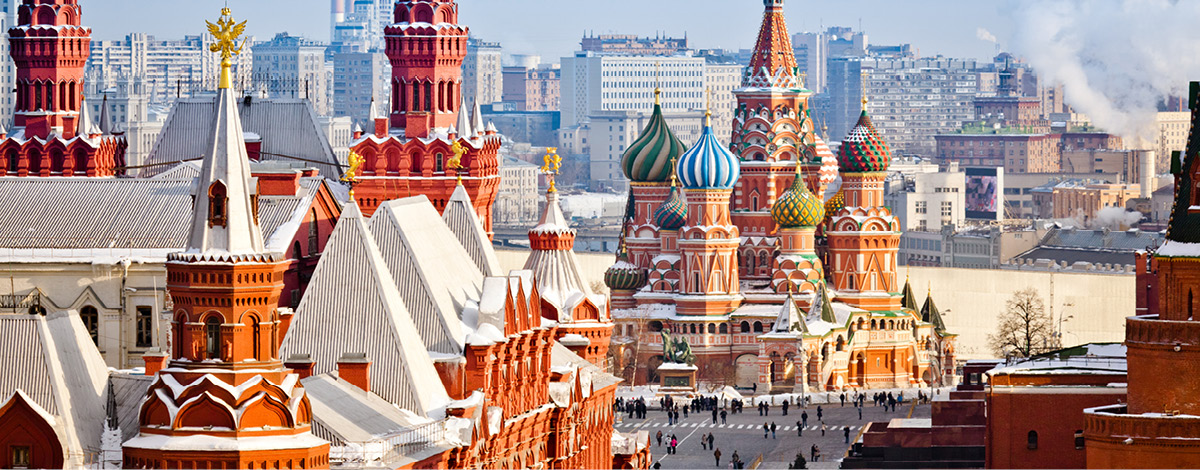

Warlordism undermines state power in Russia

Poor Sino-US relations and fears that China may seek to take Taiwan by force remain a headline risk for many EM investors. Last year we wrote that Russia’s botched invasion of Ukraine and the strength of the Western response painted a clear picture to Beijing of the risks associated with conflict and further deterioration of relations with the West. Yevgeny Prigozhin’s jolly through Russia with his band of Wagner mercenaries underlined this risk, as the mutineers moved virtually unopposed through Russia, taking the southern military command post in Rostov-on-Don and breezing through a series of supine military checkpoints as they barrelled towards Moscow. While the uprising was eventually put down thanks to the intervention of Putin’s Belarussian stooge president Lukashenko, it suggests that the government no longer commands a monopoly on violence in Russia. The risk is that this emboldens would-be usurpers in the Kremlin and secessionists in Russia’s vast periphery, risking the rise of warlordism reminiscent of Republican China. While the CCP has tightened its grip over the People’s Liberation Army under Xi, a high-risk amphibious assault on Taiwan inviting a US military response and harsh Western sanctions would place incredible pressure on state power structures at a time of economic fragility and high youth unemployment. Recent chaos in Russia reinforces our view that Russia’s invasion of Ukraine actually lowers the risk of China attempting to take Taiwan by force.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)