US banks signalling H2 credit crunch

The Fed’s July senior loan officer survey signals a major slowdown in US bank lending in H2 and 2023.

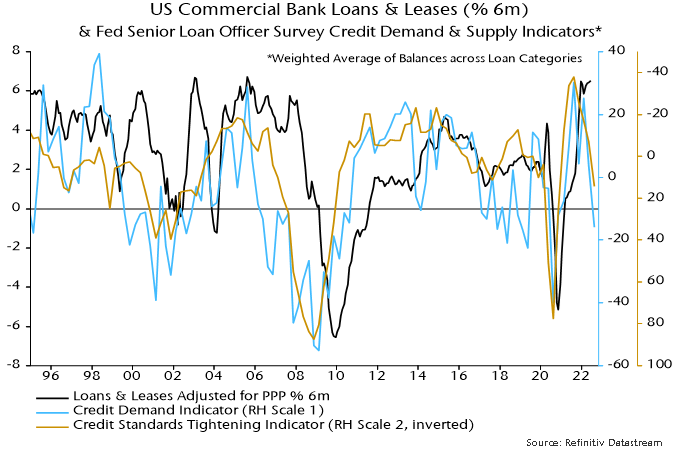

Most commentary focuses on survey responses about credit standards and demand for commercial and industrial (C&I) loans. However, the Fed calculates aggregate indicators incorporating data for all loan categories (i.e. also including commercial real estate (CRE), consumer and residential mortgages).

These indicators weakened sharply in Q2*, moving below their averages since 1995 – see chart 1.

Chart 1

Demand for residential mortgages weakened most, with smaller declines for CRE and consumer loans. C&I loan demand remained strong, driven by inventory financing (negative for economic prospects).

Credit tightening was across the board but most pronounced for CRE and C&I loans. Banks cited a less favourable economic outlook, industry-specific problems and reduced risk tolerance as key drivers of the tightening of C&I loan standards.

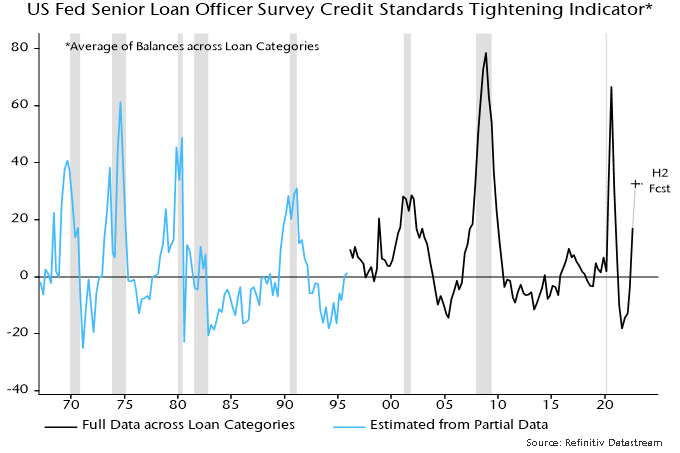

Is the degree of credit restriction consistent with a recession? The Fed’s aggregate credit tightening indicator combines data for the various loan categories using their weights in banks’ lending books. The indicator is unavailable before 1995 but similar results are obtained using a simple rather than weighted average, and this alternative indicator can be estimated for earlier years from partial data for the loan categories.

Chart 2 shows that this alternative indicator rose above 28% before or during seven of the last eight recessions, with no false positive signals. The single false negative was the double-dip recession of 1981-82, which was arguably an extension of the 1980 contraction rather than a separate cyclical event.

Chart 2

The indicator rose from -4% in the April survey to 17% in July, i.e. below the critical value. The current level was reached in 1968, 1978 and 1998 without an accompanying recession.

The July survey, however, included special questions about banks’ expectations for credit tightening for selected loan categories in H2. A net 52% expect to tighten standards on C&I loans, up from an actual 23% in Q2. Smaller but significant increases are signalled for consumer loans and residential mortgages. Assuming no change for CRE loans (which were not covered by the special questions), the aggregate alternative indicator in chart 2 is forecast to rise to 33%, i.e. above the 28% recession threshold.

*The survey cut-off date was 30 June.