Money Moves Markets

UK money trends arguing for MPC inaction

February 2, 2022 by Simon Ward

The “monetarist” view is that central banks should conduct policy with the aim of stabilising growth of (broad) money at a non-inflationary rate.

Major central banks – the Fed and Bank of England in particular – trashed this principle in 2020-21, pursuing policies that caused money growth to explode, with the inflationary consequences still playing out.

The MPC’s decision in November 2020 to launch a further £150 bn of QE when annual broad money growth – as measured by non-financial M4* – was already at 12% was one of the worst in its 25-year history.

So what is the monetarist policy recommendation now?

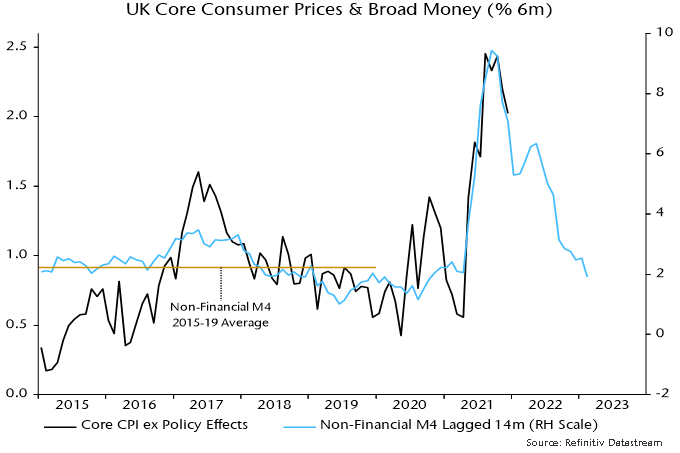

In the UK, it is to do nothing. Broad money momentum slowed sharply during 2021, with non-financial M4 rising by 1.9% or 3.9% at an annualised rate in the six months to December. This is close to the average in the five years preceding the pandemic and, if sustained, would be consistent with core CPI inflation returning to around target over the medium term – see chart 1.

Chart 1

The H2 broad money slowdown occurred despite QE continuing until November. Monthly growth of non-financial M4 fell to just 0.1% in December.

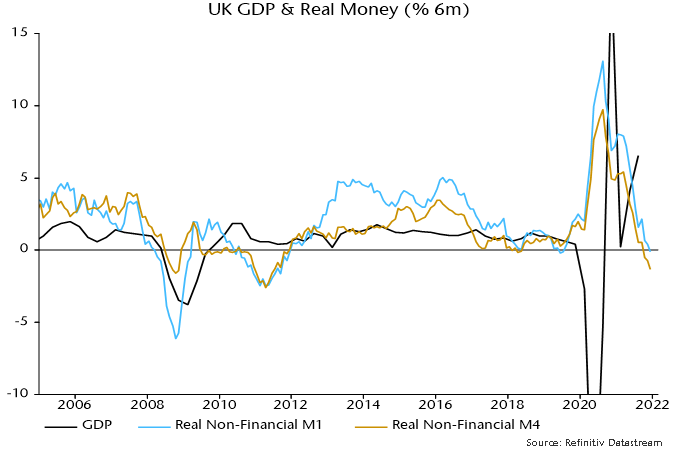

The combination of high inflation due to 2020-21 policy mistakes and the recent monetary slowdown has resulted in a contraction of real money balances, suggesting already-weak economic prospects – chart 2. Policy tightening into such a contraction risks pushing the economy into a recession.

Chart 2

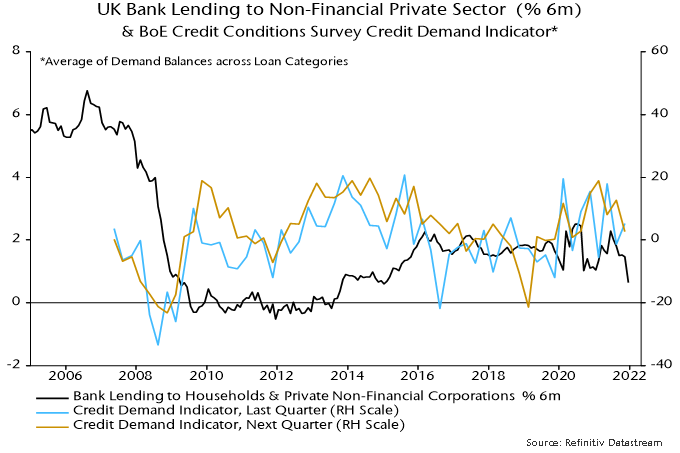

The MPC, on the view here, should wait for a rebound in money growth before raising rates and starting to reduce its gilts portfolio. Such a rebound is likely to depend on a pick-up in private sector credit growth, of which there is no sign in recent lending data or the Bank of England’s credit conditions survey – chart 3.

Chart 3

A consensus view is that the MPC needs to tighten to prevent high inflation becoming embedded in expectations. The best way of anchoring inflation expectations is to maintain low, stable money growth.

Another argument is that a period of weak money growth is warranted to offset excess expansion in 2020-21. Such attempts at monetary fine-tuning are hazardous and liable to create more volatility. The suspicion here is that “excess” money balances have already been largely absorbed by asset price / wealth gains (and an associated rise in the portfolio demand for money) and the current inflation surge.

*M4 holdings of the household sector and private non-financial corporations.