L’argent, le moteur des marchés

UK inflation: don’t panic

May 31, 2023 by Simon Ward

Market reaction to UK April CPI numbers focused on the overshoot of headline and core inflation relative to forecasts, ignoring a continued slowdown in headline price momentum.

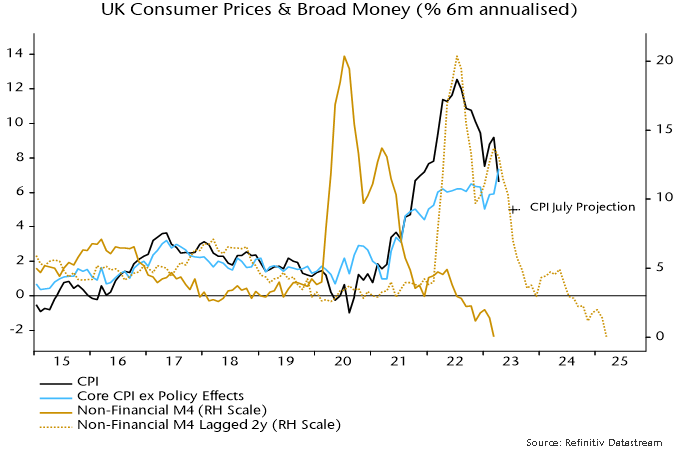

The six-month rate of increase of headline prices, seasonally adjusted here, fell to 6.6% annualised in April, the slowest since September 2021 and down from a peak 12.6% – see chart 1.

Chart 1

Six-month headline momentum is tracking a simplistic “monetarist” forecast that assumes a two-year lag from money to prices and the same “beta” of inflation to money growth as on the way up.

This forecast suggests a further decline in six-month momentum to about 5% annualised in July on the way to much lower levels in late 2023.

The projection of a fall to 5% or so in July is supported by a bottom-up analysis incorporating the announced 17% cut in the energy price cap that month.

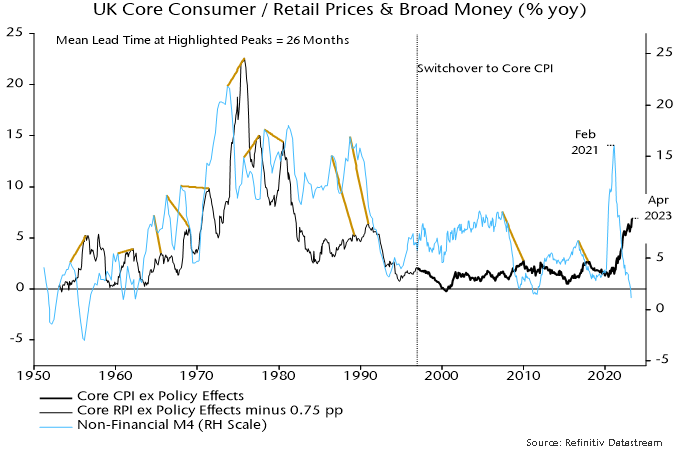

Markets were spooked by annual core inflation reaching a new high of 6.8% in April but it is normal for core to lag headline at turning points.

The April result, moreover, is consistent with a mean historical lag of 26 months between peaks in annual broad money growth and core inflation: money growth continued to rise into February 2021 – chart 2.

Chart 2

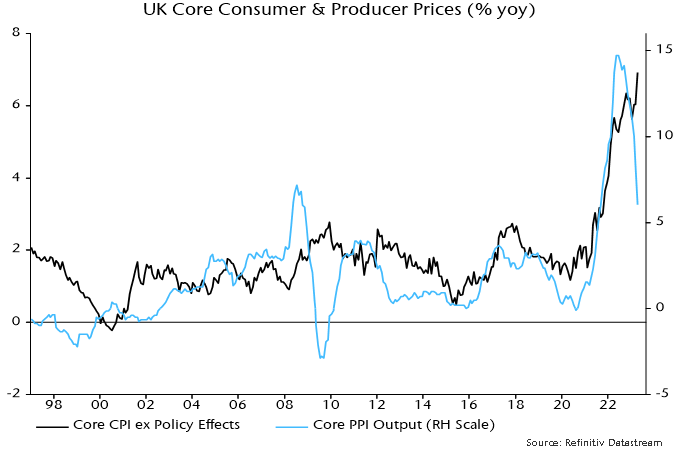

The suggestion that core inflation is at or close to a peak is supported by PPI data: core PPI output inflation usually leads and has slowed significantly from a May 2022 peak – chart 3.

Chart 3

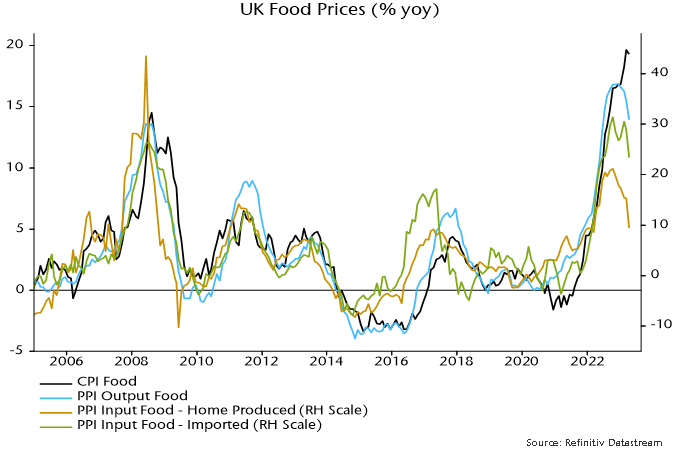

PPI data also indicate that CPI food inflation is peaking and could fall rapidly over the remainder of the year – chart 4.

Chart 4

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)