Commentary

Political risks in EM spike as Indian, South African and Mexican elections surprise

June 14, 2024

The futility of pollsters was on full display in India, Mexico and South Africa this month. Prime Minister Narendra Modi’s BJP fell short of expectations for a landslide in India. In Mexico left-wing party Morena took the presidency as expected, but came surprisingly close to a supermajority in Congress. In South Africa, the dismal performance of ruling party ANC opens up a new era of coalition politics.

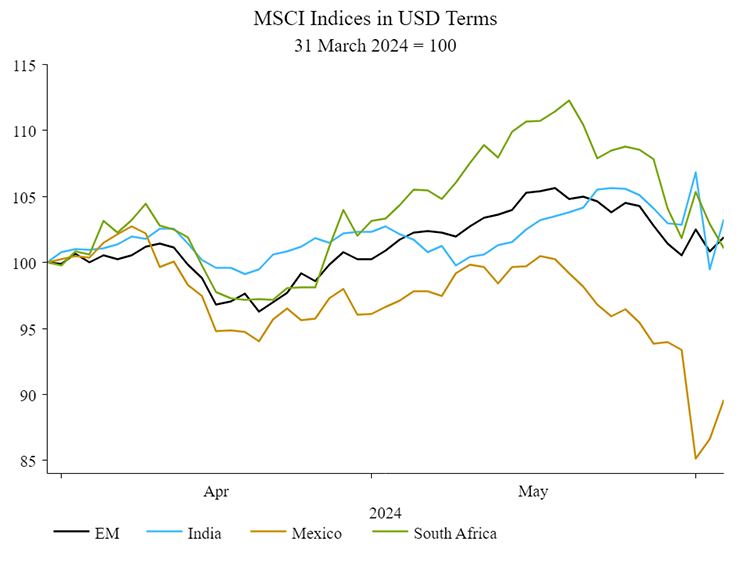

Political risk spiking in these countries has fuelled some wild swings in their stock markets.

All three markets took a hit on election uncertainty through May-June

Source: NS Partners and LSEG Datastream.

Political risk is a factor that we consider as part of our macro analysis, which we know is crucial in EM investing. Fundamentals alone will not save you when the macro is headed south and the risk premium spikes. Outperforming in EM is about finding the right stock in the right country.

India

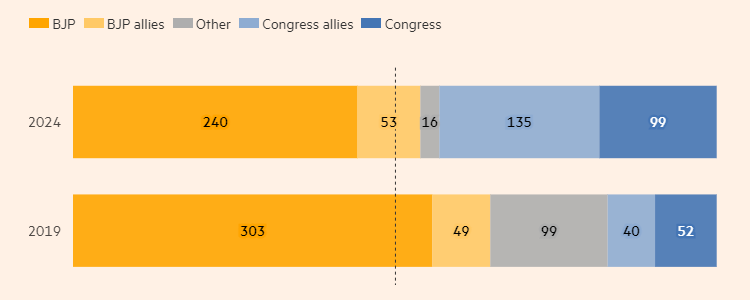

India’s Modi is set to become the first Prime Minister to serve three consecutive terms since the first post-colonial leader, Jawaharlal Nehru (Congress Party). Early June exit polls sent expectations (and stocks) soaring for Modi’s BJP to storm home to victory and claim as many as 400 hundred seats out of 543 in India’s lower house. Stocks exposed to infrastructure led the way on the expectation that a strong mandate would allow Modi to pursue a growth/investment-focused manifesto.

Instead, the BJP failed to claim a majority on its own and will have to rely on the support of regional allies to form government.

Seats won in the 2024 and 2019 elections

Source: Financial Times & Indian Electoral Commission, June 2024.

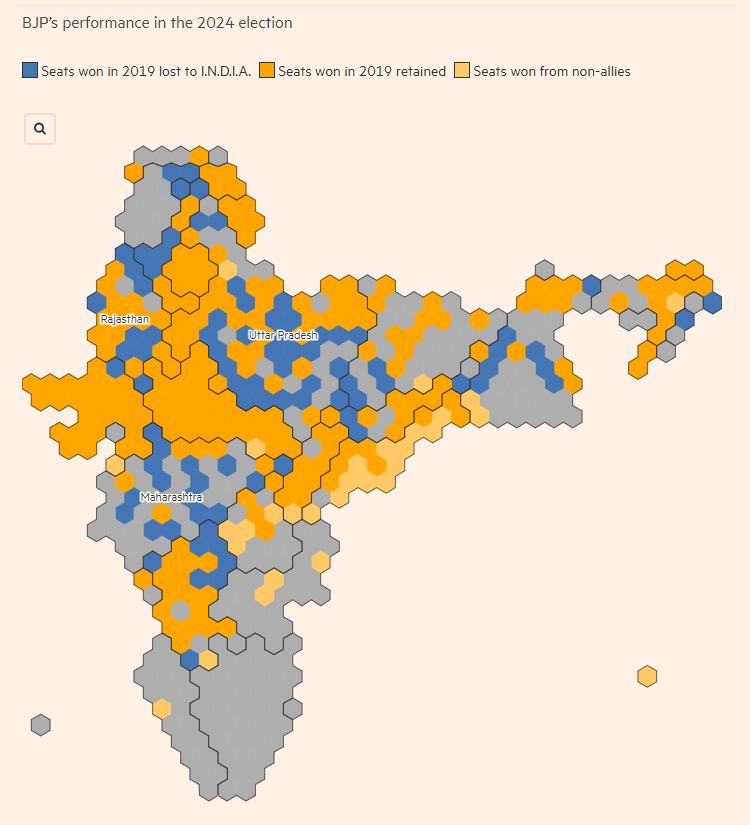

BJP strongholds crumble

The BJP ran on a record of positive reform over the past decade which has fuelled economic growth that has lifted millions out of poverty, cracked down on corruption, and built out electrification and sanitation access across the country. Tax reform also led to a doubling of tax revenue that has been reinvested into developing critical infrastructure, including freight railway lines and ports. Personalised rule and a presidential-style campaign positioned Modi as the figurehead of such rapid progress. At the outset of the campaign, approval ratings for the Indian PM were among the highest for any major democracy in the world.

Yet the damaging swing against the BJP came from the party’s Hindi-speaking northern heartland. The opposition INDIA alliance was able to peel away BJP supporters by targeting poorer rural communities feeling the effects of high inflation and unemployment.

Losses in Uttar Pradesh were pivotal

Source: Financial Times, June 2024.

Positive structural story intact

Modi nevertheless claimed victory in a coalition with regional allies known as the National Democratic Alliance. Despite the surprise verdict, it is unlikely that Modi will be prevented from pursuing his agenda barring a few tweaks likely to increase social spending. This may dilute business sentiment and infrastructure spending in the near term, while consumption should remain robust.

One positive is that the result should alleviate fears Modi would use a supermajority to pursue regressive constitutional changes. On the other hand, there also is a higher risk that a diminished Modi, a pro-growth moderate within the BJP, could cede influence to nationalist elements who will have more sway over a leadership transition.

Overall, our expectation for markets is some profit taking in the short term, while the long term structural story remains very positive.

South Africa

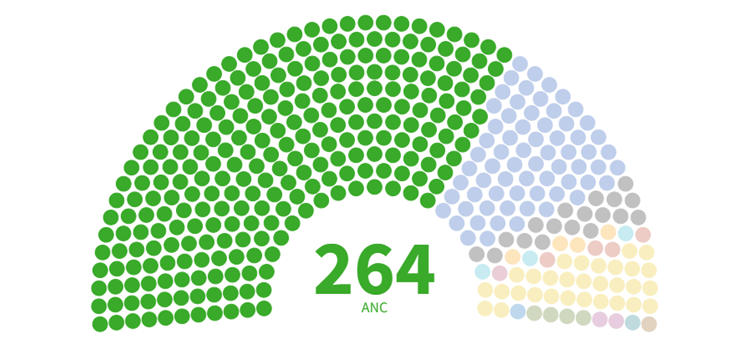

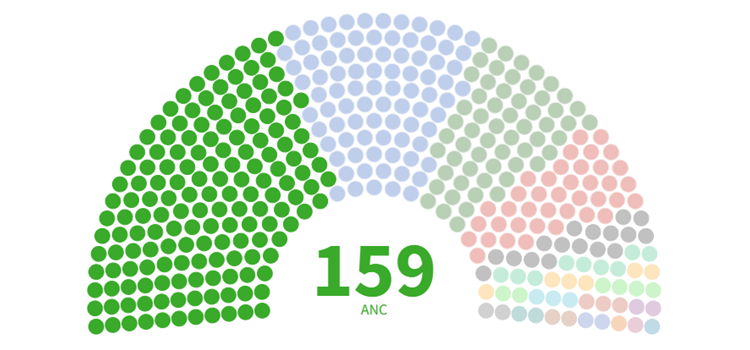

The African National Congress (ANC), South Africa’s dominant political party having governed since 1994, was rebuked by voters for having presided over a polycrisis in the economy, energy and law and order. The scale of the result was the surprise, while uncertainly looms over the make-up of a governing coalition.

The ANC fell a long way short of a majority, commanding only 159 seats of the 400 in the National Assembly. The graphics below illustrate just how sharply ANC support has fallen from a once commanding position.

2009 ANC National Assembly share

2024 ANC National Assembly share

Source: Daily Maverick, May 2024.

The result could mark the beginning of a new era of politics in South Africa. Much like with the decades-long decline of the Congress party in India, the ANC as a post-colonial liberation movement finds itself out of step with the challenges that confront the country today.

Uncertainty and opportunity

The horse trading to form a coalition government within the next two weeks is now underway. The worst outcome, a deal with a radical breakaway party such as disgraced former president Zuma’s MK, who wants to ditch South Africa’s constitution, is off the table, while a direct deal with Julius Malema’s socialist EFF won’t command a majority.

A coalition between ANC and the second largest party Democratic Alliance (DA) is clearly the outcome markets are cheering for, the most likely outcome is for the ANC to kick the can down the road through a multiparty alliance that should disintegrate within 12 months. The result of this may well be a broader re-alignment of South African politics. No doubt this will be a time of high uncertainty, but there is also a chance that some political creative destruction will act as a catalyst for positive change.

Mexico

While the election of Claudia Sheinbaum to Mexico’s presidency was widely expected, the surprise was her left-wing Morena party running close to a parliamentary supermajority. Mexican stocks tumbled 12% and the peso fell on the result as investors fret that a stronger mandate for Morena will allow Sheinbaum to carry on with the agenda of outgoing president Andrés Manuel López Obrador (AMLO).

AMLO’s chequered legacy

AMLO leaves office with high approval ratings owing in part to large cash transfers from the state and minimum wage hikes that lifted over five million Mexicans out of poverty during his term (The Economist (November 2023): Andrés Manuel López Obrador has reduced poverty in Mexico, but he could have done better). In contrast to India’s Modi alleviating poverty through reform-driven economic growth, critics argue AMLO achieved this by diverting funds away from education and healthcare.

Is Morena a threat to Mexico’s democratic institutions?

Crucially for investors, AMLO and Morena are pursuing policies that could threaten Mexico’s institutions. Institutional quality is a key factor in determining whether a country moves up the economic development ladder. Throughout his term, AMLO threatened to attack institutions on the notion that they have been corrupted by neoliberal partisans. His term also saw the military play a growing role in domestic affairs, becoming involved in major infrastructure projects, tourism and customs oversight, and the militarisation of domestic security as a response to rising cartel violence (which proved ineffective).

Investors fear that a strengthened mandate will allow Sheinbaum (or even an outgoing AMLO) to undermine judicial independence, and pursue plans to eliminate autonomous government agencies overseeing telecoms, energy and access to information, as well as weaken electoral supervisory bodies.

Hopes for fiscal discipline

Finance Minister Ramírez de la O has been credited with steering AMLO away from the fiscal profligacy characteristic of so many socialist leaders in Latin America. Markets have welcomed his return in Sheinbaum’s cabinet, with the leader tweeting a series of pledges concerning the economy following a recent meeting with the Minister:

- A fiscal consolidation in 2025 of 3% of GDP to stabilize public finances and the overall debt/GDP ratio;

- Maintain an open dialogue with the investor community and rating agencies to reiterate the new government’s priorities: economic stability, fiscal prudence and feasible fiscal targets.

- Work closely with Pemex [state-owned oil company] and take advantage of the government’s support in Congress to “optimize the use of public resources.”

- Reiterate to international organizations and private investors that the government’s project is based on fiscal discipline, preserving and protecting Banco de México’s independence, a commitment to the rule of law, and incentivising domestic and international private investment.

We are encouraged that the incoming administration is clearly looking to soothe frayed market nerves.

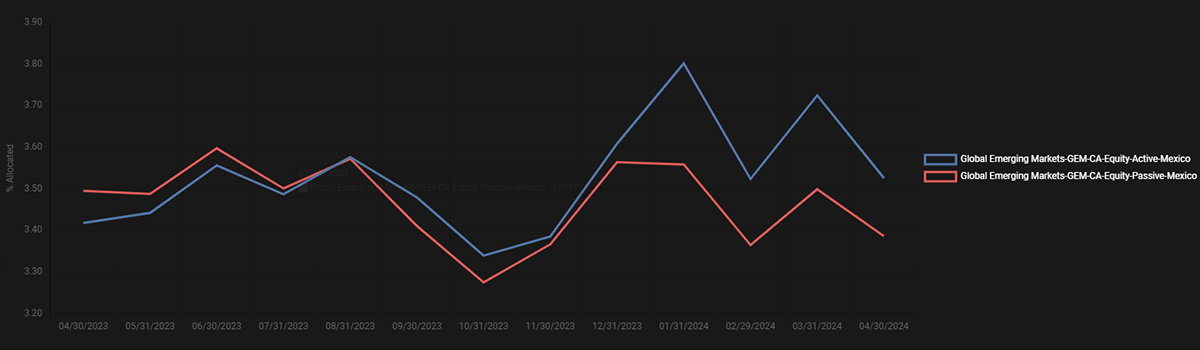

Mexico has been a favourite for most GEM managers

We have been in the minority of GEM investors to remain underweight the market on concerns over political risk, an overvalued currency and exposure to a US slowdown.

GEMs active vs. passive country allocations

Source: EPFR, June 2024.

That’s not to say there isn’t real potential – the trend of global supply chain reshoring and Mexico’s geographic proximity to the powerhouse economy of the US leaves it well-positioned to harness a major structural tailwind in the years ahead.

However, making the most of this opportunity hinges on the dynamism of Mexico’s private entrepreneurs, supported by strong institutions. The question is whether Morena under Sheinbaum can resist their worst instincts.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)