Commentary

Is Mexico snatching defeat from the jaws of victory?

September 18, 2024

The recent push by Mexico’s ruling Morena Party to undermine the country’s judiciary is a perfect example of why relying on company fundamentals alone in emerging markets can leave investors exposed to being whipsawed by macro factors.

We covered election risks across EM In July – Political risks in EM spike as Indian, South African and Mexican elections surprise – and flagged that outgoing president AMLO and president-elect Claudia Sheinbaum threaten to undermine Mexico’s institutional quality through a series of regressive reforms. The most damaging of these is the proposal to overhaul the country’s judicial system through having all judges elected by popular vote, along with relaxing the term limits and age/experience hurdles for Supreme Court justices.

As the Financial Times put it in September (FT: Mexico’s retrograde path on the rule of law):

Mexico is barrelling ahead with one of the world’s most radical shake-ups of a legal system, alarming investors and citizens alike. In his final month in office, President Andrés Manuel López Obrador is using his coalition’s congressional supermajority to ram through constitutional changes to change the entire supreme court and several thousand state, federal and appeal court judges with replacements elected by popular vote. Candidates for some posts will need only a law degree, five years of undefined “legal experience” and a letter of recommendation from anyone in order to run.

Lawmakers have been on strike in recent months protesting the move, but to no avail. In September, Morena wielded supermajorities in both the lower house and Senate to push the reform through, which will see thousands of judicial positions up for election over the next three years. Rather than officials working their way up the legal hierarchy, the judiciary will now be exposed to the corruption, bribery and intimidation of Mexico’s cartels, according to critics.

Snatching defeat from the jaws of victory

Mexico should be in prime position to benefit from supply chain reshoring following the pandemic and ratcheting-up of the Sino-US dispute. Indeed, FDI (much of it from China – Why Chinese Companies Are Investing Billions in Mexico – The New York Times (nytimes.com) was pouring into the country to pursue a bright trade story. We saw this in the sharp appreciation of the Mexican peso and a bull market in Mexican equities through 2023 (MSCI Mexico up 42% in USD terms) with the market a favourite among foreign investors.

US imports from Mexico have outpaced imports from the rest of the world

US imports, index Jan. 2017 = 100

Source: GBM Nearshoring Barometer, August 2024.

Mexico a favourite for foreign equity investors through 2023

Source: EPFR

Sentiment soured on deterioration in the political outlook as Morena’s dominant performance in Mexican elections in June emboldened the party to pursue a series of regressive policies. As we noted in June:

Investors fear that a strengthened mandate will allow Sheinbaum (or even an outgoing AMLO) to undermine judicial independence and pursue plans to eliminate autonomous government agencies overseeing telecoms, energy and access to information, as well as weaken electoral supervisory bodies.

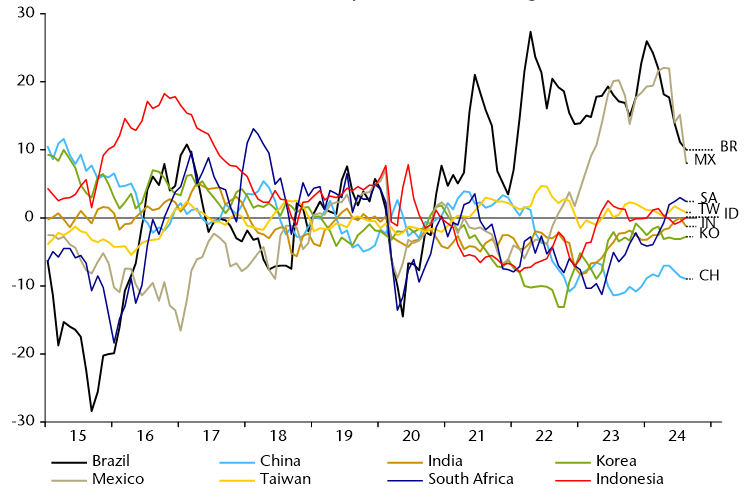

Currency overvaluation correcting in Mexico and Brazil

Real broad effective exchange rates, % deviation from 5y ma

Source: NS Partners and LSEG Datastream

From being one of the consensus overweights among EM investors last year, Mexican equities have been hammered in 2024. MSCI Mexico is down 21% in USD terms to mid-September, while the broader index is up 7%.

Source: Bloomberg

Losing the FDI beauty pageant

As one trade official explained to us on a recent research trip in India, competing for FDI is a beauty contest where participants must maximise their appeal relative to their competition to attract those seeking to deploy capital. China’s retrogressive turn to favour state-owned enterprises rather than the entrepreneurs that fuelled its economy’s meteoric rise is a golden opportunity for ambitious leaders in other emerging markets to step up and attract capital and supercharge development. We are seeing this across ASEAN and in India, eastern Europe and the GCC.

But none have Mexico’s advantage of geographic proximity to an economic juggernaut in the US. President-elect Sheinbaum has talked up Mexico’s nearshoring potential and support for private investment in recent months. However, the rhetoric belies an agenda to undermine Mexico’s institutions, which has unnerved key trade partners and investors.

Nothing scares investors and compromises progress up the development ladder more than attacks on key institutions such as the judiciary. In August, the US Chamber of Commerce warned the Mexican government that the reforms would be likely jeopardise trade relations:

“The U.S. Chamber of Commerce respectfully calls on the sovereign Government of Mexico to continue deliberations with the private sector, academics and legal experts on the package of reforms the new Mexican Congress intends to consider in September. This dialogue is essential to ensure that the proposed reforms contribute to strengthening the rule of law and conditions for economic growth in Mexico.

Given our longstanding commitment to Mexico’s growth and prosperity, the U.S. business community is an important stakeholder in the reform process. American companies represent by far the largest source of foreign direct investment in Mexico and provide good jobs to millions of Mexicans. Whether operating in the U.S., Mexico or anywhere else in the world, American businesses depend on respect for the rule of law as the foundation of a vibrant investment climate, sustainable development, and job creation.

While there is a broad consensus about the need to strengthen Mexico’s judicial system, we strongly believe that certain constitutional and legal reforms currently proposed by the Mexican government – in particular, the judicial reform and the proposed elimination of independent regulatory agencies – risk undermining the rule of law and the guarantees of protection for business operations in Mexico, including the minimum standard of treatment under the U.S.-Mexico-Canada Agreement. The reforms also put at risk Mexico’s obligations under other international treaties to provide all with the right to a competent, independent, and impartial judicial system.

Further deliberation to address these concerns is needed to avoid jeopardizing the incoming Mexican government’s ability to generate shared prosperity and to tap into the potential of nearshoring to strengthen the country’s economic growth and development.”

Macro matters – downgrading Mexico

Our process involves scoring the level of team conviction for every emerging market each month and includes an assessment of the direction of travel for politics in the short run and institutional quality in the long run. The trajectory is negative on both counts, and we think souring sentiment could have some way to run.

We have been underweight and defensively positioned in Mexico for well over a year, on a view that a slowing US economy would be an economic drag for Mexico. The deteriorating political backdrop flows through to a downgrade of our conviction rating for Mexico, and consequently a reduction in exposure. The market is already trading at a significant valuation discount to the 10-year average, but we think it can get cheaper still.

Portfolio activity

We sold our defensive staple Walmex last month, in favour of shale oil producer Vista Energy. While listed in Mexico, Vista is actually an Argentinian company boasting a growing production profile. Its shale assets in the Vaca Muerta (Spanish for Dead Cow) geologic formation are some of the best in the world. In contrast to Mexico, there are also some signs that the political backdrop in Argentina is improving under libertarian president Javier Milei, including efforts to deregulate the oil and gas sector which could provide an additional tailwind for Vista.

The race is on

As Mexico falters, we expect competition to reap the fruits of reshoring to heat up. ASEAN, the GCC and India are all banging on the door for foreign investment flows. Political stability, as well as safeguarding and improving institutional quality, will be the keys to success.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)