Commentary

Implications of Asian currency tremors

May 16, 2025

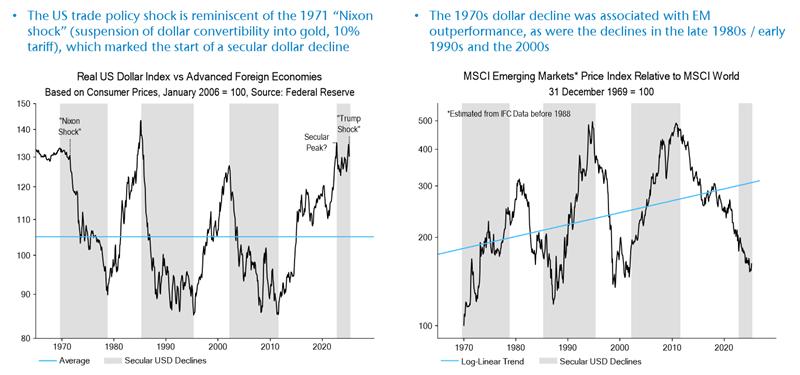

Currency intervention across Asia in recent weeks may be yet another signal that we are entering a new investment order. We have written to clients previously that a secular peak in the USD likely occurred at the end of 2022.

Looking back to previous peaks in the 1970s and 1980s under Nixon and Reagan respectively, the dollar provided a powerful signal to investors that the US economy was experiencing major distortions that would force policy intervention.

President Trump’s Liberation Day tariff shock is part of a broader play to reinvigorate the competitiveness of American manufacturing. Another key pillar of the strategy is the desire for a weaker dollar. We are now starting to see this play out in Asian currency markets.

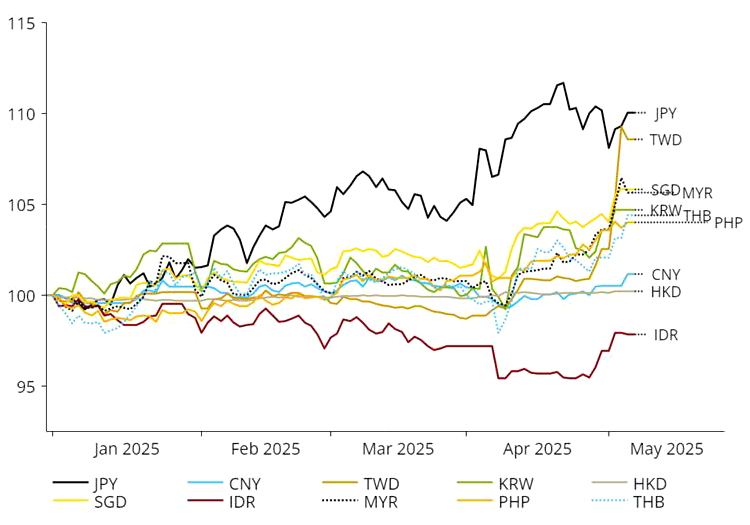

The most dramatic moves were in the Taiwan dollar, which surged by 9% over two trading days, reaching three-year highs and logging its sharpest daily gains since at least 1981.

East Asia currencies vs US dollar

31 December 2024 = 100

Source: NS Partners and LSEG (May 2025)

Source: NS Partners and LSEG (May 2025)

Currency tremors may signal the start of a broader shift in global capital that could have big implications for which markets out- or underperform going forward. As the Financial Times reported in “The Coming Asian FX ‘avalanche’” (7th of May 2025) quoting Eurizon’s Stephen Jen:

“We have long warned about the ‘Avalanche’ risk for the dollar. There could be USD2.5 trillion worth of ‘snow’ in China and more from the likes of Taiwan, Malaysia and Korea, rising at a pace of USD500 billion a year – we conservatively guesstimate. Only a modest proportion of the very large trade surpluses these countries have earned have been repatriated back home, with the bulk of the export earnings being hoarded by exporters in USD deposits.

“Like in actual avalanches, ex-ante, many might dismiss the warnings, but ex-post, all would admit that it was an obvious risk. We are still waiting for more triggers, but we see the sharp sell-off in USDTWD this week from this Avalanche perspective. We predict there will likely be other sudden lurches lower in USDAsia in the coming quarters. Corrections in USDAsia could pacify the US, as Asia accounts for more than half of all US trade deficit, making this a fundamentally benign development, except for those caught long dollars.

“The overhang of liquid dollar holdings is just too large if the dollar weakens, the Fed cuts interest rates, and China stages a cyclical rebound. In other words, both the push and pull factors that kept the export earnings in dollars outside the home countries in the past years will potentially flip signs in the coming quarters. At the same time, many of those holding long-dollar exposures know very well that the dollar is over-valued.”

Emerging markets love a falling dollar, which is an environment we’ve not seen in over 13 years.

Source: LSEG Datastream

Source: LSEG Datastream

Historically, this has seen EM outperform DM, while the winners and losers within the asset class also rotate. For instance, while the strong dollar environment typically favoured EM exporters, a weak dollar would be a shot in the arm for domestic consumers.

Other markets which could surge are those which the United States permits to manage their currencies against a falling dollar by easing monetary policy. There are a number of other smaller EM economies with managed exchange rates which could enjoy surging liquidity that feeds bull markets in financial assets.

The cleanest example of this currency-liquidity transmission is the Hong Kong dollar peg. When the USD falls, the Hong Kong Monetary Authority intervenes to maintain the HKD peg by buying USD and selling HKD, increasing HKD supply. This surge in liquidity lowers interest rates, stimulates economic activity and can lead to higher asset prices (and inflationary pressures).

Our liquidity analysis should be a powerful tool for identifying the risks of both booms and busts if this trend continues.

It’s all about pricing power for the export winners

While exporter stock prices may pop in the coming months on better tariff news, currency dynamics could be important drivers of future outperformance. Let’s use Taiwan Semiconductor Manufacturing Company (TSMC) as an example at the stock level. The company has previously given clear guidance that every 1% of appreciation in the TWD against the USD is a 0.4 ppt hit to OPM. We roughly model this impact out below to illustrate the currency risk to earnings:

| EPS | Q1 25a | Q2 25e | Q3 25e | Q4 25e | 2025 | Implied PE | Implied share price with 17x | Fr current share px |

|---|---|---|---|---|---|---|---|---|

| Consensus | 13.9 | 14.8 | 15.7 | 15.5 | 60.0 | 15.4 | 1019 | 11% |

| FX Impact (10%+) | 13.9 | 13.7 | 12.7 | 12.1 | 52.4 | 17.5 | 891 | -3% |

| FX Impact (15%+) | 13.9 | 13.1 | 12.1 | 11.5 | 50.6 | 18.2 | 861 | -6% |

| FX Impact (20%+) | 13.9 | 12.5 | 11.5 | 10.9 | 48.8 | 18.8 | 830 | -10% |

If we assumed a further appreciation of TWD/USD to 25 – a 20% appreciation from where TSMC recently guided (when TWD/USD was 33) – the hit to TSMC’s EPS is around 23%.

If we apply a mid-cycle PE (17x) to the company and factor in the earnings hit from the currency shift, that would take us to a stock price of TWD830 from the TWD950 at the start of May.

Adding to the risk is the unpredictability of tariffs negotiations between the United States and Taiwan. Tariffs above 20% on Taiwan semiconductor exports could be a meaningful hit to earnings. Perhaps authorities in Taiwan are allowing the TWD to appreciate as part of a pitch to avoid tariffs.

Mitigating the risks is TSMC’s immense pricing power. We believe robust demand will persist for the leading-edge chips enabling AI where it has a monopoly status. This positions TSMC to pass through a significant portion of price increases to its customers.

However, players in the more commoditised segments of the semiconductor industry which lack the moats and pricing power will be more vulnerable to hits from tariffs and currencies.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)