Commentary

AI supply chain bottlenecks are opportunities for EM tech leaders

March 18, 2024

Summary

- A bounce in unloved Chinese equities led a positive month for EM stocks, with the MSCI EM Index up nearly 5% in USD terms.

- Among the leaders was portfolio holding Trip.com, which surged over 25%, reflecting a recovery in consumer demand for travel in China.

- Korean stocks continued a run of strong performance fed by enthusiasm for the government’s proposed Corporate Value-up Program (covered in detail in last month’s commentary: Super-cheap Korean equities rally on market reform talks).

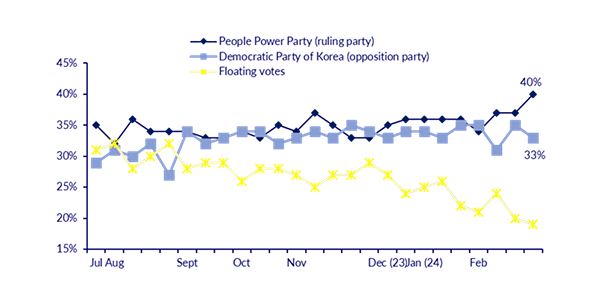

- With around a third of South Korea’s population actively participating in the stock market, the reforms have boosted the ruling Democratic Party’s legislative election prospects, its approval rating reaching 40% against 33% for the opposition. The chart below from CLSA shows the turnaround in fortunes since the program was announced earlier in the year.

Korea general election poll

Source: Gallup Korea & CLSA, March 2024.

- With less than one month before the election, re-election of the Democratic Party with a mandate to press forward with the reforms could be a catalyst for further outperformance by Korean equities.

AI boom exposes supply chain bottlenecks

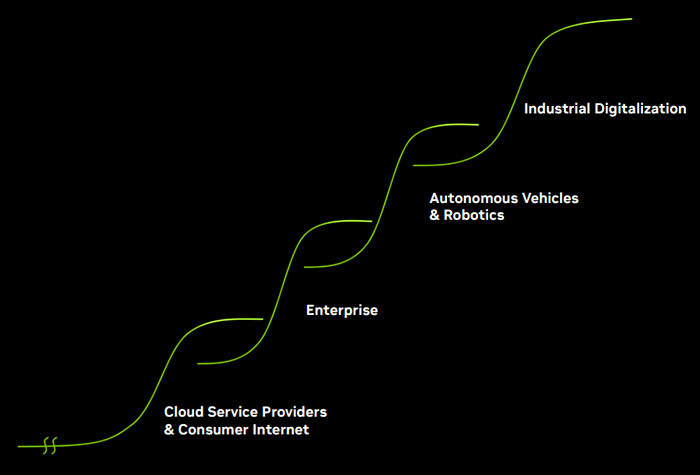

The global rush is on to harness an explosion of AI innovation, with investment by hyperscale cloud and consumer tech giants only the first wave of adoption powering demand for the technology.

Waves of AI adoption

Source: Nvidia Corporate Presentation, 2024.

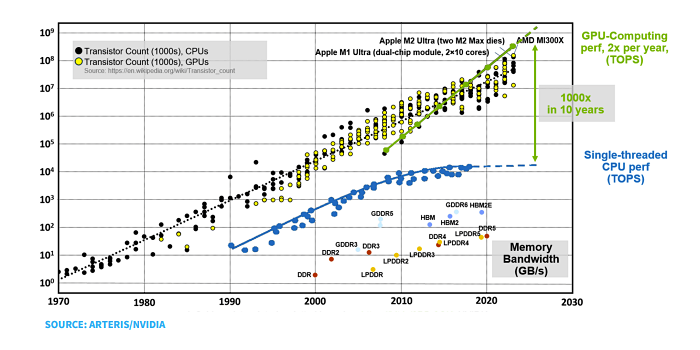

What unleashed this step change? While some more complex neural network architectures and algorithms have emerged in recent decades, the real shift has been the rapid advances in brute processing power that enables machine learning.

The chart below illustrates the yawning gap which has opened up between the power of GPUs (green line) and conventional CPUs (blue line), with the former now capable of executing many trillions more operations per second (TOPS).

Explosion in power of high-end chips

Source: Nvidia/Arteris, 2023.

The chart also hints at one of the key bottlenecks to scaling AI applications like ChatGPT – aside from the difficulty of meeting the sheer scale of demand for Nvidia’s high-end GPUs – which is “memory wall.”

To illustrate the concept, one useful analogy we have heard is to imagine an AI server as a steam train, with the GPU being the engine, data being the coal, and the network being the person shovelling the coal. Getting all the juice out of the massive GPU engine depends in large part on how quickly that coal (data) can be shovelled into the furnace.

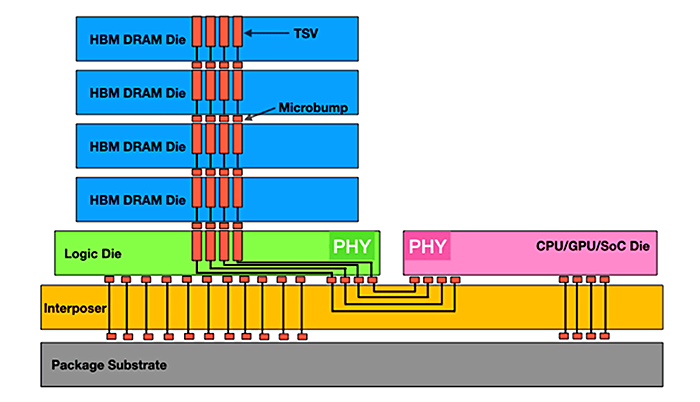

This is where High Bandwidth Memory (HBM) comes in. HBM is physically bonded to the GPUs in stacked layers via thousands of pins which enable “massively parallel data throughout” (The Pragmatic Engineer: Five Real-World Engineering Challenges).

HBM stack

Source: Semiconductor Engineering, 2023.

This tech enables the data transmission at a speed of about 3TB/second, around 100 times faster than conventional data transfer architecture powering PCs. This speed is crucial given the massive amounts of data that need to be fed into large language models like ChatGPT.

The issue (and opportunity) is that this wave of demand for leading-edge computing tech to power AI is far outpacing supply. HBM costs around five times more than conventional memory, with Korean memory giant SK Hynix controlling half of global supply, and the remainder split between Samsung and Micron. Hynix is set to enjoy a margin boost driven by premium memory products such as HBM, which it forecasts to grow at a 60-80% CAGR for the next five years.

Emerging markets are home to a host of companies like Hynix, which dominate their respective niches in the AI supply chain. Opportunities exist across multiple segments including fabrication, design, and testing capabilities, as well as key components (like HBM) that form the foundations of hyperscale computing that powers AI.

Chinese stocks outperform as stimulus efforts kick into gear

Chinese stocks are plumbing the depths, now trading at a CAPE of around 10X (from 21X in 2021) discounting a deflationary outlook. While Premier Li Qiang attended the World Economic Forum meeting in Davos earlier this year to announce that China met its 5% GDP growth target for 2023, investors were fretting about steepening consumer price declines. The stock market is signalling an increasing risk of corporate bankruptcies (BBC – Evergrande: Crisis-hit Chinese property giant ordered to liquidate) and financial instability in the absence of decisive monetary and/or fiscal intervention.

Will the authorities blink? It is certainly within the Party’s wheelhouse to pivot, especially given the risk that further economic malaise stokes political instability. The abrupt end to zero-COVID policy in 2022 is the most recent pragmatic policy turn under Xi. Could he reprise Deng Xiaoping’s dictum that “to get rich is glorious” alongside an announcement of fiscal stimulus?

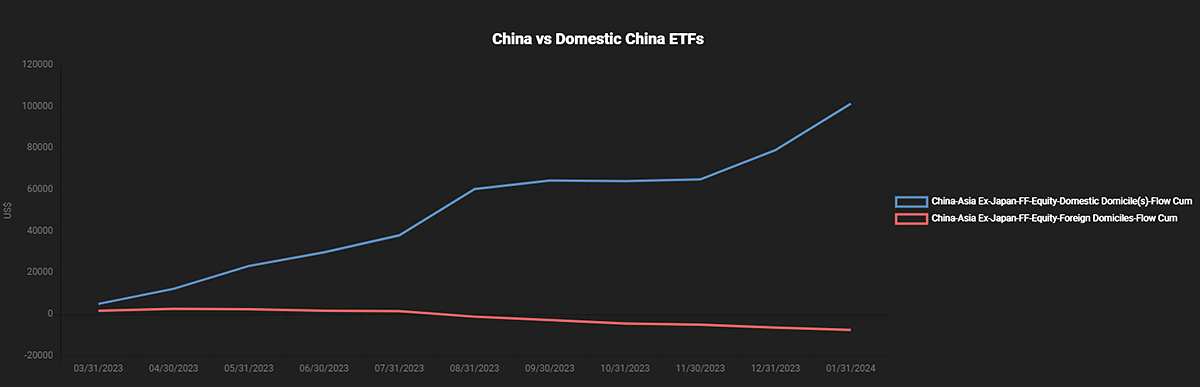

That is doubtful to say the least, but recent activity suggests the authorities understand there is a problem. SOE and SOE-linked names outperformed through February on the back of the “national team” (state-backed financial services companies) ploughing US$57 billion into Chinese equities so far in 2024 (China ‘national team’ ETF buying reaches $57bn this year, says UBS). The chart below from fund data provider EPFR shows flows from local Chinese investors into domestically domiciled China funds (blue line) of just under $100 billion over the 12 months to 31st January 2024. Contrast this with negative flows for foreign-domiciled China funds (i.e. for foreign investors) over the same period.

Source: EPFR

During the month, Xi Jinping was briefed by the China Securities Regulatory Commission (CSRC), coinciding with the replacement of the Commission’s chief Yi Huiman in favour of former banking regulation veteran Wu Qing (known as the “broker butcher”). Bloomberg noted that the move echoed government efforts in 2016 to boost market confidence by dismissing financial regulators amid a market rout (China Replaces Top Markets Regulator as Xi Tries to End Rout).

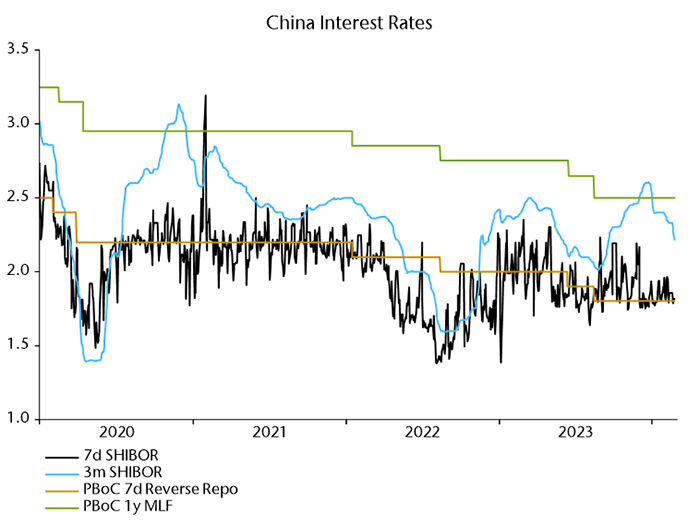

A visit to the central bank by Xi last year preceded record levels of lending from the PBoC to the banks in Q4, followed by an earlier and larger than expected cut in the reserve requirement ratio (RRR) in January, which suggests the central bank is now back on an easing track.

Money rates responding to liquidity injection

Source: LSEG Datastream.

On the fiscal side, the government revealed a GDP target of “around 5%” at its National People’s Congress, suggesting further modest stimulus is on the way.

We have flagged in previous commentary the risk that deteriorating institutional quality under Xi appears to be crushing the animal spirits of entrepreneurs and consumers. Indeed, we saw Xi tighten the CCP’s grip over the private sector, announcing new anti-corruption crackdowns across a host of key sectors in January.

Tone-deaf policymaking amid a fragile economic backdrop is causing economic paralysis and interferes with the credit impulse. No one is complaining about a shortage of credit. The real issue is a shortage of confidence among consumers and businesspeople. Consumers are hoarding cash in time deposits, while banks aren’t looking to borrow short and lend long to businesses to invest. While all of this is structurally negative for China over the long term, continued policy easing at these valuations could be the catalyst for a large trading rally in Chinese equities.

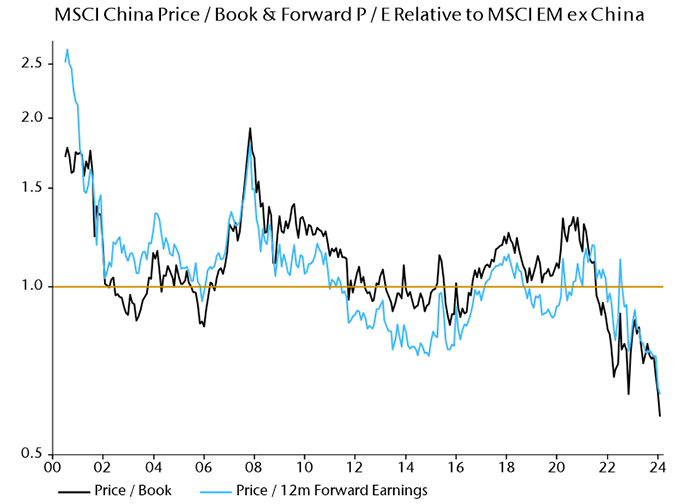

MSCI China at record discount to rest of EM

Source: LSEG Datastream.

Our strategy is to maintain a modest underweight to China and position defensively while waiting for further confirmation that liquidity is improving.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)