Money Moves Markets

Monetary deficit finance and medium-term inflation

February 16, 2021 by Simon Ward

G7 headline consumer price inflation will spike in H1 2021, possibly reaching 3-4%, which would mark a 13-year high. Central banks will portray the rise as a temporary blip but the “monetarist” view is that higher inflation is related to the 2020 broad money surge and will be sustained into 2022. A key issue is whether G7 broad money growth will return to its low post-Global Financial Crisis (GFC) average in 2021. Monetary financing of enlarged fiscal deficits was the key driver of the 2020 surge and is likely to remain a significant contributor in 2021, suggesting that broad money will grow by 5-10% over the course of the year.

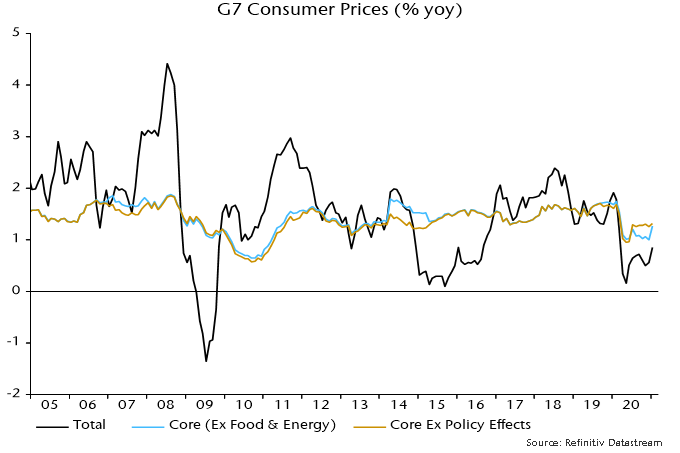

G7 core CPI inflation, i.e. excluding food / energy and adjusting for policy effects such as VAT changes in Germany / the UK and Japan’s travel subsidy programme, is estimated to have been stable at 1.3% in January – see chart 1. Mainstream forecasters had expected a significant fall in response to last year’s economic weakness but the latest reading is exactly in line with the post-GFC average (i.e. over 2010-19).

Chart 1

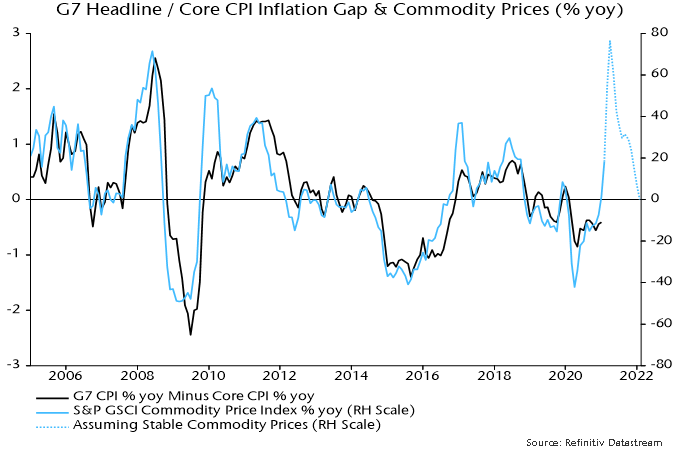

Headline inflation remained below core in January but the headline / core gap will spike during H1, reflecting recent commodity price strength and base effects. The relationship in chart 2 suggests that the gap will reach 2 percentage points or more, in which case stable core inflation of 1.3% would imply a headline rate peak of 3-4%.

Chart 2

Central banks and the consensus are expecting a pick-up, though probably not on this scale. The official response will be insouciance – an inflation comeback, it will be argued, would be welcome but the rise is temporary / technical, with output gapology signalling future weakness. Headline inflation is indeed likely to retreat during H2 but the “monetarist” view is that it will continue to exceed forecasts into 2022, reflecting last year’s broad money surge and an average two-year lead from money to prices. Commodity prices may strengthen further later in 2021, with core inflation lifting into 2022.

Chart 3

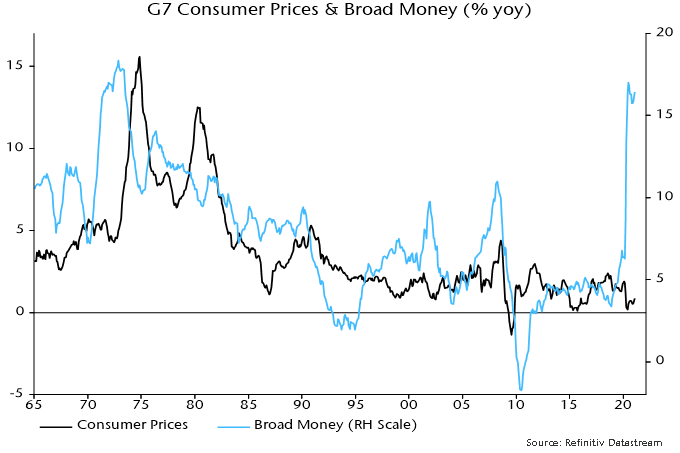

Medium-term inflation prospects, on this view, hinge critically on whether G7 broad money growth will return to around its low post-GFC average of 3.7% during 2021. Annual growth, estimated at 16.4% in January, will fall sharply from March as negative base effects kick in but the central case here is that it will end the year at 5-10%, consistent with a lasting inflation upshift.

The central case recognises that monetary financing of fiscal deficits was the key driver of the broad money surge and – with deficits remaining large – is likely to make another sizeable contribution this year. Bank lending to the private sector is projected to grow weakly but not to contract, as it did after the GFC as banks sought to pare their balance sheets to boost capital ratios.

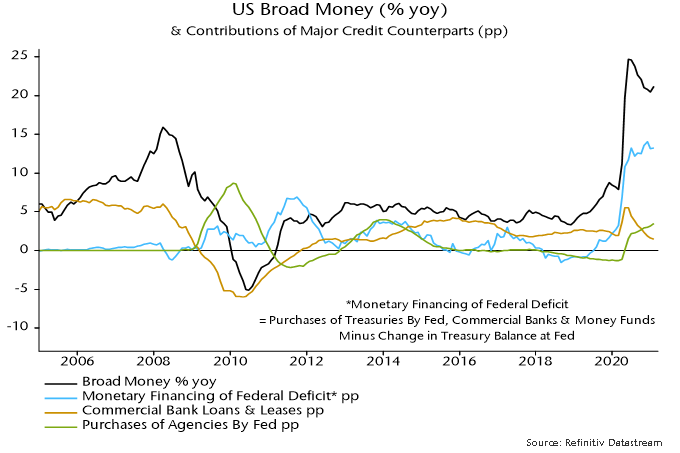

Chart 4 shows the main credit counterparts of US broad money* growth. Monetary deficit financing – defined as net lending to the federal government by the Fed and private monetary institutions – accounted for an estimated 13.2 percentage points (pp) of annual broad money growth of 21.2% in January. The Fed’s purchases of agency MBS added a further 3.5 pp, with growth of commercial banks’ loans and leases contributing only 1.5 pp.

Chart 4

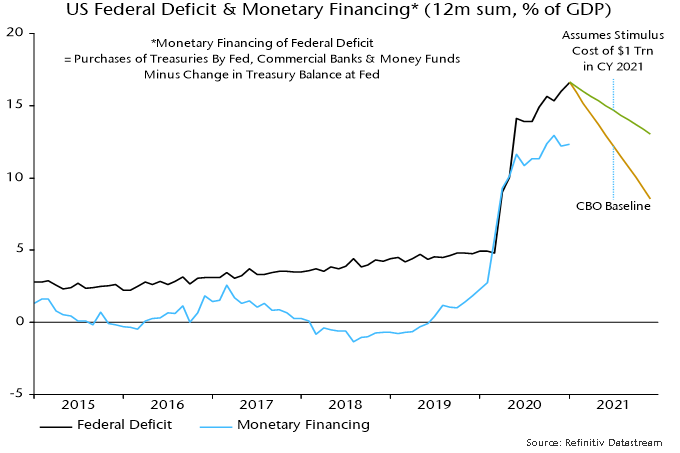

The rise in monetary financing mirrored the blow-out of the federal deficit, which reached 16.0% of GDP in 2020 – chart 5. Non-monetary financing as a share of GDP – the gap between the black and blue lines – was slightly larger in 2020 than in 2019, though smaller than in 2018.

Chart 5

The CBO’s revised baseline budget forecasts released last week suggested a fall in the federal deficit to below 9% of GDP in 2021 on unchanged policies. President Biden’s stimulus package could, on a conservative estimate, maintain it at about 13% of GDP. Assuming that monetary financing covers the same proportion as in 2020, the implied contribution to broad money growth in the 12 months to December 2021 would be about 9 pp.

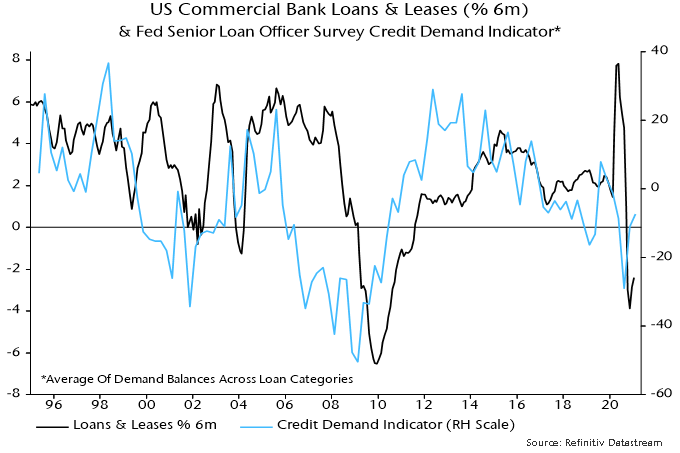

Will a contraction in commercial bank lending pull down broad money growth, as it did after the GFC recession? The latest Fed senior loan officer survey reported a reduction in credit tightening along with a modest recovery in demand – chart 6. Bank lending may make little contribution to money growth in 2021 but is unlikely to be a major drag.

Chart 6

Fed purchases of agency MBS are running at $40 bn per month, suggesting a 2 pp contribution to broad money growth over a year. Other credit counterparts could conceivably have a negative impact (e.g. banks’ net external lending if capital were to flow out of the US in scale) but a reasonable base case is money growth of at least 5% during 2021 and probably significantly higher.

A similar argument applies in other G7 economies. Monetary deficit financing accounts for the bulk of recent UK broad money growth and has also been a key influence in the Eurozone. Fiscal deficits may show an earlier decline than in the US but bank lending to the private sector could make a larger contribution, reflecting official subsidy and guarantee schemes.

*M2 plus large time deposits at commercial banks plus institutional money funds.