Money Moves Markets

Less favourable monetary conditions for markets?

November 23, 2021 by Simon Ward

The term “excess money” describes a monetary backdrop in which growth of the stock of money exceeds the rate necessary to support economic expansion. Excess money is associated with increased demand for financial assets and upward pressure on their prices, other things being equal.

Excess money cannot be measured directly. Two global proxies are followed here: the gap between six-month growth rates of real narrow money and industrial output; and the deviation of 12-month real narrow money growth from a slow moving average.

These measures have been strongly correlated with equity market performance historically. Between 1970 and 2020, global equities outperformed US dollar cash by 17.9% pa on average when the two measures were positive (allowing for reporting lags). They underperformed by an average 3.6% pa when one of the measures was negative and by 9.2% when both were.

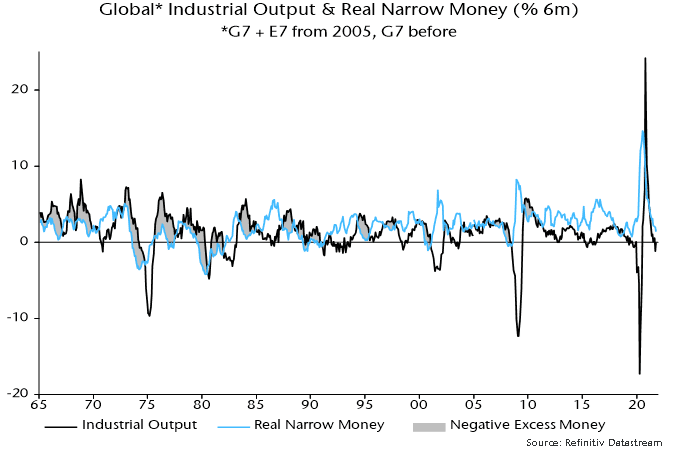

The first measure remains positive despite a large fall in six-month real narrow money growth because of offsetting weakness in industrial output – see chart 1. Output growth has been held back by supply constraints and is likely to bounce back temporarily as these ease.

Chart 1

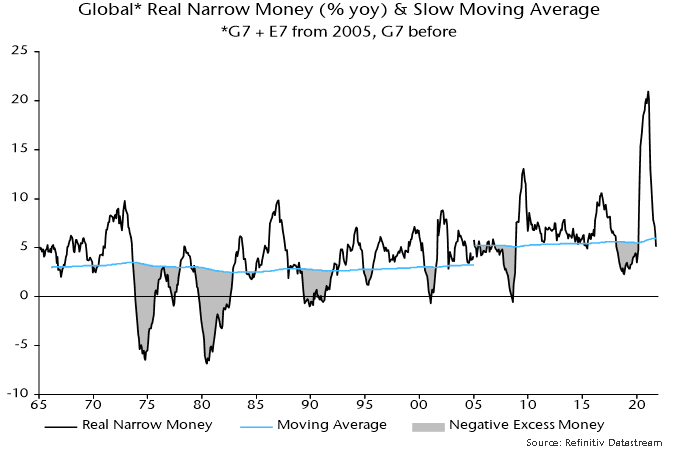

12-month real narrow money growth is estimated to have fallen below the slow moving average in October, turning the second measure negative – chart 2.

Chart 2

The long-term performance of equities / cash switching rules based on the individual measures has been similar. The second measure, however, has outperformed in the recent past – the associated rule recommended cash at the start of 2020, switched to equities in April and now suggests a move back into cash.

The rule associated with the first measure recommended equities in 2020 but switched to cash for several months in early 2021, reflecting a spike rebound in industrial output growth. Equities continued to climb during this period.

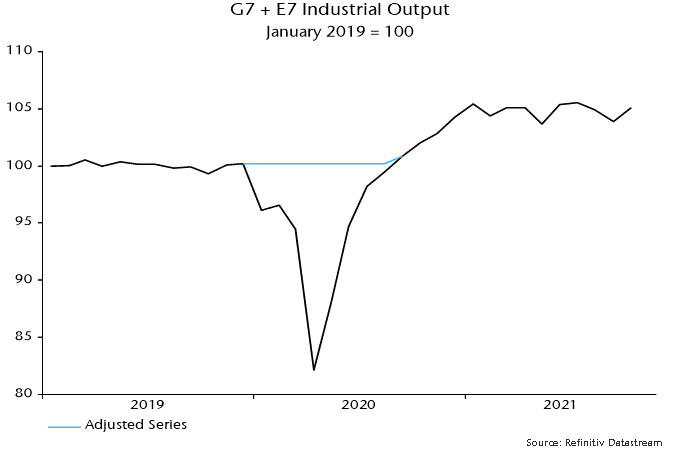

The lesson from this experience is that output volatility due to temporary non-cyclical factors – in this case the covid shock – should be discounted when using this measure. For example, the V-shaped fall and rebound in global industrial output during 2020 could (should) have been removed from the measure by using the alternative series shown in chart 3. An excess money measure incorporating the adjusted series indicated that the monetary backdrop remained favourable in early 2021.

Chart 3

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.