Commentary

Inflation is Fading Fast

October 6, 2022

Summary

- September was a deeply negative month for stocks globally, with EM declines led in large part by very poor sentiment in China.

- Cyclical consumer technology stocks in Korea and Taiwan were hit hard as signs emerge that global demand is waning.

- For the portfolio, high quality and defensive names across healthcare, consumer staples and communications services held up over the period to post positive returns.

- Hawkish central banks around the world are determined to kill inflation, even at risk deepening an oncoming recession and as signs emerge that inflation is peaking globally:

- oil prices have been falling through the quarter;

- metals prices are easing on soft economic numbers in China;

- soft commodity prices are falling as grain exports by Ukraine resume; and

- short term gas European gas prices fall despite war the escalating war in Ukraine and attacks on the Nordstream gas pipelines.

- Our position for several month has been that inflation is set to collapse, led by rapidly declining liquidity from central banks.

- Inflation expectations are anchored while global real money weakness suggests a recession through to Q2 2023.

- Central banks are likely to ignore this and are unlikely to slow tightening unless some structural stresses emerge.

- China remains attractive as modestly positive real money trends continue to suggest economic resilience relative to other majors.

Portfolio Activity

- We continue to add to our China overweight.

- Despite the negative sentiment, liquidity and economic data along with the potential for a gradual reopening could underpin one of the only bull markets for a major economy globally.

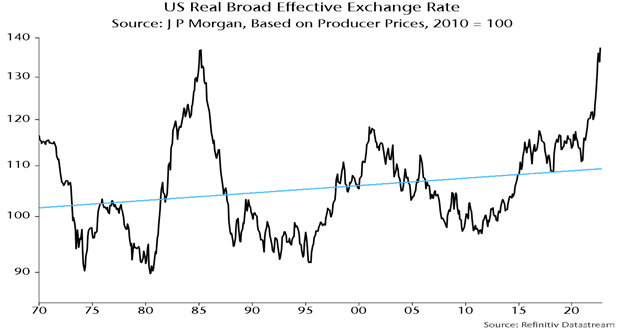

King dollar and the case for EM

- The dollar is hovering around 40-year highs – this is pressuring economies outside of the US. The Truss-Kwarteng mini-budget market revolt illustrates the fragility brought about by rapidly declining liquidity.

EM secular bears associated with USD overshoots

- Our view is that sustained dollar weakness will not arrive until the Fed shifts to a neutral or easing policy bias, which we believe is likely to come sometime after Q1 2023.

- Real narrow money numbers in emerging markets remain stronger than in developed markets, positioning them for relative recovery if USD strength abates.

- Broadly speaking, EM economies did not (and in many could not) deploy the same level of fiscal and monetary stimulus as developed markets through the pandemic, maintained more orthodox monetary policy and today do not face the same problems with inflation.

- Indeed, with the exception of Turkey, monetary policy pursued by EM economies is at its most restrictive level for more than a decade.

- CLSA noted during the month that emerging markets ex-China maintain a “weighted average real interest rate greater than 4ppt above developed economies” and have enough buffer to put tightening on hold before a Fed pause.

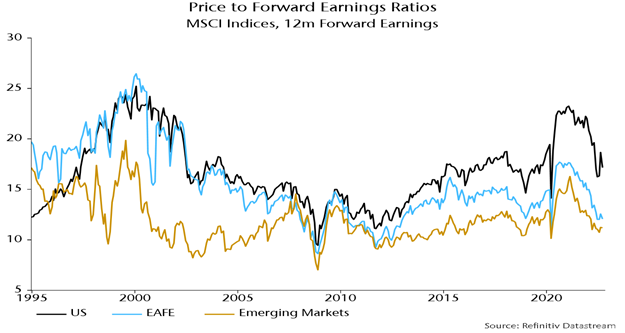

- Also in favour of EM is the relative improvement in EPS growth which is converging with DM (having lagged over the past cycle), and with further room for DM earnings to correct to the downside as recession bites.

- EM relative valuations are trading at distressed levels, with stocks looking particularly cheap in China as the Covid-zero gloom and a grinding property slump weighs on investors.

EM valuations below average (but not quite rock bottom)

Putin under pressure

- Along with liquidity analysis our process also incorporates qualitative macro factors such as institutional quality and political risk. We believe that the ripple effects of the war in Ukraine reverberate globally and play a part in shaping the shaping the opportunity set of our investment universe.

- The 22nd annual Shanghai Cooperation Summit in Uzbekistan’s Samarkand was held during the month, which was significant in a number of respects.

- The Summit marked Xi Jinping’s first trip abroad since the beginning of the pandemic and a potential signal that China is taking the first very tentative steps to reopen.

- It was particularly notable given the trip coincided with the war in Ukraine taking a surprise turn after a successful Ukrainian counter offensive to retake Kharkiv in the country’s east.

- Putin now finds himself under extraordinary pressure, not just from hawkish right wing nationalists domestically, but also from other previously more sympathetic national leaders (and major buyers of Russia’s oil) in China’s Xi and India’s Modi.

- At the outset of the Summit, Putin acknowledged China’s “concerns and questions” over Ukraine, suggesting Chinese discomfort with the trajectory of the Russian leader’s “special operation”. This is a far cry from the “no limits” partnership declared by Xi and Putin in February.

- Indian Prime Minister Narendra Modi pulled no punches, telling Putin that “today’s era is not an era of war” with the Russian leader responding that “we will do our best to stop this as soon as possible.”

- Russia’s leader looks more isolated and desperate, and a diminished partner.

- Particularly so for China which is observing the conflict with interest and drawing lessons with an eye to Taiwan.

- In early April we wrote the following in a memo at the outbreak of war in Ukraine:

“The risk of a conflict between the West and China, particularly over Taiwan, was a low probability but rising. We believe that recent events actually slightly lower that risk. There are signs that China did not anticipate the full scope of Russia’s incursion in Ukraine (invasion vs. a “special operation” in the east), signalled by its shifting messaging and failing to evacuate Chinese citizens early in response to Russian moves leading up to the invasion. It is also likely that neither China nor Russia anticipated the strength and unity of the Western response. We believe that given the economic backlash that Russia is weathering, China has a clear picture of the risks associated with further deterioration in Sino-Western relations.”

- Our view is that events in September support this assessment.

- Indeed, while Sino-US tensions flared after Nancy Pelosi’s visit to Taiwan in August, Chinese officials over the past few weeks have toned down the public rhetoric and stressed that China will strive for peaceful reunification.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)