Money Moves Markets

Equity market “internals” consistent with PMI peak

May 18, 2021 by Simon Ward

The forecast here remains that global industrial momentum, as measured by the manufacturing PMI new orders index, is at or close to a peak, with a multi-month decline in prospect.

The basis for the forecast is a fall in global six-month real narrow money growth from a peak in July 2020 – the rise into that peak is judged to correspond to the increase in PMI new orders to an 11-year high in April.

Available April monetary data indicate that real narrow money growth fell further last month, suggesting that the expected PMI decline will extend into late 2021 – see chart 1.

Chart 1

The presumption here is that PMI weakness will be modest, partly reflecting a view that the global stockbuilding cycle will remain in an upswing through H2. The cycle has averaged 3.5 years historically and bottomed in Q2 2020, suggesting a peak in Q1 2022 assuming an upswing of half-cycle length. Large declines in PMI new orders (i.e. to 50 or below) have usually occurred during cycle downswings.

Any PMI pull-back, however, could have significant market implications given consensus bullishness about global economic prospects.

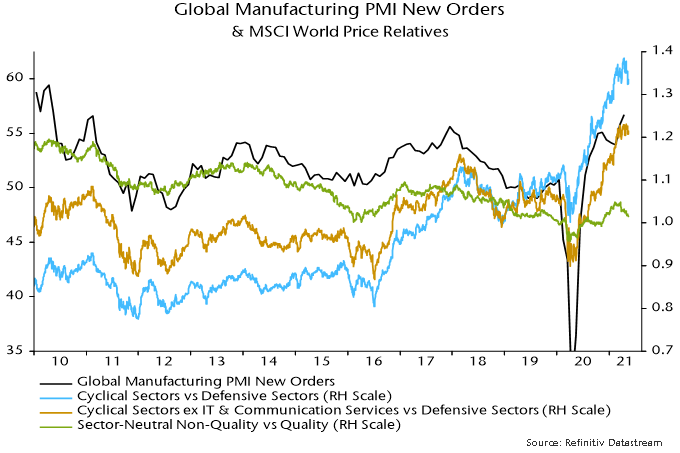

Historically, a declining trend in global manufacturing PMI new orders has been associated with underperformance of cyclical equity market sectors and outperformance of quality stocks within sectors. The price relative of MSCI World cyclical sectors to defensive sectors peaked in mid-April, falling to a three-month low last week – chart 2.

Chart 2

The decline has been driven by a correction in tech – the MSCI cyclical sectors basket includes IT and communication services. The price relative of non-tech cyclical sectors to defensive sectors has moved sideways since March.

The MSCI World sector-neutral quality index, meanwhile, has recovered relative to the non-quality portion of MSCI World since March, following underperformance in late 2020 / early 2021 when cyclical sectors were outperforming strongly.

Equity market behaviour, therefore, appears to have started to discount a PMI roll-over, although confirmation is required – in particular, a breakdown in the price relative of MSCI World non-tech cyclical sectors to defensive sectors.

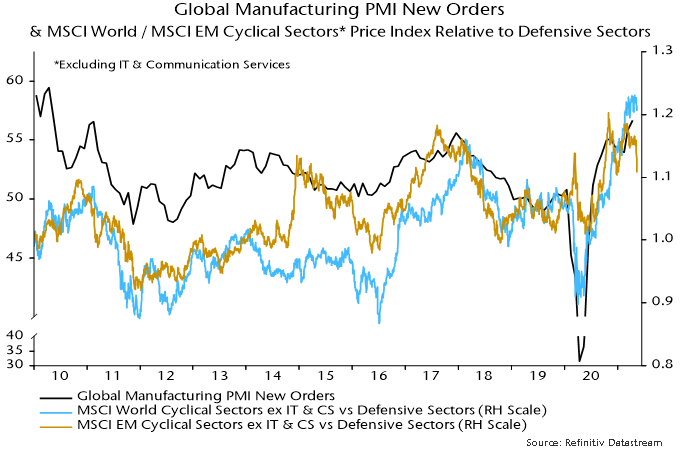

A sign that this could be imminent is a recent sharp fall in the non-tech cyclical to defensive sectors relative in emerging markets – chart 3. A possible interpretation is that the decline reflects worsening Chinese economic prospects, with China likely to be a key driver of a global slowdown. Early Chinese monetary policy easing may be required to mitigate this drag and lay the foundation for a resumption of cyclical outperformance.

Chart 3

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)