Commentary

Emerging Markets Cool into Year-end

January 11, 2023 by Michael Mortimore

Summary

- Slight down month for EM to round out the year.

- The US dollar steadied against major currencies, following a sharp fall in November.

- Turkey finished the year as the best performing market in EM (having been the worst in 2021), nearly doubling in USD terms.

- Unsurprisingly, Russia was the worst, having been rolled out of the index in Q1.

- China was the only major EM market to notch positive gains through the month as reopening moves ahead at a rapid clip.

- Gulf markets struggled as a darkening global economic outlook hit energy stocks.

- India had a down month following strong performance through the year. We think the long-term structural story in India is extremely compelling, but valuations look rich at this point.

- Political risk in South Africa fell following president Cyril Ramaphosa’s re-election as African National Congress (ANC) party leader for a second five-year term, allowing the leader to run in the South African presidential election in 2024.

- Re-election followed a tumultuous campaign, rocked by allegations that emerged in June that a large sum of foreign currency stashed inside a couch had been stolen from the president’s game farm in 2020.

- A subsequent parliamentary investigation indicated that the president may be liable for misconduct, leading to an impeachment vote that was ultimately shot down by the ANC majority parliament in December.

Portfolio activity

- Paring back exposure in Southeast Asia and India to add to China H-shares.

- Maintaining bias to defensive sectors and quality.

Missed opportunity in Turkey?

- There is currently no exposure to Turkey in the portfolio. Despite the sharp rally this year, we are wary of very poor liquidity and high macro risk. It is hard to see how the recent run is sustainable, to say the least.

- Portfolio Manager Oliver Adcock visited Turkey earlier in 2022 to see whether there is a realistic chance of political change in presidential and parliamentary elections scheduled for most likely June 2023. Markets would undoubtedly cheer the election of an Erdogan alternative who would move quickly to establish a more orthodox fiscal and monetary regime.

- Oliver met with pollsters, the head of one of the opposition parties, banks, corporates and a local thinktank.

- Elections in 2023 look to be a close call, with the most likely outcome being that Erdogan and his AK Party lose control of parliament while retaining the presidency. We see this as a poor outcome.

- One of the factors in Erdogan’s favour is that the coalition of opposition parties (the “Table of Six”) are struggling to decide on a presidential candidate, much less one that is likely to beat Erdogan to the presidency.

- Erdogan does have room on the fiscal side and is likely to continue to pump the economy as much as he can into elections. This is despite headline inflation running at around 80%. Rates have recently been cut to 12%.

- Cutting rates in the face of raging inflation courts serious currency risk, especially when forex reserves stand at around -$56 billion when accounting for currency swap lines (mainly with other Middle Eastern countries).

- One large factor in the market rally has been driven by single stock futures, whereby the Turkish regulator has been allowing investors to reinvest gains made on trades even though they were not closed out. This has had the effect of supercharging the upswing.

- Meetings with a number of banks confirm the economic situation is very volatile and fragile. The government is trying to control everything. New regulation attempts to force banks to lend at rates lower than 25%. The central bank rate is set at 12% but no one is lending there, banks are lending at 20% to SME and consumers, while deposits are 16%.

- Overall, the economic backdrop is changing so rapidly that banks are reluctant to do anything, compelled to keep lending tight, and are holding weekly strategy meetings to assess key risks such as dwindling forex balance sheets.

- The rally in Turkish stocks looks fragile and recent data indicates that foreign investors have been selling into it. Foreign ownership was already at historic lows and has continued to fall so it would seem that very few people have benefitted from this rally apart for the domestic traders who have been pumping the market (in many cases on margin) with the domestic liquidity created in the election run-up.

- Risks are too high for us to build conviction in Turkey, however, it will be worth keeping an eye on polls in the coming months to see if sentiment changes once an opposition candidate for the presidency is chosen.

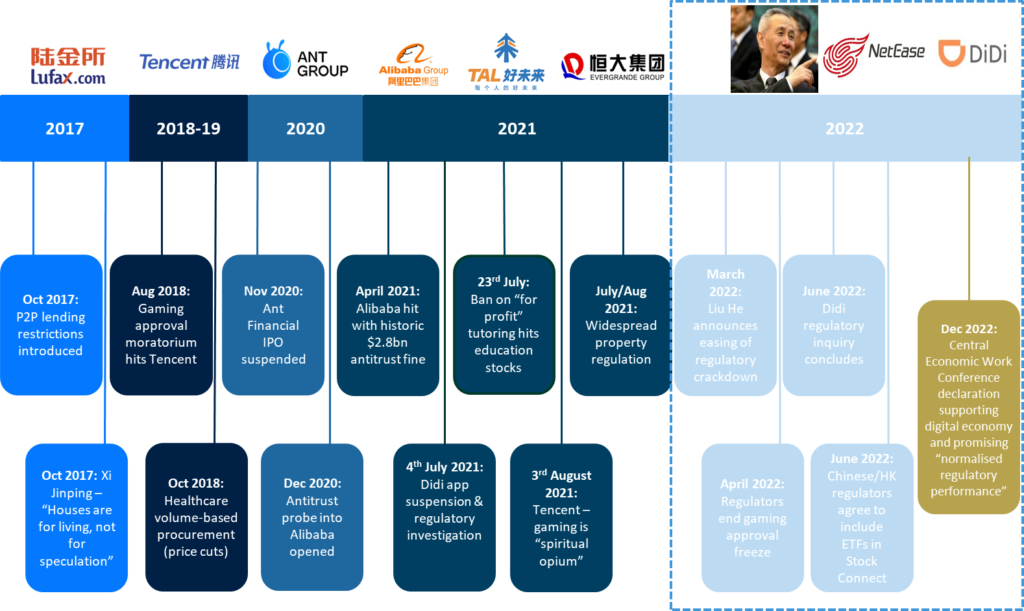

China regulatory headwinds abating

- In March, Chinese Vice-Premier Liu He called for greater order and transparency in regulation of the tech sector. Our view was that this signalled a policy shift from Beijing, and that regulatory pressure was set to ease.

- China made further supportive moves in December at the CCP’s annual Central Economic Work Conference (which shapes economic policy priorities), with policymakers declaring that it is essential to “support platform-based companies to leverage their abilities in leading development, creating jobs, and participating in international competition” (China Daily, December 2022).

- This was soon followed by news that the China’s gaming regulator had granted 84 new game licences to domestic developers, and critically, 44 licences for imported games. These are the first approvals for imports for nearly two years. This shift from Beijing, which in August 2021 described gaming as “spiritual opium,” lifted the stocks of major gaming companies including Tencent and Netease.

China’s reopening accelerates

- Following last month’s COVID 180 and rapid shift to reopening, Beijing pressed ahead through December despite news of a huge spike in cases (and presumably deaths) and hospital ICUs being overwhelmed.

- China’s National Health Commission (NHC) announced a downgrade to the risk level for COVID (from class A to class B infectious disease), effective from 8 January. This effectively removes all centralised quarantine, contact tracing and risk area categorization throughout the country. Further, no control measures related to infectious diseases will apply at the border to all goods and people arriving from overseas. Travellers will only need a 48 hour pre-departure PCR test.

- Outbound travel for Chinese citizens will also resume.

- The NHC also reiterated that its focus will shift to boosting elderly vaccination levels, securing medical supply and healthcare resources (especially in rural areas), as well as prioritising treatment of severe cases.

![Jean-Philippe-Lemay, CC&L FG [504x504_03]](https://ns-partners.cclgroup.com/wp-content/uploads/sites/3/2025/06/FG_-Jean-Philippe-Lemay_504x504_03.jpg)