Money Moves Markets

Easing bottlenecks a sign of weakness not strength

December 3, 2021 by Simon Ward

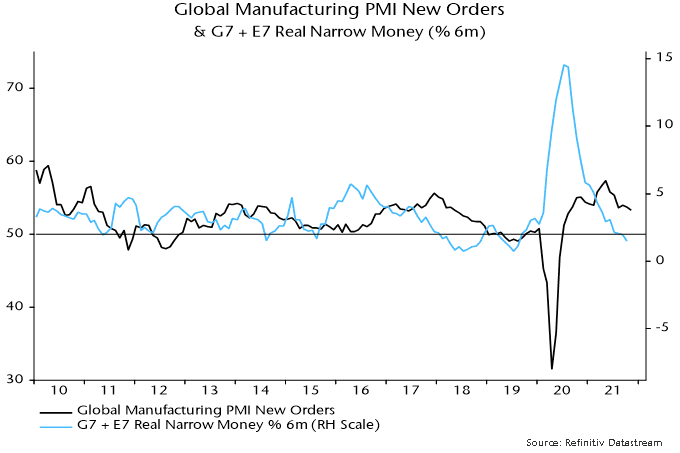

The global manufacturing PMI new orders index – a timely indicator of industrial demand momentum – eased to a 15-month low in November, continuing its decline from a May peak that was signalled by a July 2020 top in six-month real narrow money growth. With additional October data confirming a further fall in real money growth, the PMI orders slide is expected to extend into Q2 2022, at least – see chart 1.

Chart 1

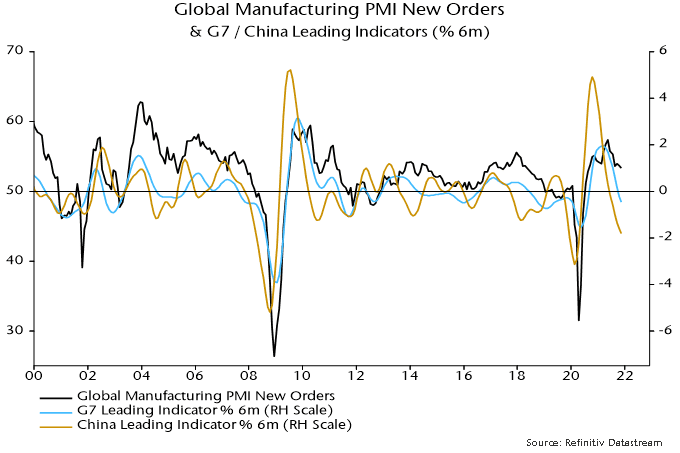

The monetary slowdown signal is supported by the OECD’s leading indicators, November estimates of which are included in chart 2. The OECD indicators mostly exclude monetary aggregates and display a shorter lead time than money.

Chart 2

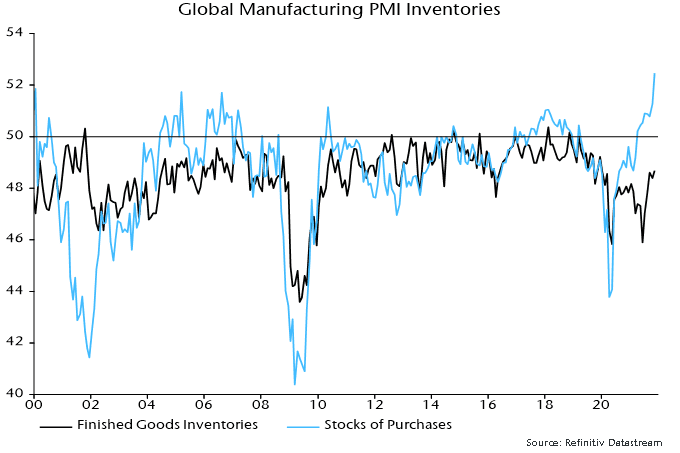

The November decline in global new orders reflected a slight firming in developed markets offset by EM weakness driven by a relapse in China.

The most striking feature of the global report was a further surge in the stocks of purchases index – a gauge of the pace of input stockpiling – to a record. Finished goods inventory accumulation, by contrast, remains “normal” – chart 3.

Chart 3

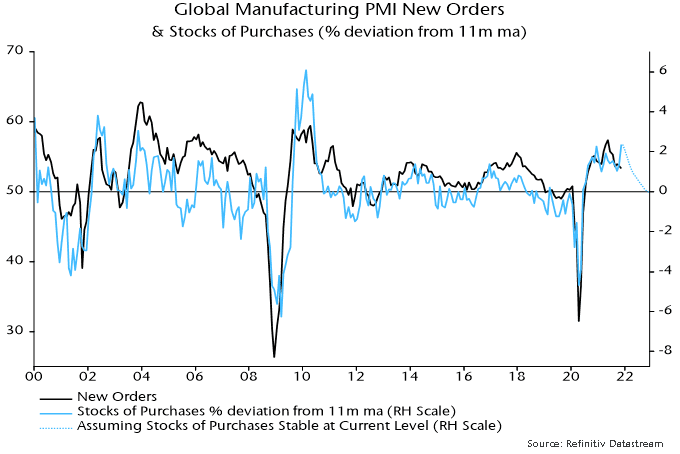

Input purchases by downstream manufacturers have boosted order flow for firms higher up the production chain. Such stockbuilding, however, is peaking and even a stabilisation at the current extreme pace would imply a drag effect on new orders – chart 4.

Chart 4

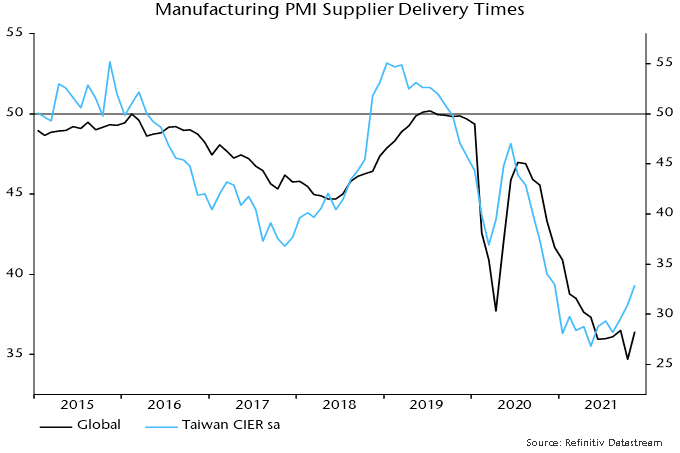

Cooling demand is starting to feed through to an easing of supply pressures. The supplier delivery times index recovered from an October record low (rise = faster), with an extension of an earlier turnaround in Taiwan, which typically leads, suggesting further improvement – chart 5.

Chart 5

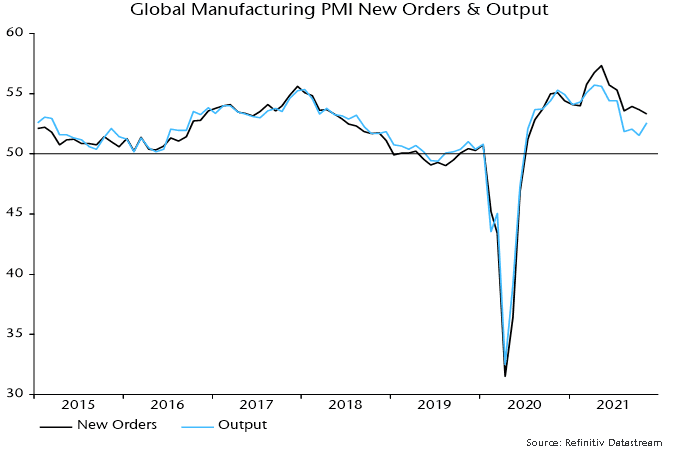

Easing supply problems and a possible pick-up in finished goods inventory accumulation suggest that the PMI output index will catch up with and temporarily overtake new orders – chart 6. An improved supply / demand balance should also be associated with moderating price indices, which probably topped in October.

Chart 6

The judgement here is that markets will focus on softening demand / price momentum and “look through” a temporary output pick-up. Any reignition of the cyclical / reflation trade is likely to require a prior rebound in global real money growth.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.