Money Moves Markets

BoJ / PBoC policy shifts worrying for global monetary prospects

December 20, 2022 by Simon Ward

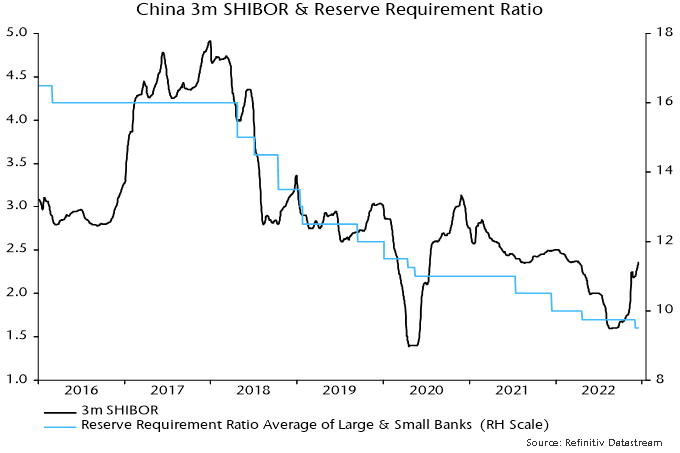

The BoJ’s decision to widen the fluctuation band of the 10-year JGB yield around the zero target follows an apparent withdrawal of monetary policy support by the PBoC in recent weeks.

Three-month SHIBOR has risen by 75 bp since late September and is now only 15 bp below its start-of-year level – see chart 1. Upward pressure has been partly market-driven but the PBoC has chosen not to accommodate increased demand for liquidity.

Chart 1

The PBoC’s Q3 monetary policy report, issued in November, expressed concern about medium-term inflation risks, stressing the importance of avoiding excessive monetary growth. An apparent hawkish shift may have been reinforced by the shock abandonment of the zero covid policy, which officials may view as likely to boost near-term price pressures via a faster demand recovery and / or an increase in supply bottlenecks.

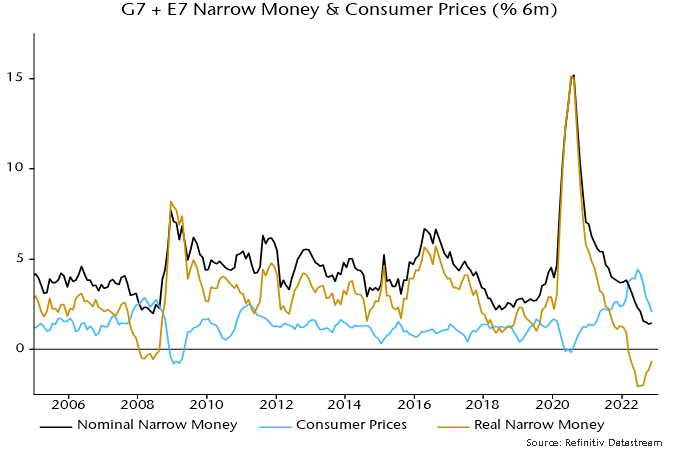

The Japanese / Chinese policy moves are worrying because monetary trends in the two economies have been providing a modest offset to significant US / European weakness – chart 2. That support could now fade.

Chart 2

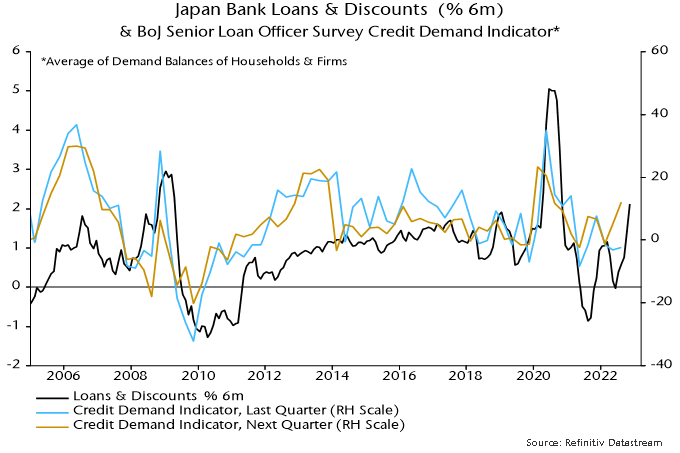

A rise in Japanese six-month narrow money growth in November was accompanied by a further pick-up in bank lending, consistent with stronger credit demand expectations in the BoJ’s Q3 loan officer survey – chart 3. The hope is that firmer bank loan growth / money creation will survive a modest policy adjustment.

Chart 3

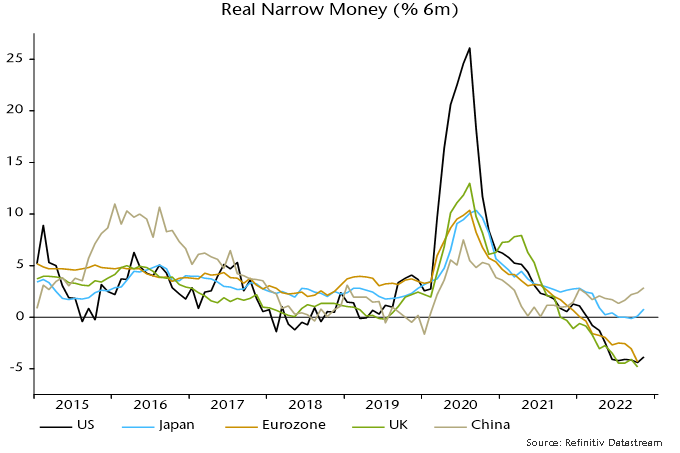

Global six-month real narrow money momentum is estimated to have risen for a fifth month in November but remains negative – chart 3. Allowing for the usual lag, the suggestion is that global manufacturing PMI new orders will bottom by next spring but remain in recessionary territory into Q3.

Chart 4

The recovery in real money momentum continues to be driven by a slowdown in six-month CPI inflation, with nominal money growth languishing – chart 5. The inflation decline will extend but overly hawkish central banks risk pushing nominal money momentum to new lows.

Chart 5