Money Moves Markets

Is Chinese money growth bottoming?

September 20, 2024 by Simon Ward

Chinese money / credit trends remain weak but could be at a turning point.

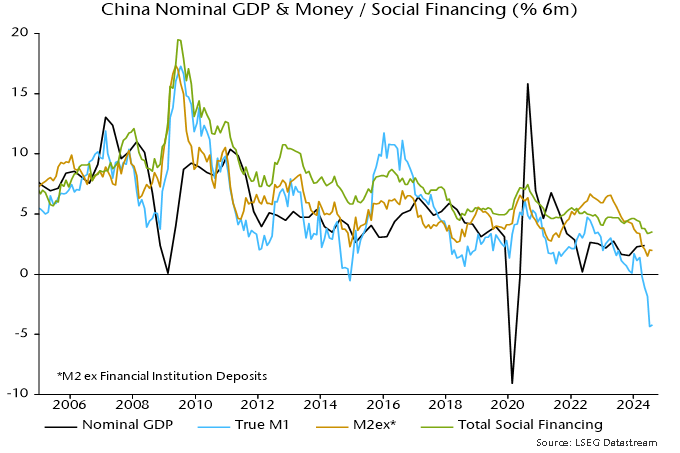

Six-month rates of change of broad money and total social financing have stabilised above June lows – see chart 1. (Broad money here refers to M2 excluding money holdings of financial institutions, which are volatile and less informative about economic prospects.)

Chart 1

Narrow money is contracting at a record pace but has been distorted by regulatory changes in April that have reduced the attractiveness of demand deposits, resulting in enterprises shifting into time deposits and money substitutes while repaying some short-term bank borrowing. (The “true M1” measure shown adds household demand deposits to the published M1 aggregate to align with international monetary convention.)

Chart 2 compares six-month rates of change of the raw narrow money series and two adjusted measures. The first assumes that the share of demand deposits in total bank deposits of non-financial enterprises would have remained at its March level in the absence of the regulatory changes. The second additionally adds the inflow to instant-access wealth management products (WMPs) since end-March (data sourced from CICC), on the assumption that this represents a transfer from demand deposits. Six-month momentum of the latter measure was similar in July to the series low reached at end-2014.

Chart 2

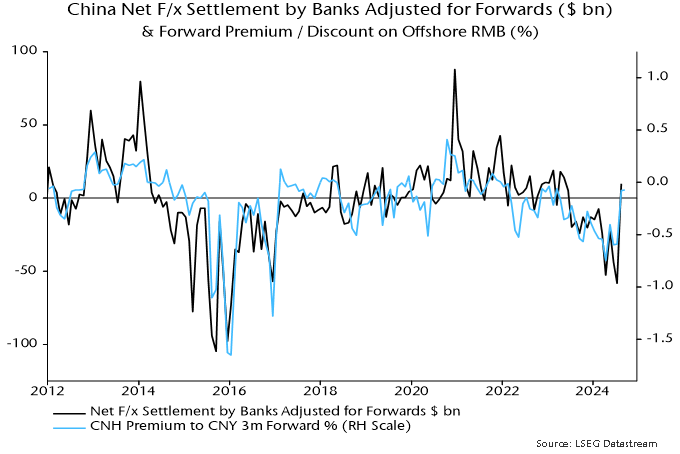

A key reason for expecting money / credit reacceleration is that the yen rally has relieved pressure on the RMB, easing monetary conditions directly and opening up space for further PBoC policy action. The balance of payments turnaround is confirmed by a swing in the banking system’s net f/x transactions, including forwards, from sales of $58 billion in July to purchases of $10 billion in August. This series captures covert intervention via state banks (h/t Brad Setser) and an August reversal had been suggested by a sharp narrowing of the forward discount on the offshore RMB, which has remained lower so far in September – chart 3.

Chart 3

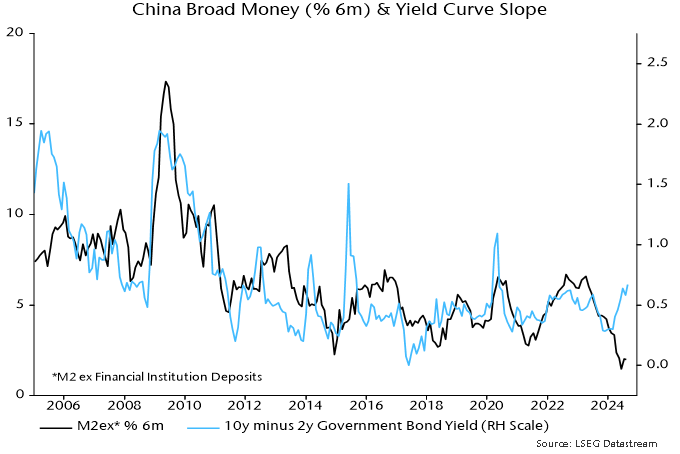

Actual and expected monetary easing has been reflected in a further steepening of the yield curve, which has correlated with, and sometimes led, money momentum historically – chart 4.

Chart 4

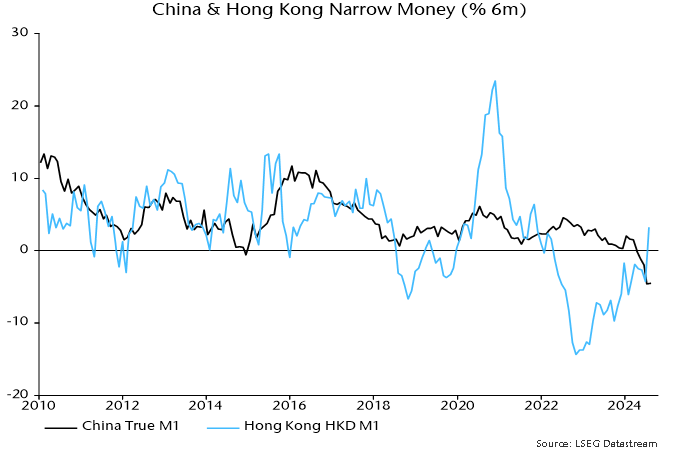

An easing of Chinese monetary conditions coupled with the start of a Fed rate-cutting cycle could have a powerful monetary impact in Hong Kong, where six-month momentum of local-currency M1 recently returned to positive territory, having reached its weakest level since the Asian crisis in October 2022 – chart 5.

Chart 5