Will US consumers spend their money stash?

The consensus expects US consumer spending to continue to grow solidly despite the current inflation squeeze on real wages and associated weakness in sentiment / confidence – the average forecast is for a rise of 3.6% in 2022, according to Consensus Economics Inc. This partly reflects an assessment that spending has been supply-constrained while consumers have substantial unused fire-power in the form of money balances accumulated against a background of high saving over the past 18 months.

The suspicion here is that much of the increase in money holdings reflects portfolio and precautionary demand, implying little implication for near-term spending prospects.

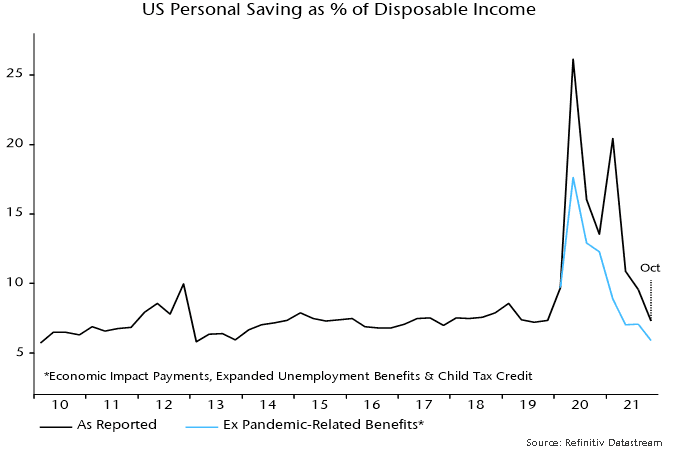

The personal saving ratio has now fully reversed its 2020 surge, with October’s 7.3% reading the same as in December 2019 – see chart 1.

Chart 1

The ratio, moreover, continues to be inflated by temporary pandemic-related benefits, which are winding down and will expire at year-end. Excluding such benefits from the income definition, the saving ratio was 5.9% in October, close to a post-GFC low of 5.8% reached in 2013.

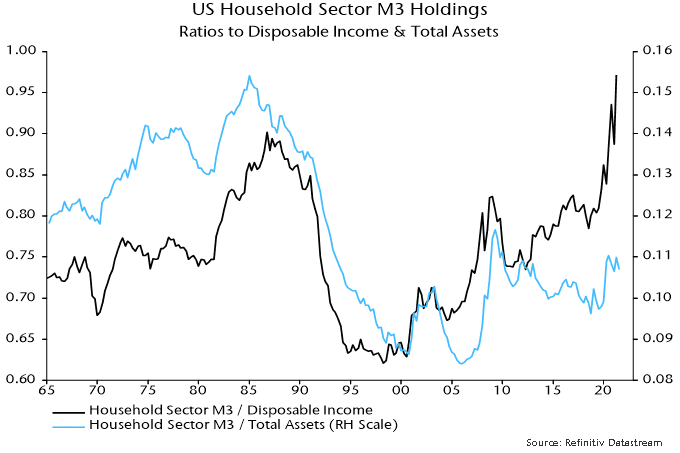

Bulls argue that the saving ratio will remain low or fall further as supply shortages and pandemic disruption fade, allowing consumers to spend accumulated money balances. According to the Fed’s financial accounts, households’ broad money (M3*) holdings surged by 29.9% between end-2019 and mid-2021, pushing their ratio to disposable income to a record – chart 2.

Chart 2

The demand for money, however, depends on portfolio considerations as well as income / spending. With household wealth – housing as well as financial – growing strongly before and during the pandemic, the ratio of money holdings to total assets remains within its post-GFC range and below the long-term historical average.

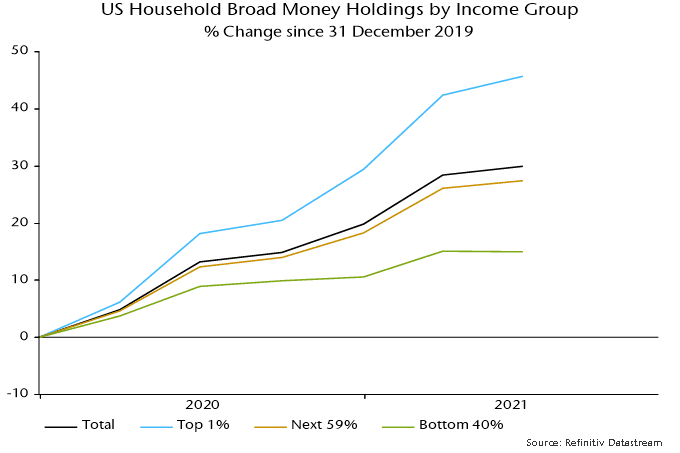

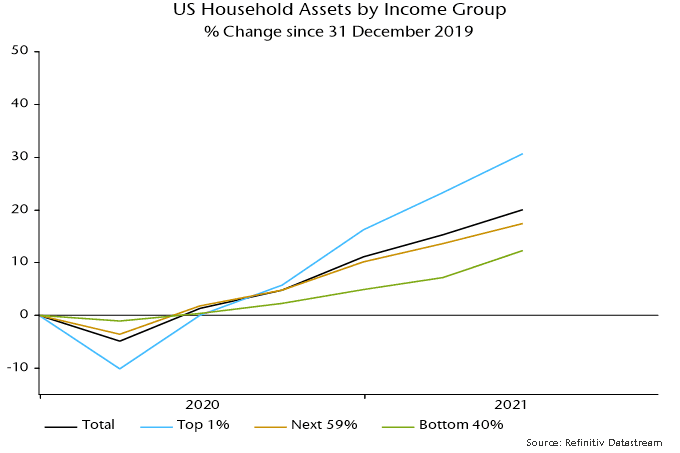

The suggestion that much of the money surge reflects portfolio demand rather than unsatisfied consumer spending is supported by Fed data breaking down money holdings by income level.

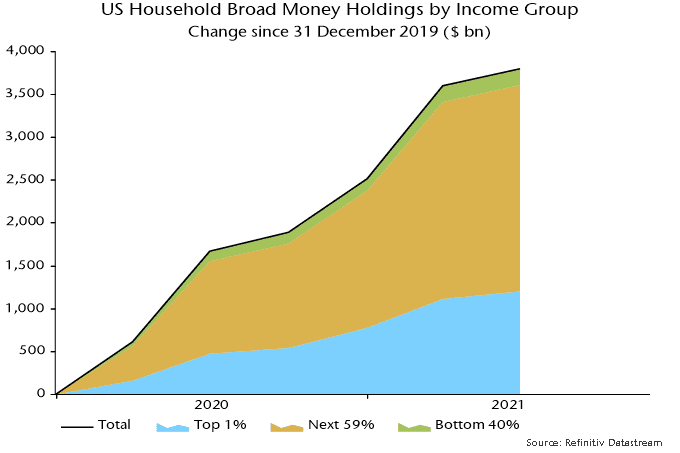

M3 holdings of the top 1% of income-earners rose by 45.7% between end-2019 and mid-2019, accounting for 9.5 pp of the 29.9% increase in total household money balances over this period – charts 3 and 4.

Chart 3

Chart 4

The bulk of the remaining increase in money holdings was absorbed by other households in the top 60% of the income distribution – their money balances grew by 27.4%. The bottom 40% of income-earners accounted for only 1.5 pp of the 29.9% increase in household M3, their holdings growing by 15.0%.

The money growth ranking of the three groups mirrors relative increases in wealth: total assets of the top 1% of income-earners rose by 30.6% between end-2019 and mid-2020 versus growth of “only” 12.4% for the bottom 40% – chart 5

Chart 5

Independent of portfolio money demand considerations, the marginal propensity to consume out of money balances is likely to be lower for higher-income households.

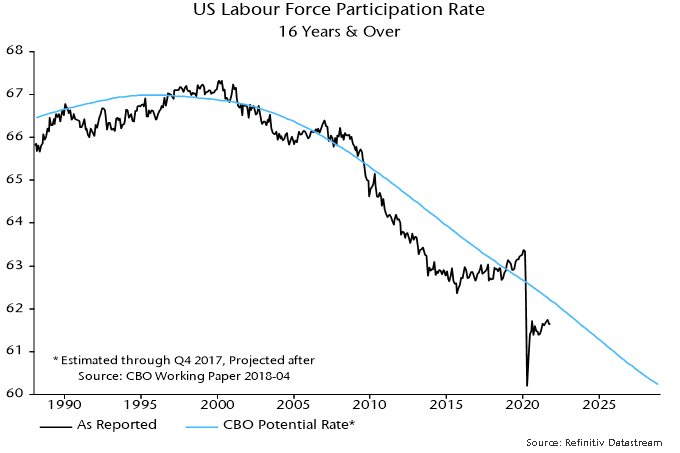

If the above argument – that high money balances may not signal further consumer spending strength – is correct, the consensus forecast for spending growth in 2022 is likely to require strong expansion of employment incomes. This, in turn, may depend on a significant recovery in labour force participation.

A CBO study in 2018 contained a long-term projection for the “potential” (i.e. cyclically-adjusted) labour force participation rate based mainly on demographic factors (i.e. the changing age structure of the population). This projection suggests that most of the recent decline is “structural”, in which case Fed / consensus assessments of labour market slack (and possible employment growth as this is absorbed) may be overoptimistic – chart 6.

Chart 6

*Checkable deposits and currency, time and savings deposits, and money market fund shares.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.