Weak Eurozone money data

A post last month argued that a pick-in Eurozone broad money M3 growth into September reflected temporary factors that would reverse. October numbers delivered the expected turnaround, with M3 falling by 0.4% on the month. Narrow money measures, meanwhile, lost further momentum, with Italian data particularly weak.

The summer pick-up in M3 growth had been discounted here for two reasons: the numbers had been boosted by rapid and probably unsustainable expansion of financial sector deposits; and the pick-up was inconsistent with the behaviour of the credit counterparts (bank lending to government and the private sector, net external lending etc), instead reflecting a statistical “residual”.

October numbers showed a large drop in financial M3 holdings, correcting earlier strength, while the credit counterparts residual turned negative.

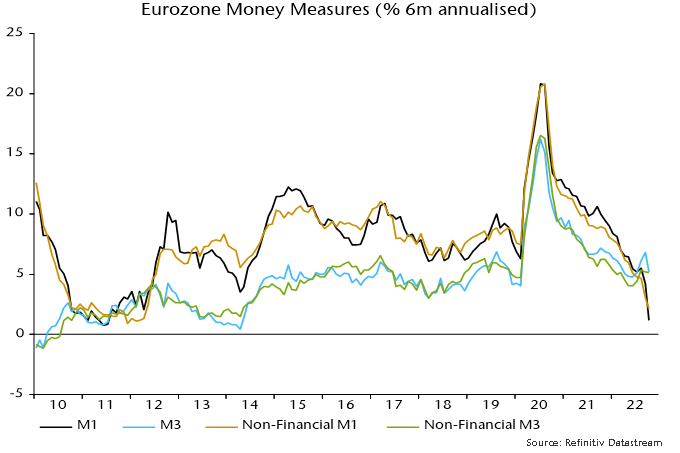

The preferred money measures here exclude financial sector holdings, which correlate poorly with near-term economic performance. Six-month growth of non-financial M3 was stable in October at 5.2% annualised; growth of non-financial M1 slumped further to 2.1% annualised, the weakest since the 2011-12 Eurozone crisis / recession – see chart 1.

Chart 1

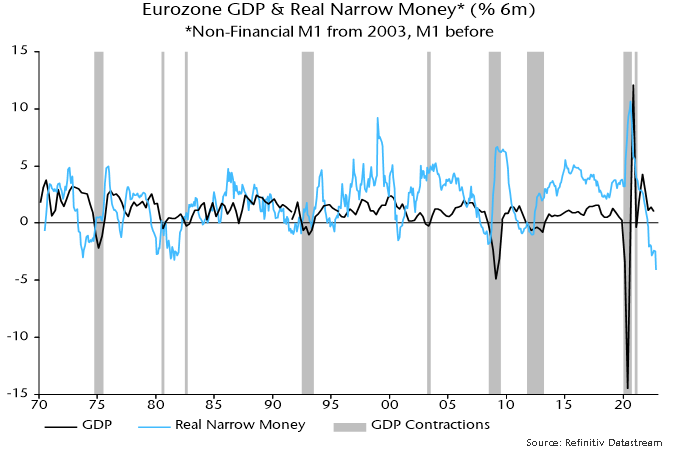

Real narrow money is contracting much faster than during that crisis: the six-month rate of decline reached a new record in data extending back to 1970 – chart 2.

Chart 2

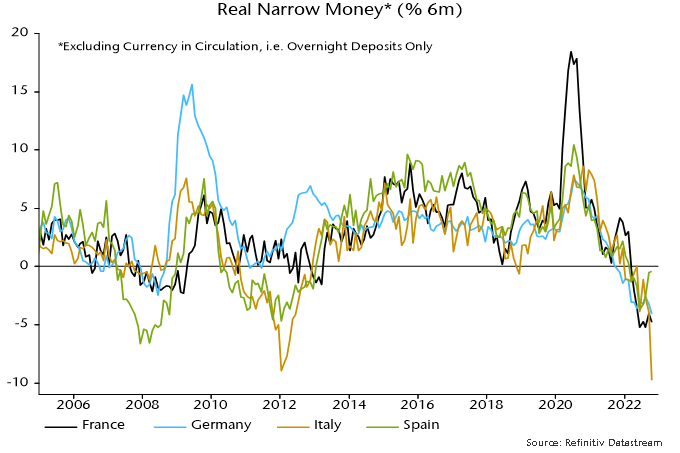

Country data on real overnight deposits (including financial sector holdings) show particular weakness in Italy, reflecting both nominal contraction and a larger recent inflation spike than elsewhere – chart 3.

Chart 3

The previous post suggested that a lending slowdown would act as a drag on broad money growth. Bank loans to the private sector were unchanged on the month in October.

Cyclical sectors of European equity markets have recovered some relative performance recently, possibly reflecting a belief that a grim economic outlook was becoming less dire at the margin. A minor recovery in the expectations component of the German Ifo business survey might be viewed as supporting reduced pessimism – chart 4.

Chart 4

The level of Ifo expectations, however, remains historically weak and a further fall in Eurozone / German six-month real narrow momentum argues that economic stabilisation, let alone a recovery, remains distant – chart 5.

Chart 5

Nominal money trends and prospects suggest that monetary conditions are already restrictive, contrary to the ECB’s assessment*. Likely policy overtightening is another reason for fading the cyclical rally.

*See speech by Executive Board member Isobel Schnabel.