Unusual UK monetary movements

UK monetary statistics for September were heavily distorted by cash-raising by LDI funds to meet collateral requirements for derivative contracts.

The headline M4ex broad money aggregate surged by £91 billion, equivalent to 2.7% after seasonal adjustment, between end-August and end-September. Money holdings of non-bank financial corporations* accounted for £71 billion of this increase.

The long-standing practice here has been to focus on non-financial monetary aggregates, where available, because movements in financial sector money holdings can be erratic and usually have little bearing on near-term economic prospects.

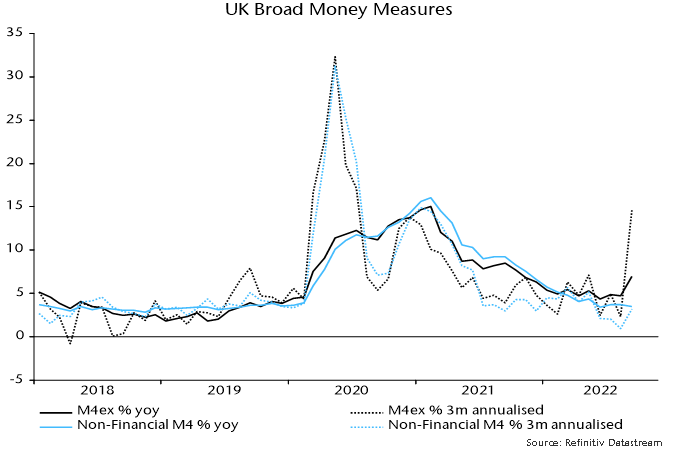

Non-financial M4, encompassing money holdings of households and private non-financial businesses, rose by £21 billion, or a seasonally adjusted 0.3%, in September. Annual growth eased to 3.5%, with the aggregate expanding at an annualised rate of 3.2% in the latest three months – see chart 1.

Chart 1

The Bank publishes an industrial breakdown of sterling deposits at commercial banks. The LDI cash-raising is reflected in large monthly increases in deposits of insurance companies, pension funds, fund managers and securities dealers (LDI funds posted margin to dealers, with the dealers placing the funds with banks). This group added a combined £39 billion to sterling deposits in September.

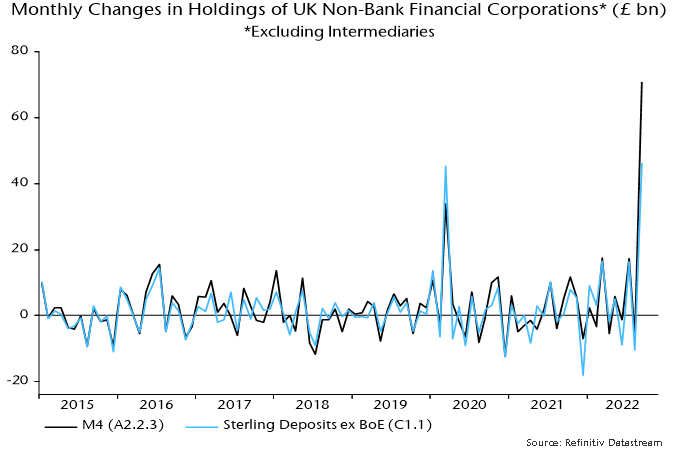

However, the rise in aggregate deposits of non-financial corporations, according to this table (C1.1), was £46 billion in September – far short of the £71 billion increase in their total M4 holdings (A2.2.3). This represents a record divergence – chart 2.

Chart 2

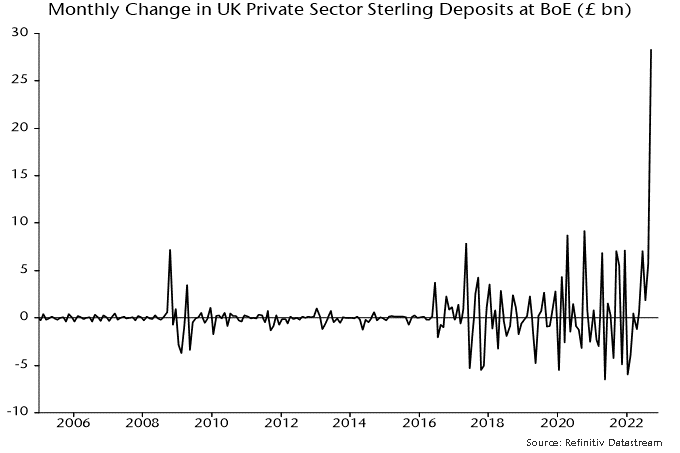

The “missing” funds show up on the Bank’s balance sheet: private sector sterling deposits held at the Bank jumped by £28 billion in September (B2.2.1), also a record movement – chart 3.

Chart 3

Securities dealers and clearing houses have accounts at the Bank, which they appear to have used to deposit a portion of the margin cash received from LDI funds.

Note that this increase in deposits is not attributable to the Bank’s gilt-buying operation, which started on 28 September: the Bank’s holdings of public sector securities fell by £5 billion during September.

Sterling cash-raising related to the LDI crisis may have totalled about £67 billion – the sum of the £39 billion increase in commercial bank deposits of insurance companies, pension funds, fund managers and dealers and the £28 billion placed at the Bank.

LDI funds were also scrambling to raise foreign currency liquidity. The rise in foreign currency deposits of the same group of institutions rose by £25 billion in September.

Not all the cash-raising represents sales of assets – LDI funds were also borrowing to meet margin requirements. Sterling bank lending to the same group rose by £16 billion in September, with foreign currency lending up by £18 billion.

Was the Bank involved in facilitating the supply of liquidity to the funds, over and above its gilt-buying operation? It is unlikely to have played a direct role but banks may have borrowed from its discount window to onlend to LDI funds.

This possibility is suggested by partial data on the Bank’s sterling liabilities and assets – it no longer publishes a full balance sheet on a timely basis. Identified sterling liabilities, including bank reserves and the sterling deposits referred to earlier, rose by £14 billion, while assets – including gilt holdings – fell by £6 billion. The implication is that unpublished items on the balance sheet resulted in the creation of £21 billion of identified sterling liabilities, with discount window lending a candidate explanation.

*Excluding intermediaries such as central clearing counterparties.