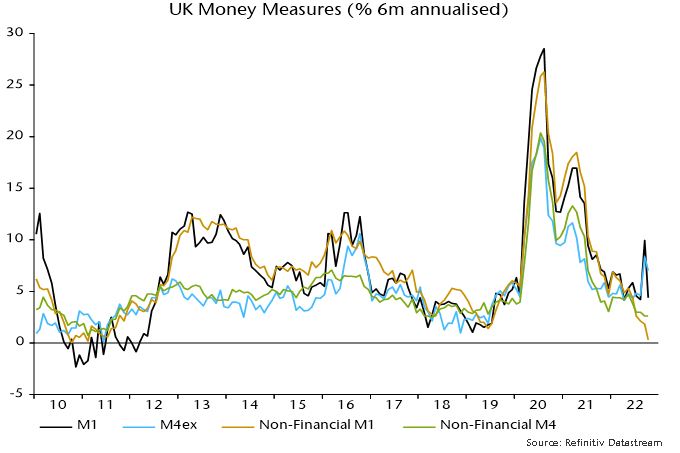

UK money data also weak ex. LDI effect

UK money trends remain consistent with inflation normalisation, implying that further MPC tightening will unnecessarily prolong and deepen the recession.

The artificial boost to headline money numbers from cash-raising by LDI funds partially unwound in October – the Bank of England’s M4ex measure fell by 0.6% on the month after a 2.6% September jump.

As usual, the focus here is on non-financial money measures, i.e. excluding volatile and uninformative financial sector holdings. The September surge in financial money was certainly no signal of future economic or inflation strength.

Annual growth of non-financial M4 was little changed at 3.4% in October, with the six-month annualised pace of increase lower at 2.7%. Annual non-financial M1 growth dropped to 2.6%, with the aggregate little changed in the latest six months – see chart 1.

Chart 1

The latter weakness reflects households and non-financial firms switching out of sight into time deposits in response to higher term interest rates. The decision to lock away money is a negative economic signal, indicating weak near-term spending intentions.

Broad money growth of 3-3.5% is unlikely to be sufficient to prevent inflation from falling below 2% over the medium term, unless potential economic expansion is even weaker than the generally assumed 1-1.5% pa. (This assumes no rise in velocity, which has exhibited a long-term downward trend, including during the 2010s.)

Non-financial M4 is growing more slowly than the comparable Eurozone aggregate, non-financial M3, which rose by 4.8% in the year to October.

The argument continues to be made that spending will be supported by the deployment of “excess” savings built up in 2020-21. The assessment of “excess” need to take into account inflation – fast price rises require more saving to maintain the real value of existing wealth.

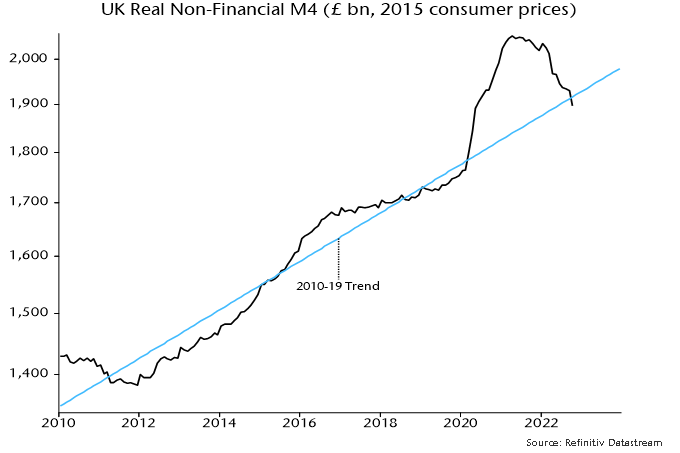

Real non-financial M4 has now crossed beneath its 2010-19 trend – chart 2. The suggestion is that money holdings are broadly in line with requirements given recent high inflation – there is no longer any buffer to cushion spending against an ongoing real money squeeze.

Chart 2