UK inflation forecast update: more upside surprises in H2

The sharp rise in UK CPI inflation to 2.1% in May supports the long-standing forecast here of a move above 3% in late 2021.

The 2.1% outturn compares with a 2.0% forecast in a post a month ago but there were bigger surprises within the detail. Core inflation – excluding food, energy, alcohol and tobacco – jumped from 1.3% in April to 2.0%. This was partly offset by unexpected further weakness in food prices, which posted a 1.2% annual fall, up from 0.5% in April.

This is an unfavourable combination because the rise in core prices is more likely to stick, with food prices expected to pick up into 2022.

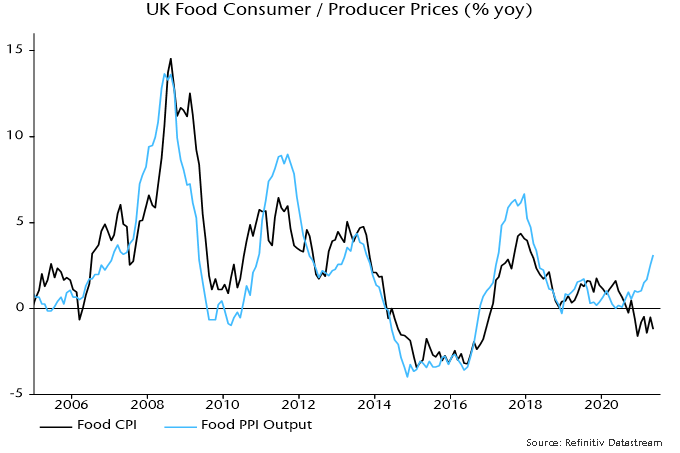

A food rebound is already evident in producer output price inflation for food products, which rose to 3.1% in May and correlates with / leads CPI food inflation – see chart 1,

Chart 1

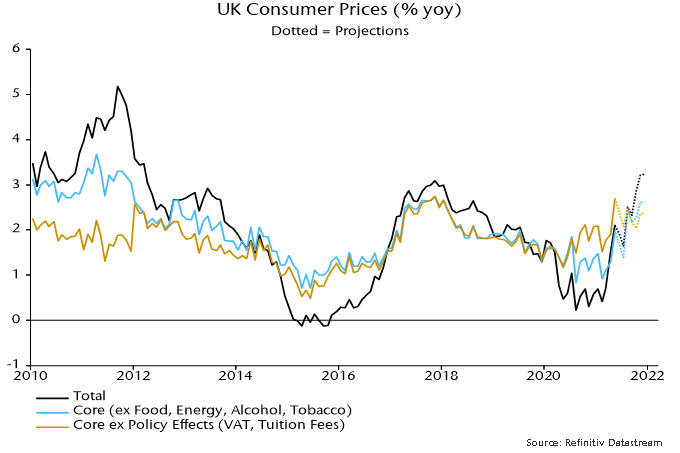

Headline / core inflation rates are still being suppressed by last year’s VAT cut for hospitality, which is due to be reversed in two stages starting in October. The guesstimate here is that core inflation would be 2.7% in the absence of the cut, based on an assumption of 35% pass-through to consumers.

The revised forecasts shown in chart 2 incorporate one-third of the upside core surprise in May, attributing the remainder to temporary “noise” – this may prove overoptimistic. As before, annual food inflation is assumed to rise to 2.0% by year-end. The previous energy price assumptions are also maintained.

Headline / core rates fall back in June / July because of base effects but rises resume thereafter, with headline inflation reaching 3.2% in November / December.

Chart 2

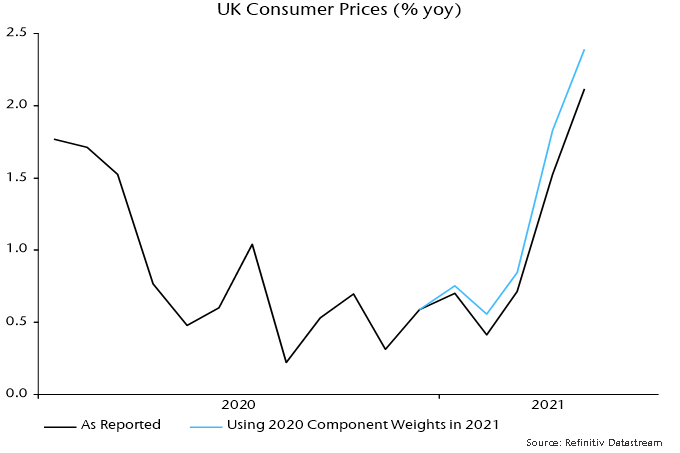

It should be noted that the end-2020 basket reweighting has had the effect of suppressing recorded inflation in 2021. The new weights reflect spending patterns during the pandemic but expenditure shares are normalising as the economy reopens, with an associated shift in relative prices.

The CPI weight of restaurants and hotels, for example, was cut from 11.9% in 2020 to 8.7% in 2021 but the price index for the sector rose by 3.4% between December 2020 and May, more than double a 1.5% rise in the overall CPI. The cut in the weight also implies that the VAT reversal will have a smaller CPI impact than last year’s reduction.

An alternative approach, which may better reflect consumer experience, is to reuse the 2020 basket weights, based on 2018 spending shares, for the 2021 index calculation. The alternative measure rose by 1.7% between December and May, with its annual increase at 2.4% versus the official 2.1% – chart 3.

Chart 3