UK credit crunch arguing for QT cancellation

Recent dramatic tightening of UK credit conditions along with Bank of England plans for large-scale QT and a “significant” rate hike could tip current weak broad money growth over into contraction, in turn threatening a deflationary depression.

To recap, the preferred broad measure here – non-financial M4, comprising sterling money holdings of households and private non-financial firms – grew at an annualised rate of just 0.8% in the three months to August.

The Bank’s broad measure, M4ex, also includes money holdings of financial institutions, which may rise sharply in September / October, reflecting pension funds’ “dash for cash”. Any such strength is not expansionary / inflationary, increasing the importance of focusing on non-financial money measures.

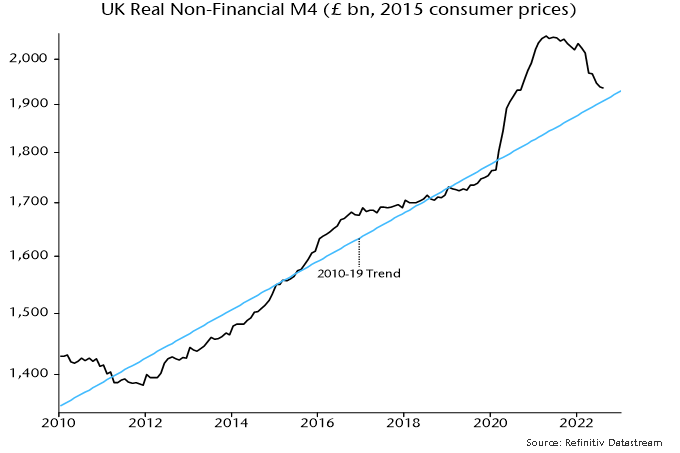

In real terms, non-financial M4 has retraced almost back to its pre-pandemic trend as the 2020-21 money surge has passed through to prices – see chart 1. There is no longer a monetary “excess” to support spending or sustain high inflation.

Chart 1

Current monetary weakness will take time to be reflected in slower price momentum. Prices may continue to outpace nominal money expansion near term, sustaining the real-terms squeeze.

How likely is it that nominal broad money will begin to contract?

The “credit counterparts” analysis links movements in broad money to changes in four other components of the banking system’s balance sheet: lending to the public and private sectors, net overseas assets and non-deposit funding.

Lending to the public sector includes QE / QT. The Bank plans to reduce its gilt holdings by £80 billion over the next 12 months, equivalent to 3.4% of non-financial M4.

The monetary drag will be smaller to the extent that there is a compensating rise in commercial banks’ gilt holdings. Banks bought £13 billion of gilts in the year to August. Purchases reached a maximum 12-month rate of £50 billion in the wake of the GFC when banks were under strong regulatory pressure to boost their liquid assets. A plausible scenario is that banks will absorb between a third and a half of the QT supply, in which case lending to the public sector would have a contractionary impact on broad money of 1.7-2.2% over the next 12 months.

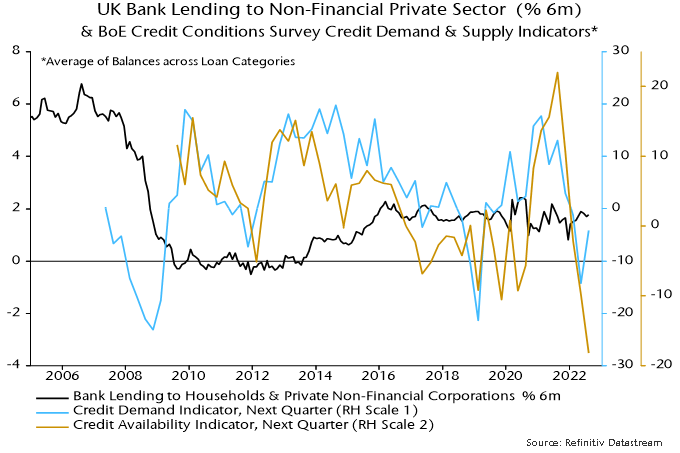

Bank lending to the private sector has been supporting broad money growth recently: lending to households and private non-financial firms expanded at a 3.1% annualised rate in the three months to August. The Bank’s Q3 credit conditions survey, released yesterday, signals weakness ahead: future credit demand balances remained soft while availability plunged – chart 2.

Chart 2

The survey closed on 16 September so does not capture the further surge in market rates and spreads in the wake of the mini-Budget.

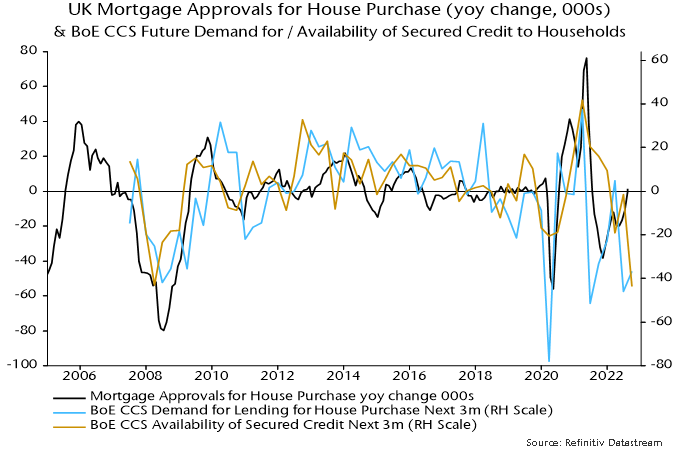

Residential mortgages account for 70% of the stock of lending to households and non-financial firms. The future demand and availability balances for secured credit to households last quarter were comparable with the lows reached at the depths of the GFC – before recent turmoil. Mortgage approvals could halve – chart 3.

Chart 3

Bank lending expansion, therefore, could plausibly grind to a halt, as it did in the wake of the GFC. The combined monetary impact of public and private sector lending would then become contractionary.

The other credit counterparts – banks’ net overseas assets and their non-deposit funding – are volatile and difficult to forecast but have had a combined contractionary impact over the last 12 months. The joint influence, however, tends to correlate inversely with lending to the private sector, so could become supportive as lending weakens.

The “best case” scenario appears to be weak broad money expansion with a significant risk of contraction.

The warranted policy response is to cancel QT and rate hikes. The Bank, instead, has boxed itself into a restrictive stance in a misguided effort to rebuild its shattered credibility and avoid a charge of “fiscal dominance”.

The hope is that a government U-turn on the mini-Budget together with an easing of global interest rate pressures result in a reversal of recent market-driven credit tightening. A Bank policy shift is coming but may have to wait for evidence of sharply contracting economic activity.