SVB is a casualty of QT-driven monetary contraction

Markets are moving towards the view that the Fed will be forced to suspend or reverse interest rate hikes in response to the SVB crisis but a cessation of QT is a more important requirement for restoring banking system stability.

QT also caused the 2019 repo rate crisis, which ended only after the Fed restarted securities purchases (Treasury bills) – portrayed, of course, as a “purely technical” measure rather than a return to QE.

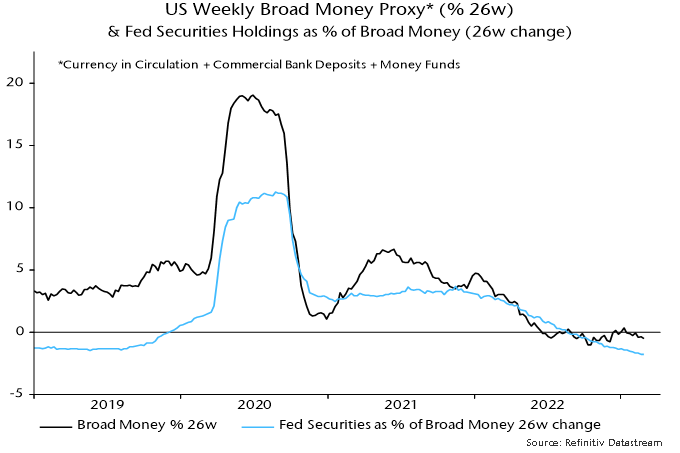

The US weekly broad money proxy calculated here has contracted since April 2022. Weakness initially reflected the US Treasury “overfunding” the federal deficit to rebuild its cash balance at the Fed. QT has been the driver more recently – see chart 1.

Chart 1

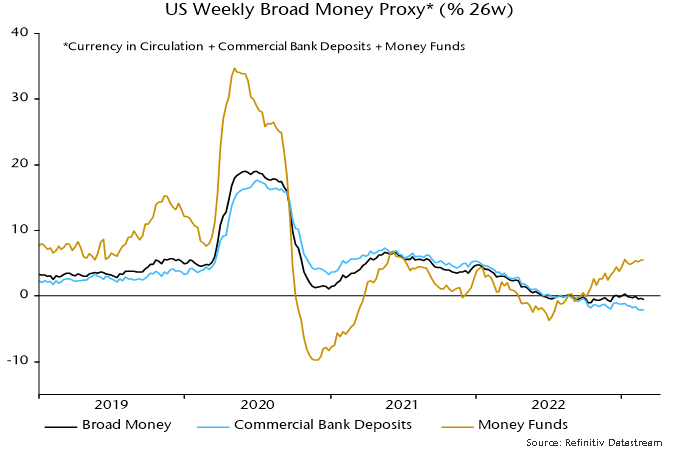

The drain of deposits from commercial banks has been magnified by competition from money market funds, which are able to place overnight funds with the Fed at an interest rate (currently 4.55%) within the Fed’s target range for the Fed funds rate (4.5-4.75%).

Balances in retail and institutional money funds grew by 5.5% (11.3% at an annualised rate) in the latest 26 weeks, while commercial bank deposits contracted by 2.2% (4.4% annualised) – chart 2.

Chart 2

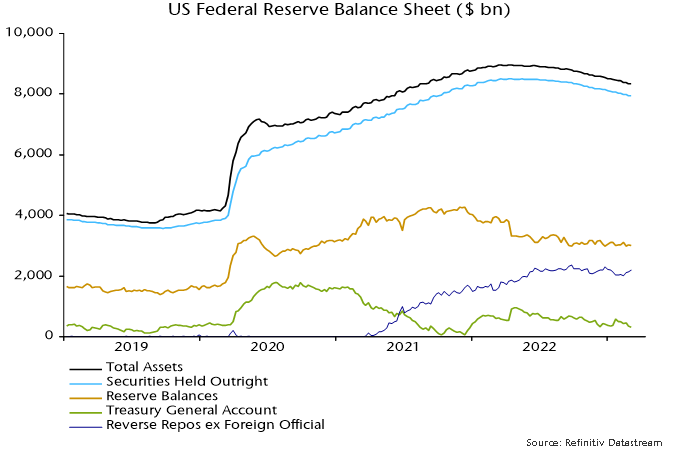

In combination, Treasury overfunding, QT and outflows to money funds have resulted in a 30% decline in banks’ reserve balances at the Fed from a peak in December 2021 – chart 3.

Chart 3

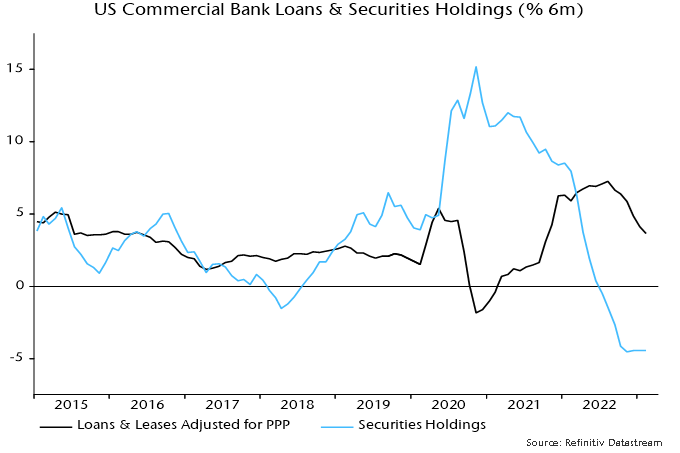

The deposits / reserves drain has caused banks to sell securities and, more recently, restrict loan supply – chart 4.

Chart 4

The new Bank Term Funding Program will allow banks to avoid selling securities at a loss but fails to address the system-wide loss of deposits due to QT. The Fed facility, moreover, is more expensive than the deposits it may replace.

Fortuitously, downward pressure on broad money has recently been relieved by a run-down of the Treasury’s cash balance at the Fed, reflecting the debt ceiling impasse. The decline, indeed, may have been accelerated to inject liquidity into the banking system – the balance fell from $345 bn to $247 bn between Wednesday and Friday last week.

Such relief, however, is temporary. The authorities’ actions to date may be sufficient to avert another bank collapse but the banking system will remain under pressure, with negative economic implications via rising deposit / lending rates, until QT-driven monetary contraction ends.