Slowdown forecast maintained, January money data in focus

The global economic slowdown signalled by monetary trends appears to be playing out. The global manufacturing PMI new orders index fell to an 18-month low in January and is now 5.1 points below a May peak – see chart 1.

Chart 1

A decline in global six-month real narrow money growth into November suggests a further PMI fall into mid-year, at least, allowing for a typical 6-7 month lead. Real money growth recovered marginally in December but could weaken again in January – a provisional number will be available by early next week. Eurozone growth is likely to have turned negative based on last week’s CPI data, showing a further spike in six-month momentum.

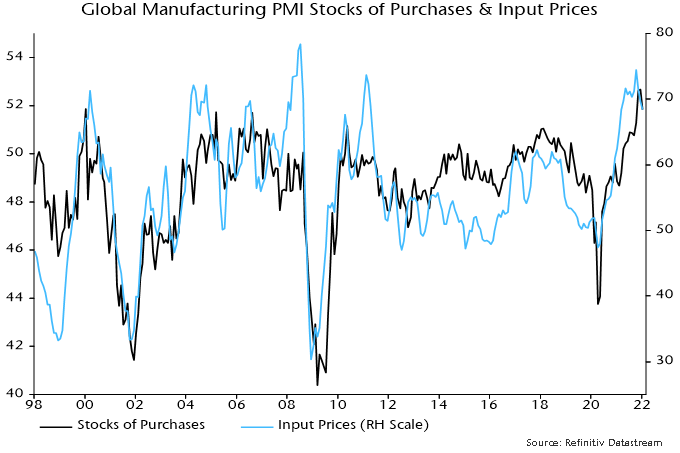

The manufacturing PMI stocks of purchases index reached a record level in December but fell back in January, consistent with the view here that the stockbuilding cycle has peaked and is about to enter a 12-18 month downswing phase. The coming inventory slowdown (and eventual liquidation) is likely, as usual, to be associated with a significant weakening of goods price pressures – chart 2.

Chart 2

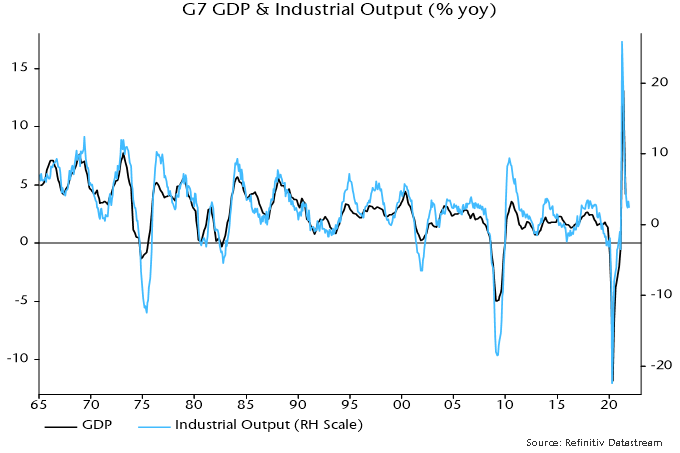

Optimists argue that services strength as pandemic disruption ends will outweigh any industrial slowdown. The (Keynesian) understanding here is that economic fluctuations are driven by goods spending and investment in particular. GDP growth swings mirror those in industrial output: the correlation coefficient of year-on-year changes was +0.89 over 1965-2020 – chart 3. There is no independent cycle in services demand. A services rebound as conditions normalise is likely to burn out swiftly if the industrial slowdown deepens.

Chart 3

The supposedly “blow-out” US jobs report has no implication for the assessment here, except to increase the likelihood of a Fed policy mistake. Labour market data are not forward-looking and the details of the report were much less impressive than the headlines.

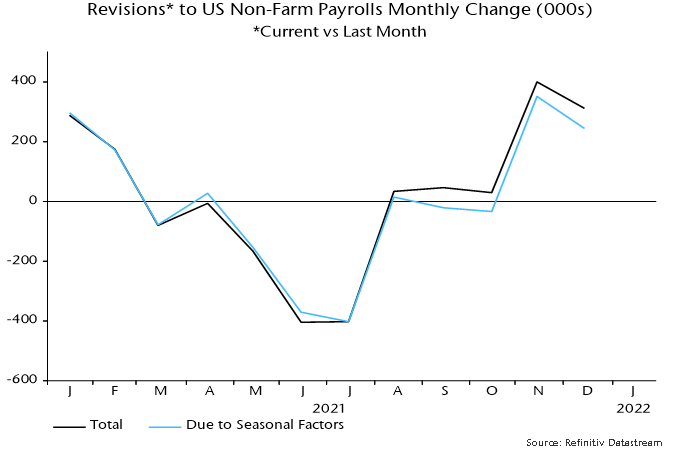

Huge upward revisions to November / December payrolls growth reflected new seasonal factors, with offsetting downgrades to June / July numbers – chart 4

Chart 4

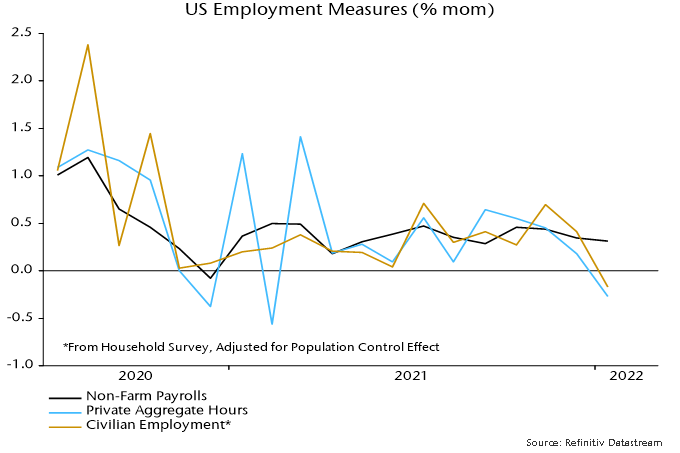

Payrolls rose solidly in January (with a boost from the new seasonal factor) but pandemic disruption showed up in falls in aggregate hours and the household survey employment measure – chart 5.

Chart 5

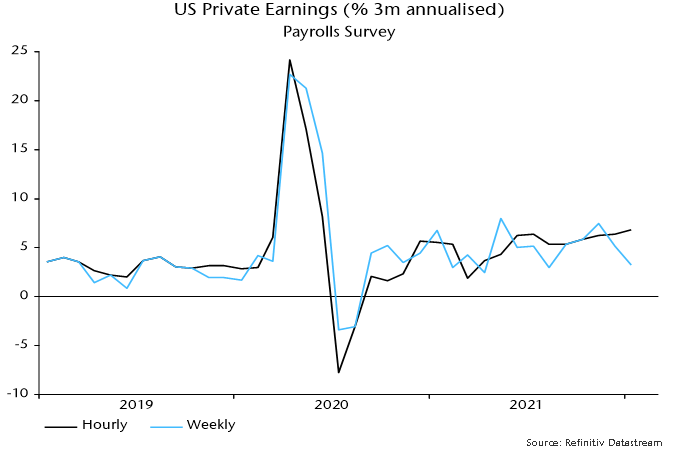

The drop in weekly hours may explain the larger-than-expected hourly earnings increase, assuming that lower-earners were more likely to have their hours cut. Weekly earnings growth remains range-bound – chart 6.

Chart 6

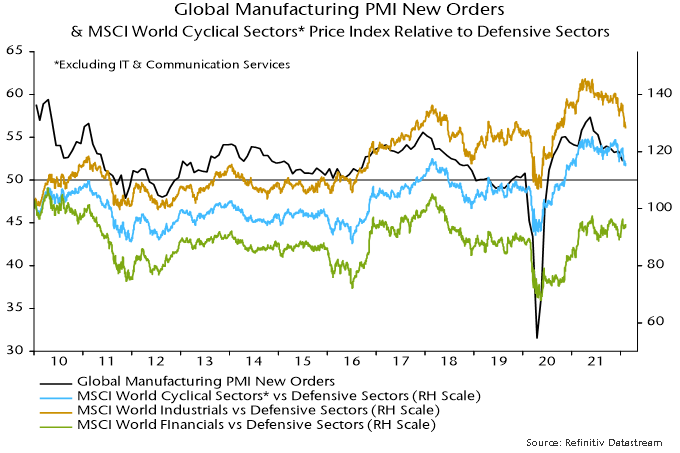

The PMI fall has been reflected in underperformance of MSCI-defined cyclical sectors versus defensive sectors but there is significant variation within the groupings, most notably the continued strength of financials – chart 7.

Chart 7

This resilience, of course, reflects rising bond yields and is likely to fade if waning economic momentum and easing price pressures pull these lower.

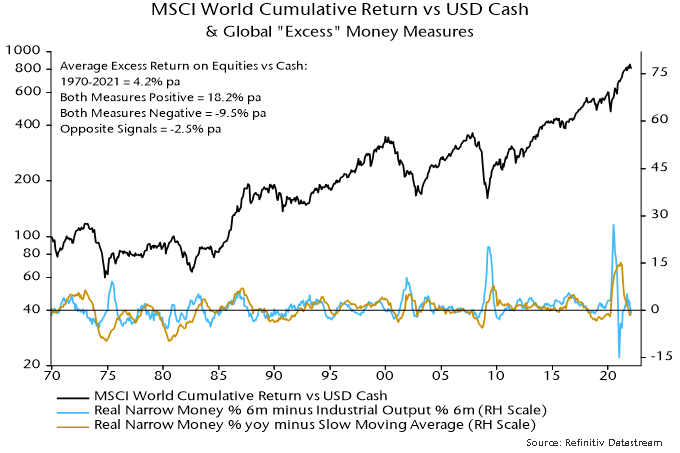

The view here remains that the rise in bond yields – like the outperformance of value versus growth – reflects a less favourable monetary backdrop for markets rather than a reprise of the “reflation trade”. Both “excess” money measures tracked here remain negative – chart 8.

Chart 8