Should the BoE tighten policy “significantly”?

Bank of England Chief Economist Huw Pill has suggested that fiscal policy easing in the mini-Budget and the reaction in markets warrant a “significant monetary policy response”. Why?

UK monetary trends continue to weaken and are consistent with a medium-term return of inflation to target, if not below.

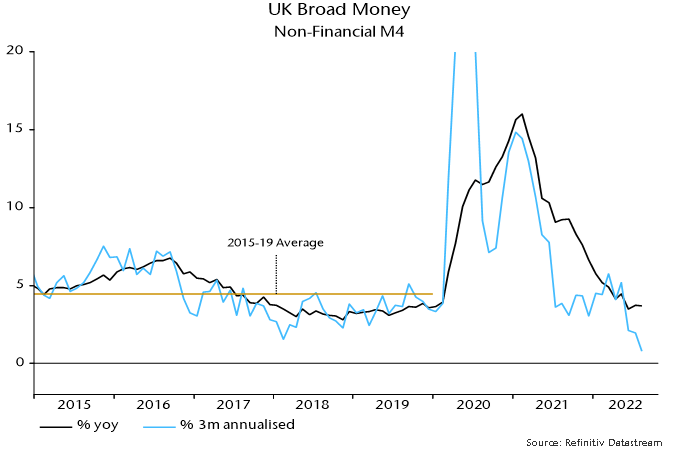

Annual growth of non-financial M4 – the preferred broad aggregate here, comprising holdings of households and private non-financial firms – was unchanged at 3.7% in August, below an average of 4.4% over 2015-19. The three-month rate of expansion fell further to just 0.8% annualised – see chart 1.

Chart 1

Should the Bank tighten to offset the inflationary impact of exchange rate weakness? The “monetarist” view is that currency movements can delay or speed up the transmission of monetary changes to prices but have no longer-term inflation impact as long as money growth is stable.

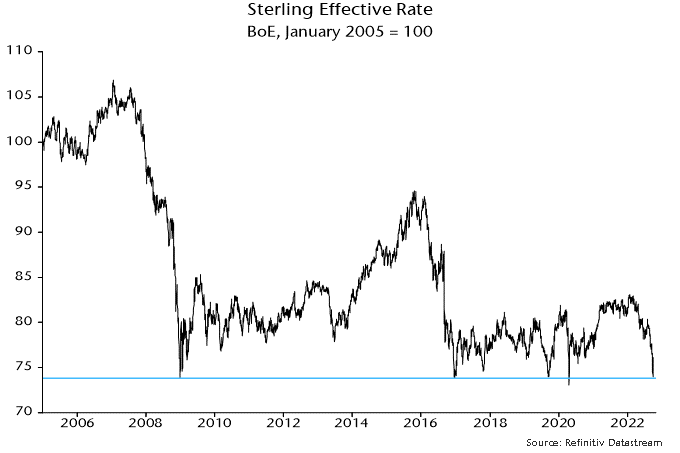

The sterling effective rate index was down by 10% on a year before at last week’s low point but the annual change reached -25% during the GFC and -19% after the Brexit referendum. The index hasn’t (yet) broken below its GFC low – chart 2.

Chart 2

The greater concern here is that increased government borrowing will be financed significantly through the banking system, resulting in another boost to money growth. This could occur via voluntary purchases of gilts by commercial banks in response to higher yields or because the Bank is forced to offer sustained support to a dysfunctional market.

Such a scenario, however, is possible rather than likely. Any monetary boost from deficit financing could be offset or outweighed by a further weakening of private sector credit trends as banks pass on higher funding costs and widen spreads.

The Bank would have made better recent decisions if it had paid attention to monetary trends: it wouldn’t have expanded QE in November 2020, would have raised rates earlier in 2021 and wouldn’t have embarked on QT. Current monetary weakness argues against policy tightening. The Bank may judge it necessary to hike rates to bolster its credibility, and that of the wider UK policy-making framework. Bank officials, however, should avoid inflating market expectations and be prepared to reverse increases if markets calm and – as seems likely – money trends remain soft.