Why is US narrow money accelerating?

A pick-up in US narrow money momentum is a hopeful signal for 2025 but requires confirmation and does not preclude near-term economic deterioration.

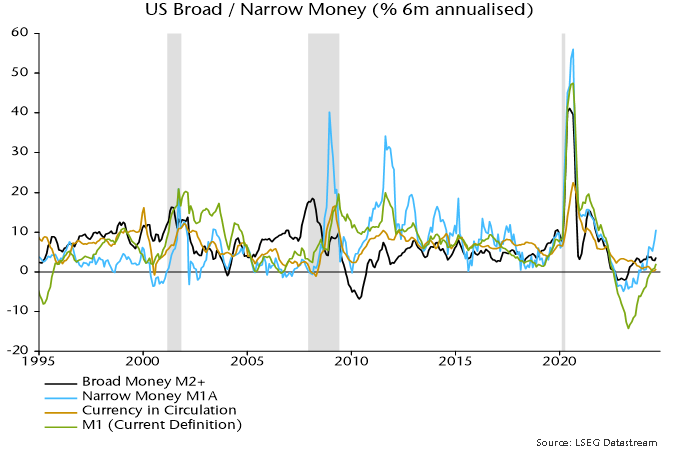

The measure of narrow money tracked here (M1A, comprising currency in circulation and demand deposits) rose by 0.8% in August, pushing six-month annualised growth up to 10.5% – see chart 1.

Chart 1

The broad M2+ measure (which adds large time deposits at commercial banks and institutional money funds to the official M2 aggregate) also rose solidly in August, by 0.5%, but six-month growth remains subdued and within the recent range, at 3.5% annualised.

Six-month expansion of official M1 is weaker, at 2.1%. M1 is no longer a narrow money measure, following its redefinition in 2020 to include savings accounts.

Narrow money outperforms broad as a leading indicator of economic direction. The recent pick-up suggests that demand and activity will be gaining momentum by mid-2025. It does not, however, preclude – and may be consistent with – current economic deterioration.

Six-month narrow money momentum similarly recovered from negative to 10% annualised in September 2001 and September 2008. In both cases, the economy was within a recession that the NBER had yet to recognise.

Those narrow money rebounds may have partly reflected a rise in liquidity preference associated with an increase in saving, i.e. they may have been a signal of a reduction in current demand. They also, however, implied potential for future economic reacceleration when liquidity preference normalised and money balances were redeployed.

The 2001 / 2008 experiences were atypical: in earlier recessions, six-month narrow money growth rose strongly only at the end of – or after – the period of economic contraction.

A reasonable assessment, therefore, is that a pick-up in narrow money momentum is a neutral or negative signal for current economic momentum but positive for prospects six to 12 months ahead.

The current positive message is tempered by several considerations.

First, six-month momentum is likely to fall back in September / October because of negative base effects: narrow money rose by a whopping 3.1% (20.0% annualised) in March / April combined.

Secondly, the currency and demand deposit components of narrow money have been individually correlated with future activity historically but the recent pick-up has been solely due to the latter, with currency momentum unusually weak – chart 1.

Thirdly, the Fed funds target rate had been cut by 350 bp and 325 bp respectively by the time six-month narrow money momentum reached 10% annualised in 2001 and 2008. The Fed’s tardiness has increased the risk of a monetary relapse.