OECD US leading indicator signalling weaker outlook

A post in June suggested that a recovery in the OECD’s US composite leading indicator was ending. A calculation based on the latest input data confirms a reversal lower.

The historical performance of the OECD indicator compares favourably with the Conference Board leading index. The OECD indicator recovered from early 2023, signalling that recession risk was (temporarily?) receding, while the Conference Board measure continued to weaken.

The latest published data point, for June, was released in early July. The next update is due on 5 September and will provide July / August numbers.

Chart 1 shows the published series (black), a replica series calculated here based on data available in early July (blue) and an updated replica incorporating an additional month of input data (gold). The updated series has fallen sharply from an April peak.

Chart 1

The decline reflects weakness in four components: consumer sentiment, durable goods orders, the manufacturing PMI and housing starts. The two financial components – stock prices and the 10-year Treasury yield / fed funds rate spread – were still marginally positive in July but levels so far in August imply a turn lower.

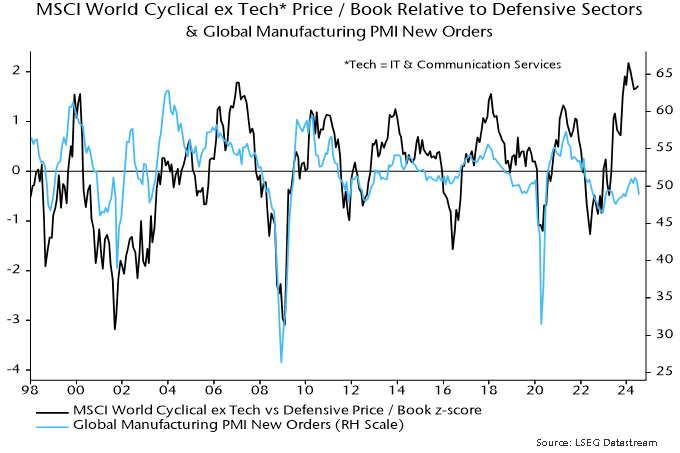

The price relative of MSCI World cyclical sectors, excluding tech, versus defensive sectors has mirrored movements in the OECD US leading indicator historically – chart 2. Relative valuation is high versus history and has diverged from a weakening global manufacturing PMI – chart 3.

Chart 2

Chart 3