Is the ECB still too pessimistic on Eurozone inflation?

Monetary considerations argue that the ECB’s latest inflation forecast, like earlier projections, will be undershot.

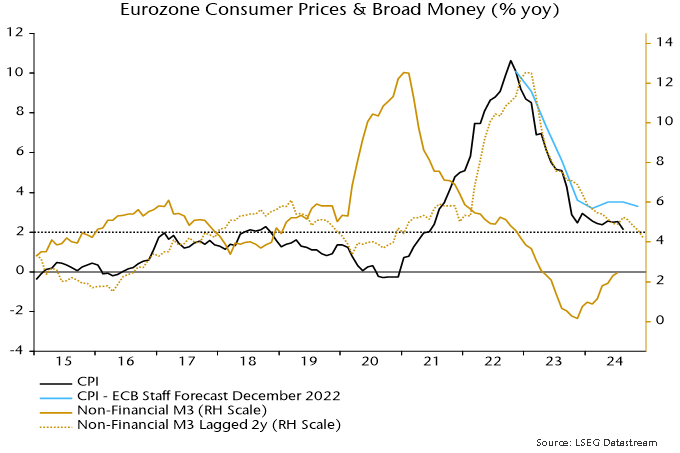

Annual growth of broad money – as measured by non-financial M3 – returned to its pre-pandemic (i.e. 2015-19) average of 4.8% in October 2022. Allowing for a typical two-year lead, this suggested that annual CPI inflation would return to about 2% in late 2024 – see chart 1. The August reading was 2.1% (ECB seasonally-adjusted measure).

Chart 1

The ECB staff forecast in December 2022 was more pessimistic, projecting annual inflation of 3.3% in Q4 2024. The forecast for that quarter was still up at 2.9% in June 2023 after natural gas prices had collapsed.

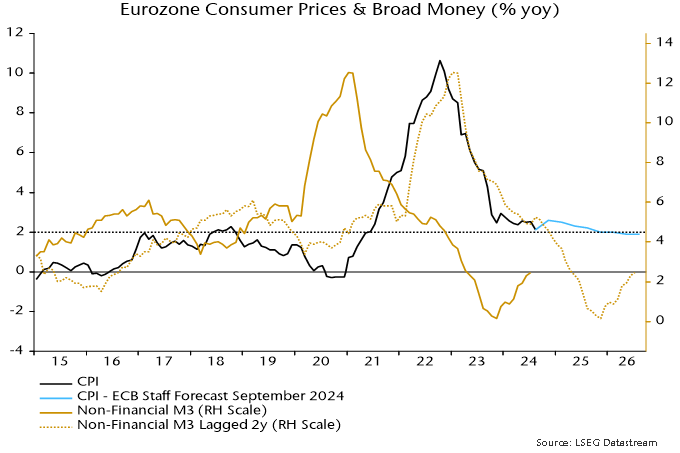

Annual broad money growth continued to plunge in 2023, reaching a low just above zero in November, since recovering to a paltry 2.5%. Simplistic monetarism, therefore, suggests that inflation will move below target in 2025 and remain there into 2026 – chart 2.

Chart 2

The September 2024 ECB staff forecast, by contrast, shows inflation rising in Q4 and remaining above 2% until Q4 2025.

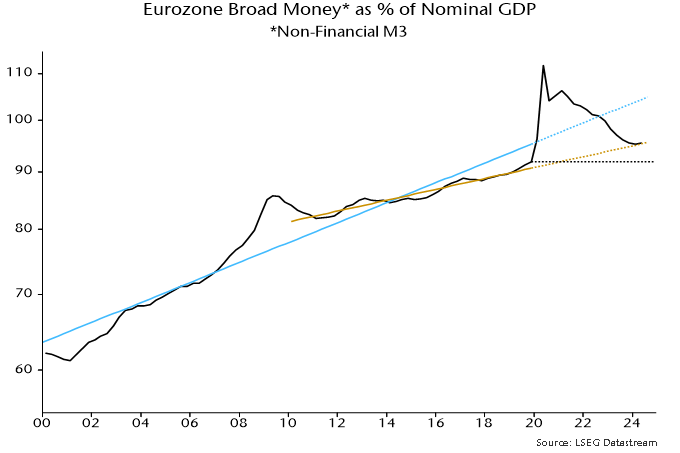

The monetarist relationship, taken at face value, implies a period of annual price deflation in H2 2025 / H1 2026. The judgement here is to downplay this possibility and regard the current monetary signal as directional rather than giving strong guidance about levels.

It is possible that the stock of money is still above an “equilibrium” level relative to nominal GDP. The current ratio is below its 2000-19 trend but in line with the 2010-19 trend, and higher than at end-2019 – chart 3. There may still be “excess” money to act as a deflation cushion.

Chart 3

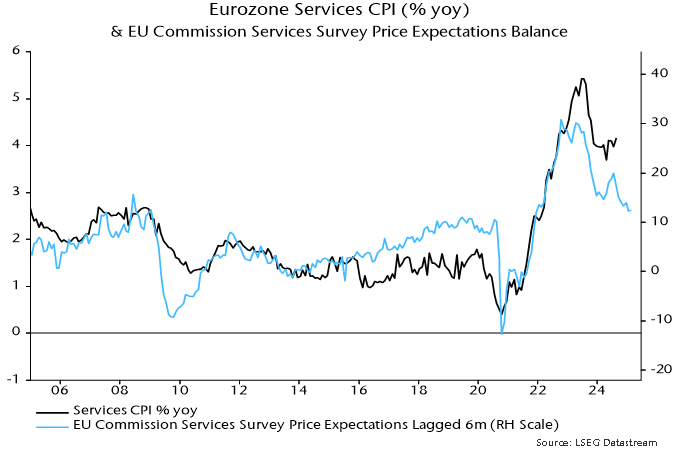

The forecast of a target undershoot requires services inflation – an annual 4.2% in August – to break lower. The price expectations balance in the EU services survey has displayed a (loose) leading relationship with annual services inflation historically, with the current reading consistent with a move down to about 2.5% in H1 2025 – chart 4.

Chart 4