Global “double dip” on track

The assessment here remains that the global economy has entered a “double dip” currently focused on manufacturing but likely to extend to services / labour markets, reigniting worries about a hard landing. Economic weakness is expected to be accompanied by an inflation undershoot into H1 2025.

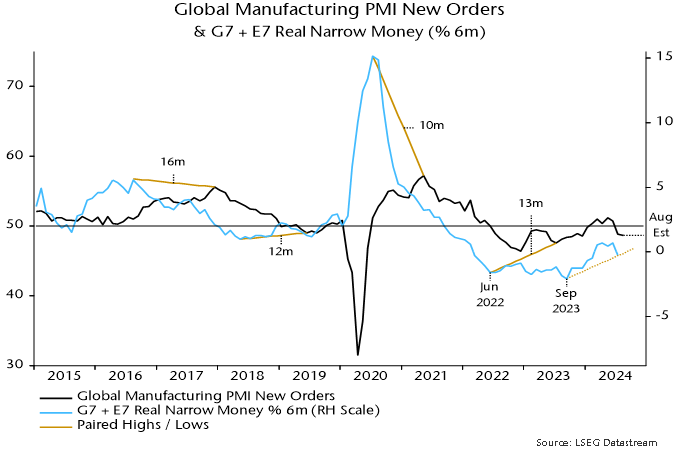

DM flash manufacturing PMI results for August were mixed across countries but on balance weak, suggesting a further small reduction in global manufacturing PMI new orders following a July plunge to below 50 (assuming no change for China and other non-flash countries) – see chart 1.

Chart 1

Services results were again much stronger than for manufacturing but there are hints of emerging weakness in a fall in output expectations since May and a drop in US / Eurozone employment indices to below 50 this month.

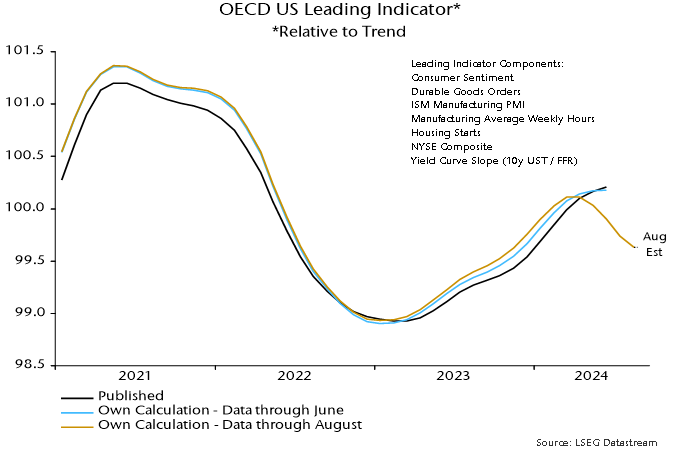

A previous post suggested that the OECD’s US composite leading indicator has reversed lower since publication of the last official data point, for June. An update based on partial data points to a further decline in August – chart 2. The OECD will release July / August data for its indicators on 5 September.

Chart 2

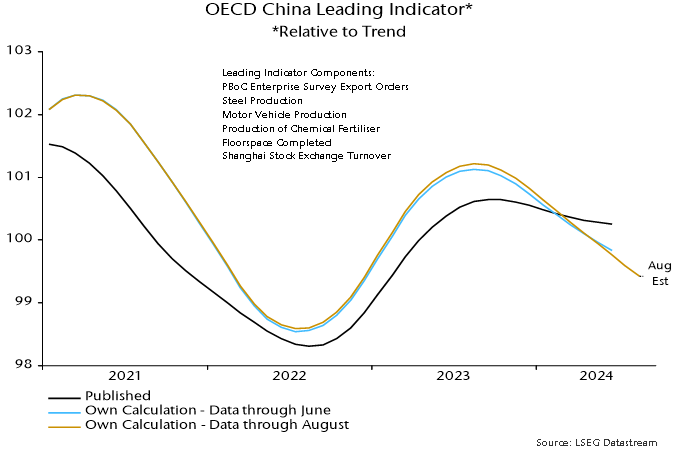

The OECD’s Chinese leading indicator has been falling since late 2023 and the decline is estimated to have continued in July / August – chart 3.

Chart 3

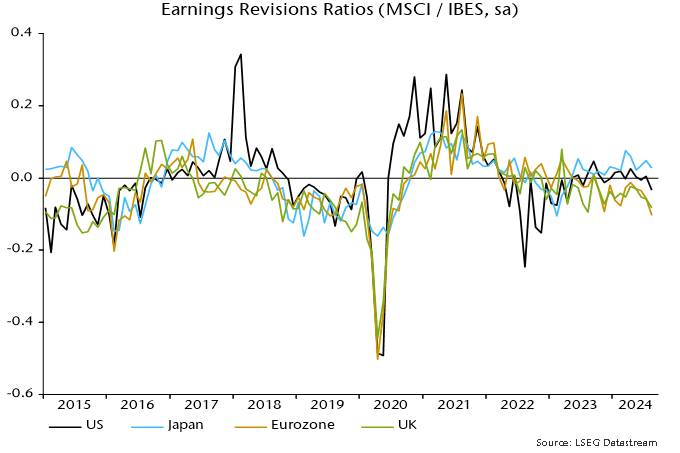

Weaker economic momentum and pricing power are feeding through to company earnings. Revisions ratios have turned down since April in the US, Eurozone and UK, with the August Eurozone reading the weakest since 2020 – chart 4.

Chart 4

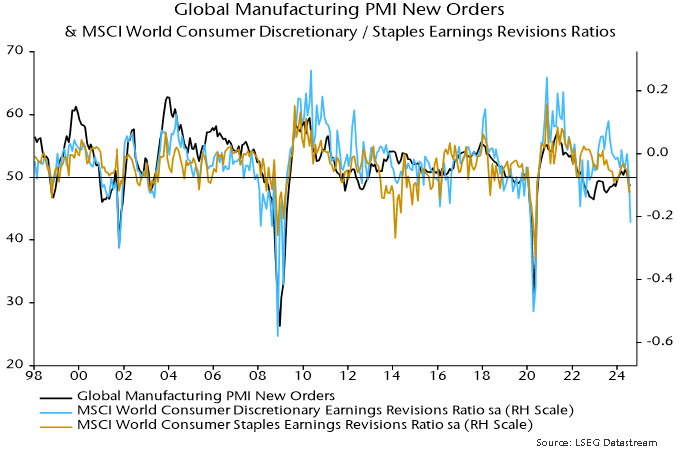

By MSCI World sector, August revisions ratios were most negative in consumer discretionary followed by energy, consumer staples and materials. The ratios for consumer discretionary and staples were the weakest since 2020, suggesting that a fall-off in consumer demand has been a key driver of the renewed downturn in manufacturing – chart 5.

Chart 5

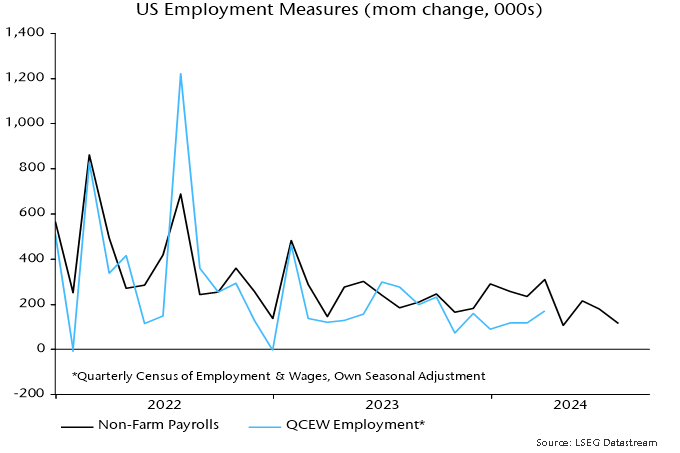

This week’s announcement by the BLS of a preliminary 818,000 or 0.5% downward revision to the March 2024 level of non-farm payrolls, meanwhile, raises the possibility that US employment has already stalled.

The revision is based on the comprehensive Quarterly Census of Employment and Wages (QCEW). A monthly QCEW employment series is available through March but is not seasonally adjusted. Chart 6 compares the monthly change in non-farm payrolls, as currently reported before incorporating the revision, with the change in a seasonally-adjusted version of the QCEW measure.

Chart 6

The increase in non-farm payrolls was 133k per month higher than growth of the seasonally-adjusted QCEW series during Q1. If overstatement of this magnitude has continued since Q1, reported growth of 108k and 114k in non-farm payrolls in April and July could imply small declines in “true” employment in those months.