More recession-consistent US data

Shorter-term leading indicators are confirming the negative signal for US economic prospects from monetary trends.

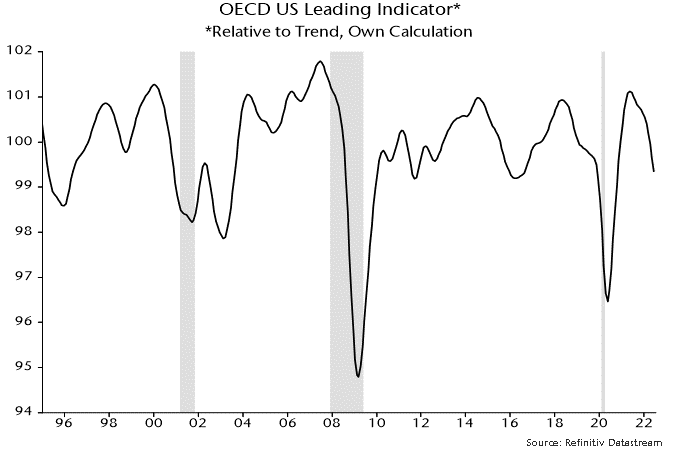

An independent calculation of the OECD’s US composite leading indicator suggests another fall in the indicator in June along with upward revisions to declines in prior months – see chart 1.

Chart 1

The indicator is calculated as a ratio to trend, i.e. a decline indicates that output will lag its trend rate of growth. The extent of the shortfall should be related to the speed of descent of the indicator. The current pace has been consistent with a recession historically.

The June indicator estimate incorporates new information for four of the seven components: housing starts, consumer sentiment, stock prices and the yield spread between 10-year Treasuries and Fed funds. Data for the remaining three – durable goods orders, the ISM manufacturing PMI and average weekly hours worked in manufacturing – will be released on 27 June, 1 July and 8 July respectively.

The indicator’s decline is notable for its breadth as well as speed: all seven components have contributed to recent weakness.

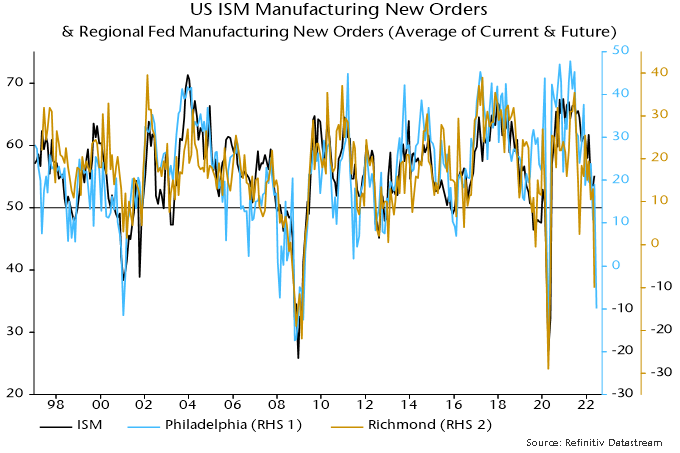

The June indicator estimate assumes little change in the three missing components. The ISM PMI could fall significantly. The Philadelphia Fed manufacturing survey for June reported a plunge in new orders (average of current and future balances), mirroring weakness in May’s Richmond Fed survey and suggesting a crash in the ISM orders index – chart 2. The latter has a 20% weight in the PMI and usually leads the other components.

Chart 2

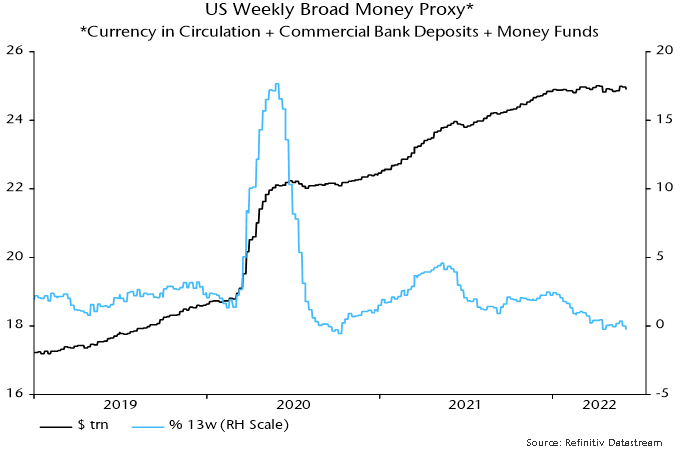

A vicious real money squeeze, meanwhile, is intensifying. A weekly broad money measure calculated here was unchanged in nominal terms in early June from its level at the start of the year – chart 3. With consumer prices up by 4.1% over December-May and expected to post another large rise in June, real broad money will have contracted by about 5% (10% annualised) during H1.

Chart 3