Monetary financing fuels red-hot UK money growth

UK money numbers continued to show absolute and relative strength in February, suggesting a coming domestic demand boom with unfavourable balance of payments and inflation consequences.

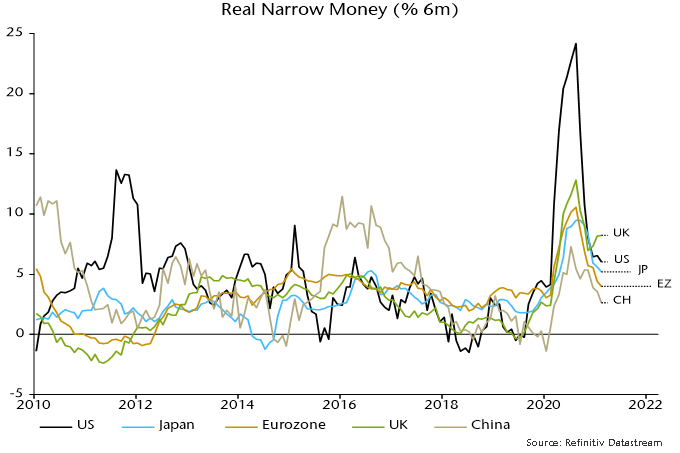

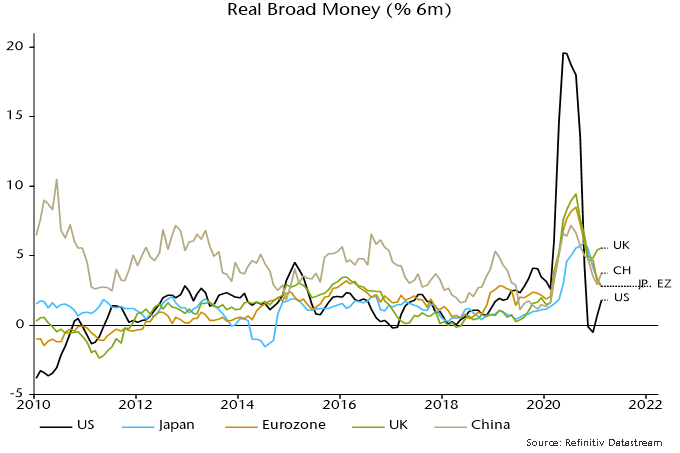

Charts 1 and 2 compare six-month growth rates of real narrow and broad money across economies. The UK tops both rankings, with recent monetary reacceleration contrasting with ongoing slowdowns elsewhere (although US growth is turning up again as stimulus payments enter bank accounts).

Chart 1

Chart 2

The preferred UK broad money measure here – non-financial M4, comprising money holdings of households and private non-financial corporations (PNFCs) – grew by 16.0% in nominal terms in the year to February. The comparable Eurozone measure – non-financial M3 – rose by 12.5%. Annualised growth rates in the latest three months were 14.4% and 9.5% respectively.

The Bank of England’s M4ex broad money measure grew by a slightly lower 15.2% in the year to February, with its annualised rate of increase slowing to 9.7% in the latest three months. M4ex also includes money holdings of financial institutions, which have fallen over the last three months* but are of limited significance for near-term demand prospects.

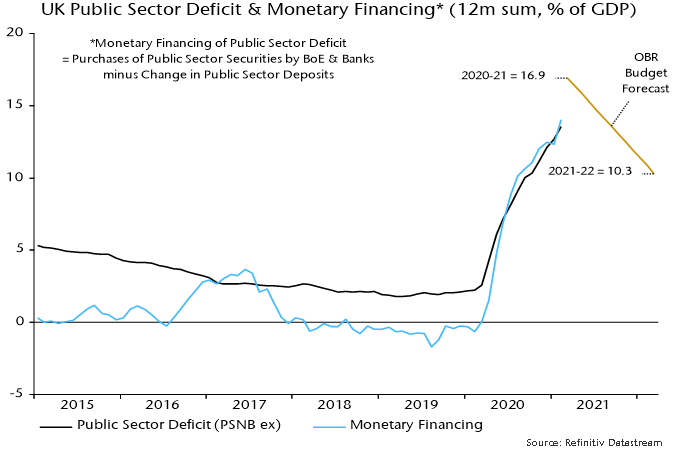

UK broad money strength reflects the large fiscal deficit and its entire financing by money creation, i.e. net sterling lending to the government by the banking system, including the Bank of England – chart 3**.

Chart 3

In 1985 then Chancellor Nigel Lawson introduced the “full funding” rule, which required deficits (and any increase in foreign exchange reserves) to be financed by net debt sales to the UK non-bank private and overseas sectors, implying no public sector contribution to broad money growth. According to this concept there has been zero funding over the last 12 months – domestic and overseas “savers” made no contribution to financing the deficit, which has been mirrored pound-for-pound by an increase in the broad money stock.

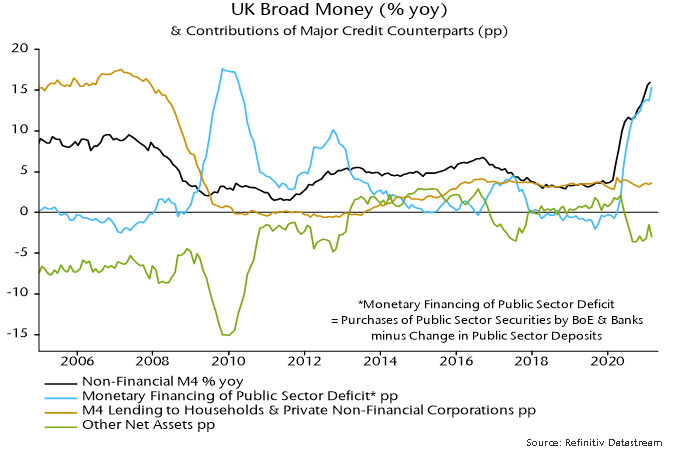

In terms of the “credit counterparts” arithmetic, monetary financing accounted for 15.4 percentage points (pp) of the 16.0% growth of non-financial M4 in the year to February. A positive contribution of 3.6 pp from sterling lending to households and PNFCs was offset by a 3.1 pp drag from other counterparts*** – chart 4.

Chart 4

The chart shows that official money creation made an even larger contribution in 2009-10, reflecting the Bank of England’s post-GFC QE programme. This was, however, needed to offset private money destruction as banks attempted to meet regulatory demands to boost their capital ratios rapidly by contracting their lending and shedding other assets. The net result was low broad money growth and inflation. There is no actual or potential monetary shortage to counteract now, and hence no monetary justification for QE on the current scale.

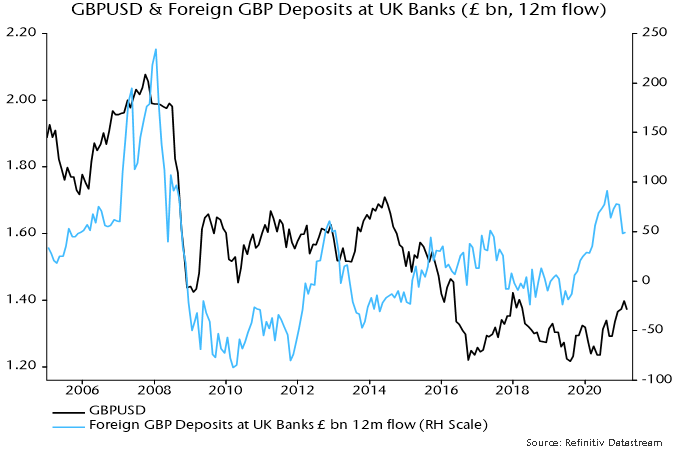

Broad money growth would have been even faster but for a diversion of liquidity into sterling bank deposits of overseas residents – monetary aggregates include deposits of domestic residents only. Overseas deposits grew by £49 bn in the year to February, equivalent to 2.6% of non-financial M4. The recent rise is the largest since before the GFC, when liquidation of the overhang of foreign balances triggered a sharp fall in sterling – chart 5.

Chart 5

Strong domestic demand prospects typically imply upward pressure on the exchange rate as expectations for monetary policy adjust. With central banks now committed to prolonged interest rate suppression, this linkage has been broken. Instead, the prospect of unchecked demand strength suggests a bigger current account deterioration and falling real rates as inflation accelerates. Central banks may be rehabilitating the monetary theory of exchange rate determination, according to which a rise in the relative supply of a currency (in this case sterling) results in depreciation.

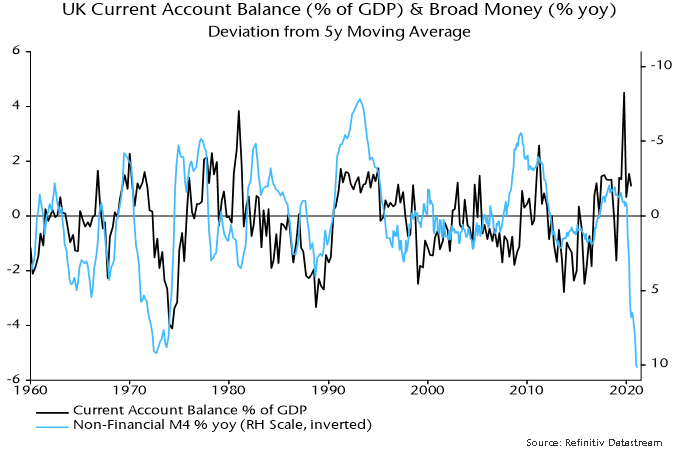

The consensus appears complacent about balance of payments risks: the average current account deficit forecast in the Treasury’s monthly survey is £80 bn in 2021 and £84 bn in 2022, essentially unchanged from £74 bn in 2020 (£79 bn excluding trade in precious metals). The view here remains that a major blow-out is possible, based on the historical relationship with broad money growth – chart 6 – and a Brexit hit to the UK’s global export share.

Chart 6

*Due to reductions in sterling bank deposits of fund managers, insurance companies and securities dealers.

**The deficit definition referred to here is public sector net borrowing excluding public sector banks (PSNB ex). The public sector net cash requirement (PSNCR) includes financial transactions and was larger than PSNB ex in the 12 months to February (£330 bn vs £286 bn), mainly reflecting Bank of England lending schemes and the student loan programme. Monetary financing accounted for 90% of the PSNCR over this period.

**Net sterling lending to UK financial institutions plus net overseas and foreign currency lending minus capital and other net non-deposit liabilities.