Is US labour market resilience about to crumble?

Revised numbers confirm that US GDP fell by 0.6% (1.1% annualised) between Q4 2021 and Q2 2022*. Hours worked in the private sector economy, meanwhile, climbed 1.1% (2.2% annualised) over the same period. What explains this disconnect and how long can it continue?

The ”explanation” here is that economy-wide productivity was pushed far above trend by the pandemic but has been normalising this year. The reversion to trend appears complete, suggesting that labour market data will reflect output weakness going forward.

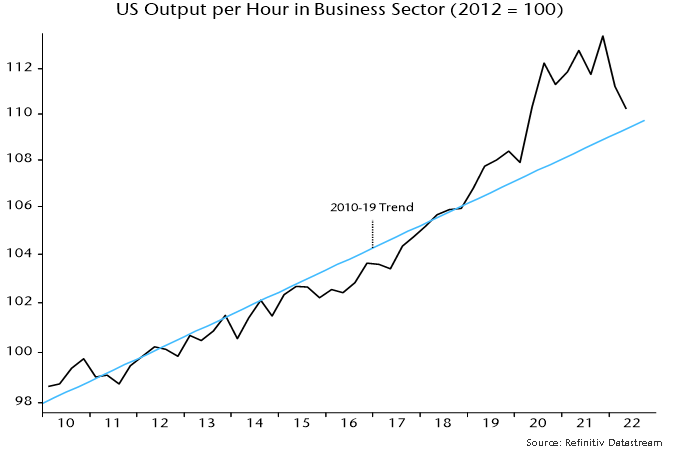

Output per hour in the business sector surged in the initial stages of the pandemic in Q2 / Q3 2000, opening up a gap of more than 4% with the prior trend – see chart 1.

Chart 1

Firms responded to economic contraction by laying off lower-productivity workers, boosting the average. Output returned to its pre-pandemic level in Q2 2021, requiring these jobs to be refilled. A fall in participation (due to age demographics) coupled with supply / demand mismatches slowed the rehiring process, resulting in output per hour remaining elevated until recently.

The deviation from trend had narrowed to below 1% as of Q2.

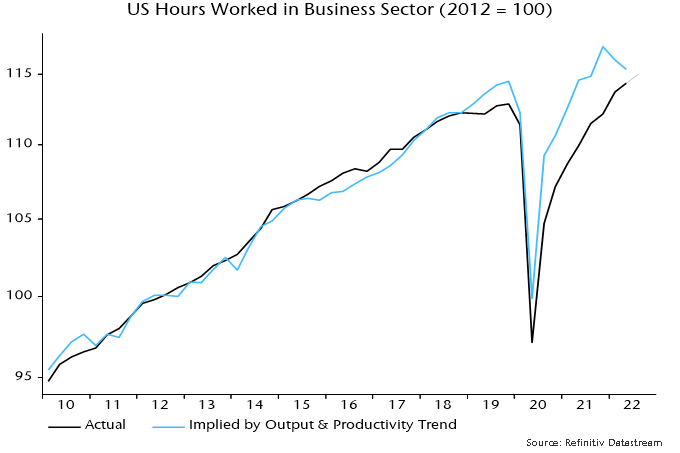

Another way of presenting the data is to compare actual hours worked in the business sector with the number implied by the current level of output, assuming that productivity had continued on its pre-pandemic path – chart 2.

Chart 2

A big deficit had opened up by Q2 2021 but strong employment growth and an output set-back have narrowed the gap. Monthly data through August suggest that hours worked rose solidly again in Q3 and may have converged with the output-warranted level.

With productivity back or close to trend, the GDP / employment divergence is likely ending.

The productivity trend implies that hours worked will fall if GDP rises by less than 0.2% (0.8% annualised) per quarter. Real narrow money has been contracting since January 2022, suggesting further GDP declines in Q4 / H1 2023. Labour market data may be poised for imminent deterioration.

*Gross domestic income – GDP measured from the income side – rose by 0.2% (0.4% annualised) over the same period.