Ignore central bank hysteria: inflation risks are fading fast

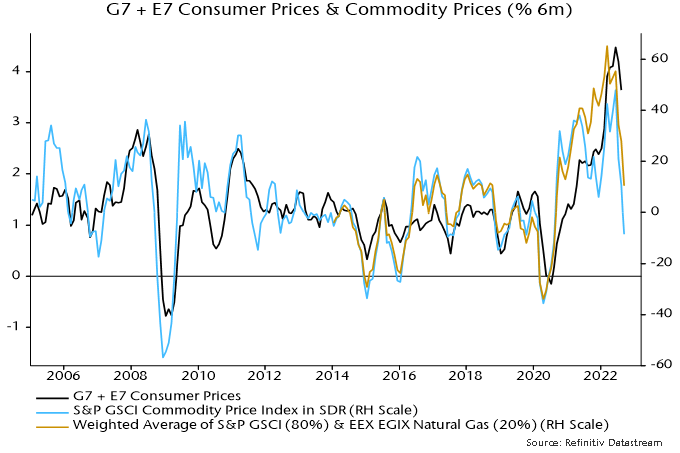

Global six-month consumer price inflation peaked in June and fell further in August, reflecting pass-through of lower oil prices and a small decline in core momentum. Current commodity prices suggest a sizeable further drop into Q4 – see chart 1*.

Chart 1

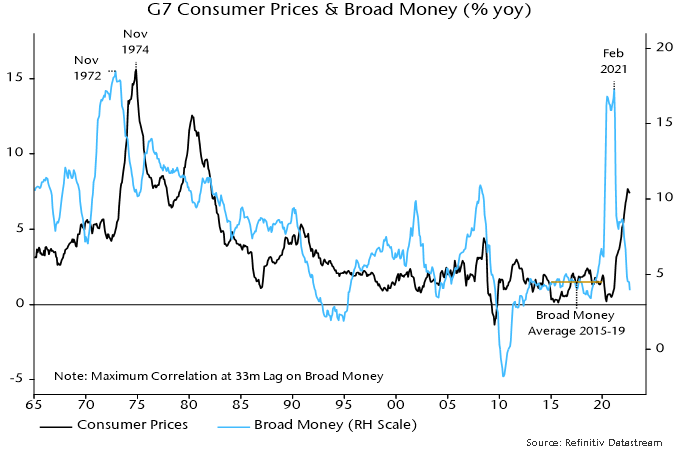

Annual as well as six-month CPI inflation probably peaked in June, with the peak occurring within the expected time band following a major top in annual broad money growth in February 2021 – money trends lead inflation by two to three years, according to the monetarist rule of thumb.

G7 annual broad money growth is estimated to have fallen further to below 4% in August, widening an undershoot of its 4.5% average in the five years before the pandemic – chart 2. The suggestion is that G7 inflation rates will be back at or below target around end-2024, if not before.

Chart 2

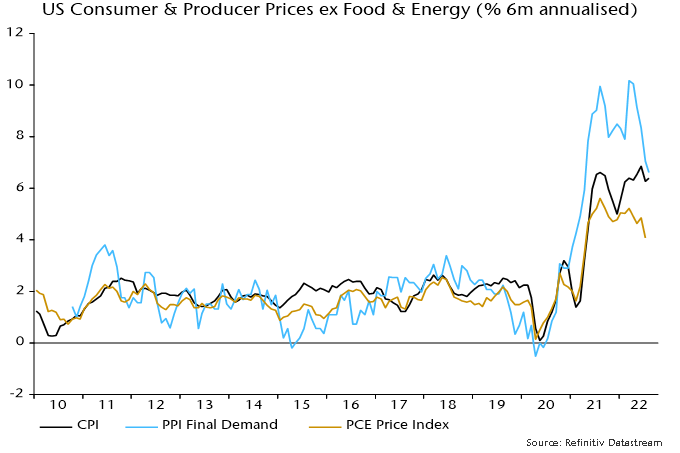

Markets were spooked by last week’s news of a hefty monthly rise in US core CPI in August but six-month momentum was little changed and below a June peak, while PPI pressures continue to ease – chart 3.

Chart 3

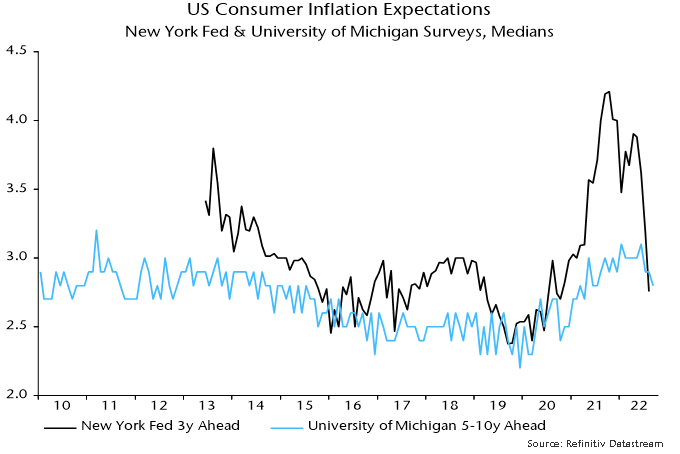

Central bankers are supposedly focused on preventing high inflation from becoming embedded in expectations. The view here has been that expectations were unlikely to become “unanchored” against a backdrop of weak money growth. The latest consumer surveys by the New York Fed and University of Michigan show longer-term inflation expectations back within 2010s ranges – chart 4.

Chart 4

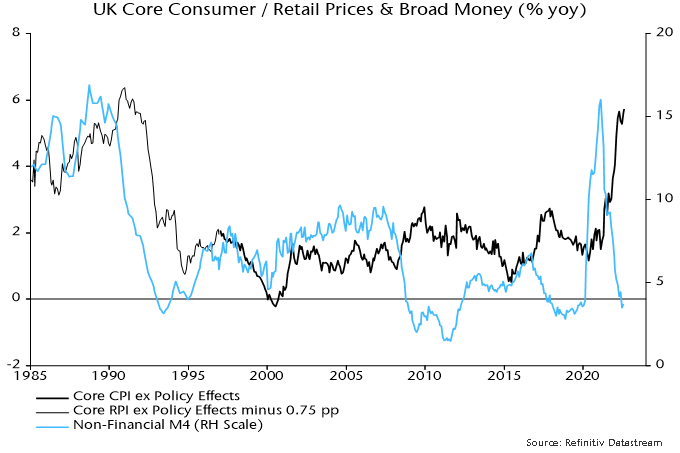

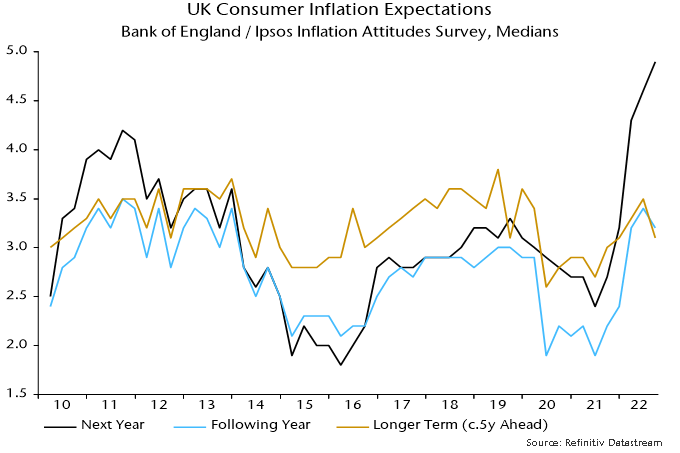

UK annual core CPI inflation made a marginal new high in August but money trends mirror the global picture and are signalling a 2023-24 collapse – chart 5. The latest Bank of England / Ipsos inflation attitudes survey, meanwhile, reported a fall in consumer longer-term inflation expectations, which have remained within the 2010s range – chart 6.

Chart 5

Chart 6

The apparent anchoring of longer-term US / UK expectations suggests that wage pressures will dissipate rapidly as current inflation rates fall sharply in 2023.

*The GSCI commodity price index uses US prices for the natural gas component; the series shown by the gold line in the chart incorporates an adjustment for European prices.