Hints of US inflation relief

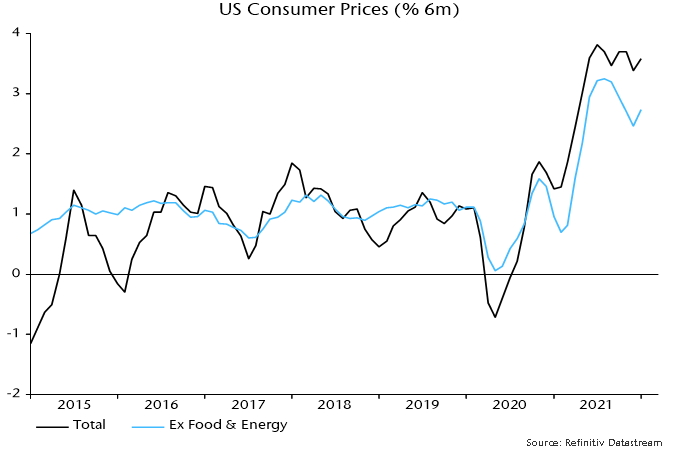

Year-on-year headline and core CPI inflation rates rose further in January, to 7.5% and 6.0% respectively, but six-month momentum remained below peaks reached in July-August – see chart 1.

Chart 1

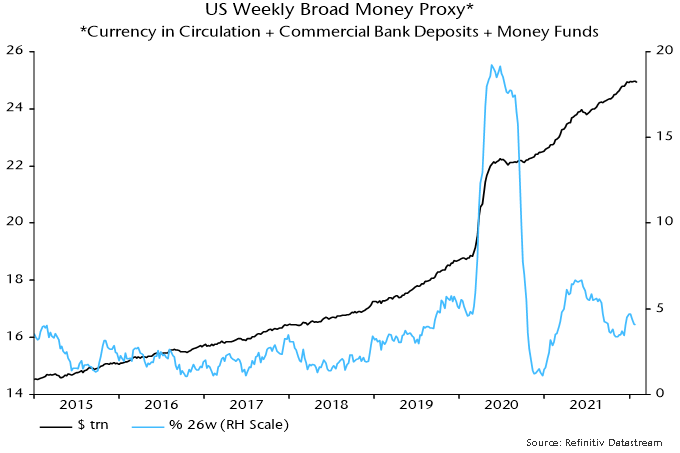

The fundamental cause of current high inflation is excessive monetary expansion in 2020-21 but six-month growth of broad money has returned to its pre-pandemic pace – chart 2. Weekly numbers have stagnated since December, when tapering started.

Chart 2

The year-on-year core rate of 6.0% overstates underlying inflation because of base effects and a one-off surge in vehicle prices. Year-on-year was only 1.4% in January 2021 so core prices have risen at an average rate of 3.7% pa over the last two years.

The CPI component for new and used vehicles soared by 28.1% between January 2020 and January 2022, boosting core CPI by 2.5 pp – vehicles had a 9.1% weight in the core basket in January 2020.

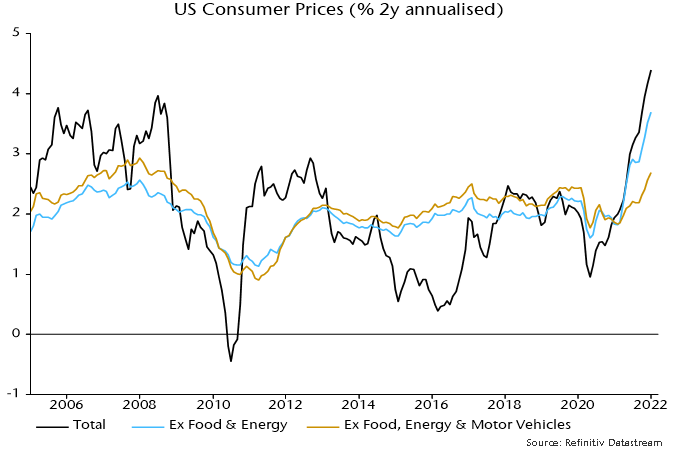

Stripping out vehicles, core CPI rose by “only” 2.7% pa in the two years to January. Two-year inflation on this measure reached a higher peak in the 2000s – chart 3.

Chart 3

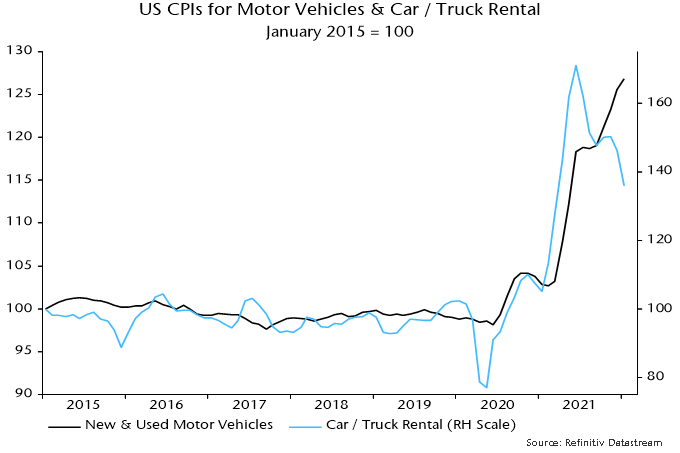

Vehicle prices should correct as supply constraints ease and high fuel prices depress demand. A recent fall in car / truck rental rates may be a harbinger – chart 4.

Chart 4

Suppose that core CPI ex. vehicles rises by 3.5% over the coming 12 months, above its two-year rate of increase of 2.7% pa. If vehicle prices were to correct by 10% over this period, the conventional core rate would fall to 1.9% in January 2023.

Actual and imputed rents are widely expected to exert upward pressure on core inflation. However, year-on-year rental inflation would have to rise from the current 4.4% to 8% to offset a 10% fall in vehicle prices. Rental inflation hasn’t breached 6% since the mid 1980s.

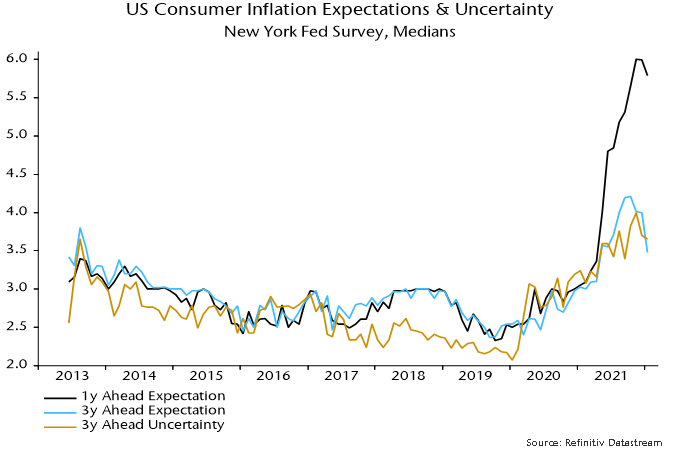

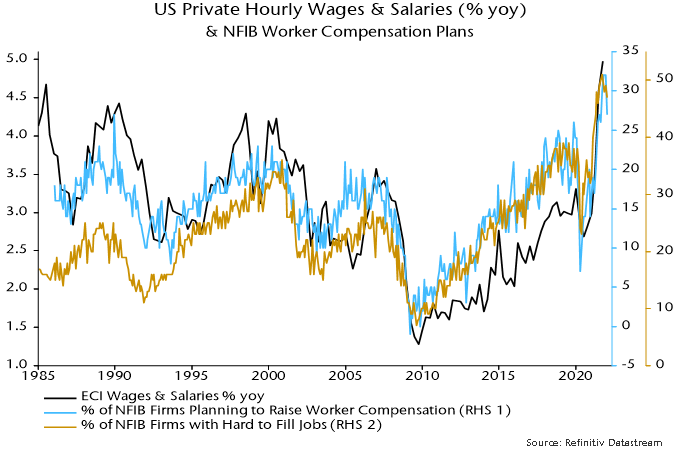

The Fed and other central banks are focused on backward-looking inflation indicators, including wage growth and (adaptive) inflation expectations, rather than money trends. Even these are showing signs of peaking: NFIB small firm worker compensation plans eased in January while New York Fed consumer expected inflation measures fell – charts 5 and 6.

Chart 5

Chart 6