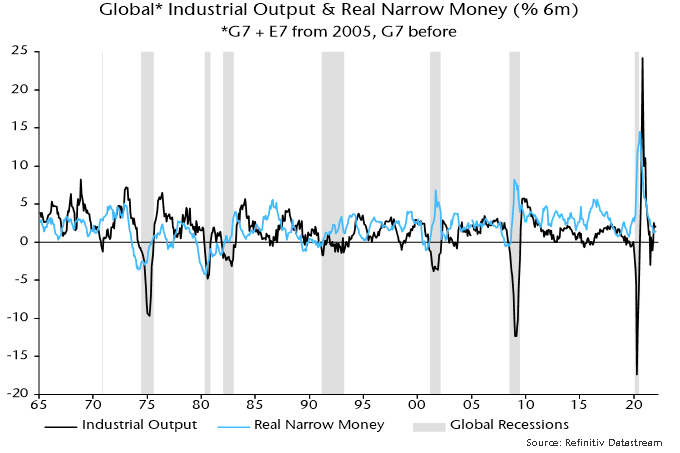

Global real money squeeze approaching recession threshold

Global real money trends were signalling economic weakness before Russia’s invasion of Ukraine. The consequent spike in commodity prices threatens a recession warning signal.

Global six-month real narrow money growth – the key monetary leading indicator followed here – turned negative before the six global recessions preceding the covid shock – see chart 1. The covid recession was not a genuine cyclical contraction because it was caused by a government shutdown of economic activity rather than endogenous spending weakness.

Chart 1

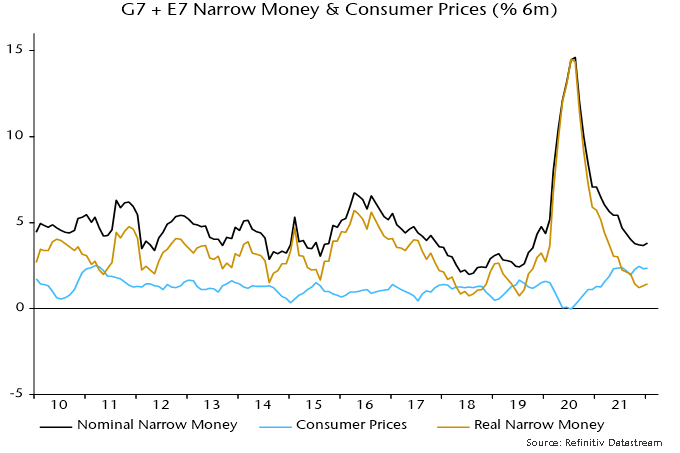

With most data now in, six-month real narrow money growth was an estimated 1.4% (not annualised) in January. This decomposes into nominal money growth of 3.8% and six-month consumer price momentum of 2.3% – chart 2.

Chart 2

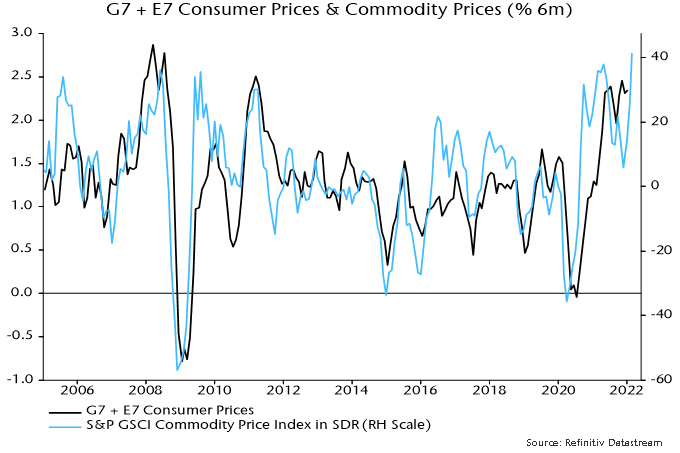

CPI momentum seemed likely to moderate before the invasion, based on a slowdown in the six-month change in commodity prices into December – chart 3. The latest spike suggests renewed upward pressure. A reasonable expectation is that the six-month CPI change will match the 2008 peak of 2.9% if commodity prices remain at current levels.

Chart 3

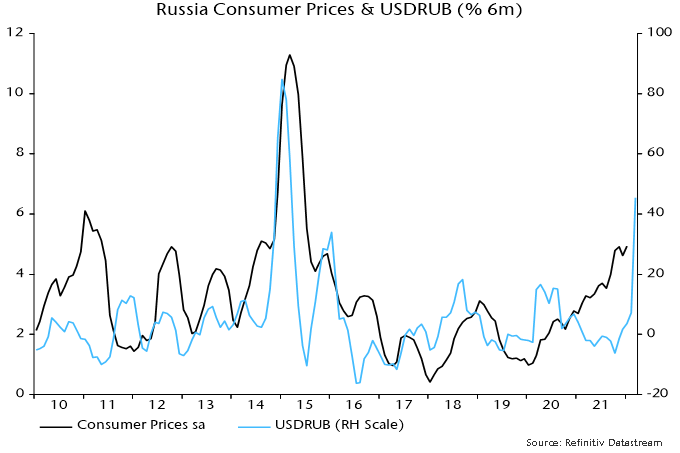

The global inflation measure, however, will receive an additional boost from a surge in Russian consumer prices due to the rouble’s collapse. Russian six-month CPI momentum was 4.9% (again, not annualised) in January but could rise to 15-20% – chart 4. Admittedly, a larger rouble fall in 2014-15 was associated with a lower six-month inflation peak of 11.3% but the depreciation then was driven by oil price weakness, which had an offsetting effect. Russian energy prices could decline as international buyers switch to other suppliers leading to a domestic glut, but any fall is unlikely to be as large as in 2014-15, while sanctions and consequent shortages may put upward pressure on other items.

Chart 4

Russia has a 4% weight in the G7 plus E7 measures calculated here so a 10-15 pp rise in six-month CPI momentum from the current level would push up global CPI momentum by 0.4-0.6 pp.

The combined effect of the commodity price spike and rouble collapse, therefore, could be to boost global six-month CPI momentum by 1 pp or more. A slowdown in six-month nominal money growth of 0.5 pp would then be sufficient for real money growth to turn negative. A slowdown of this magnitude, or greater, is plausible on the basis of QE tapering and rate rises to date, without factoring in widely expected (but unwise) future policy tightening.

A further rise in global six-month CPI momentum – if the above scenario proves correct – may take several months to play out so a recession warning from real money might not be received until well into Q2.