Global money trends still cautionary

Global six-month real narrow money growth appears to have edged lower in March, continuing a downtrend since last summer. This suggests that an expected relapse in global industrial momentum will extend through late Q3 / early Q4.

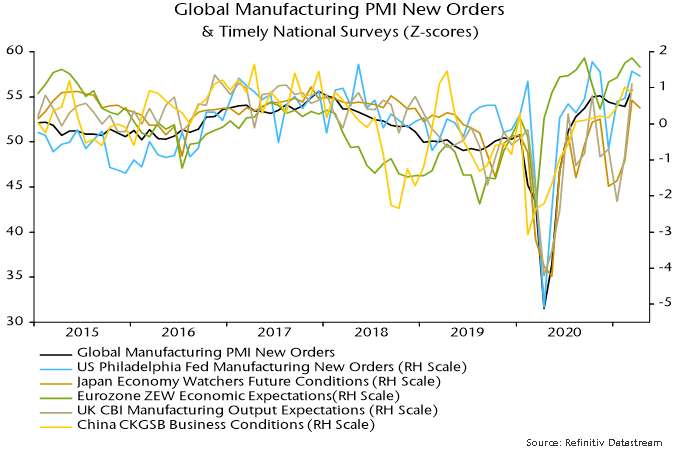

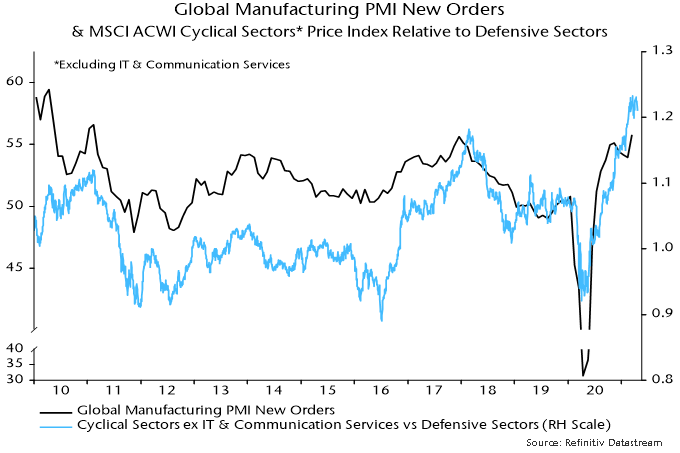

The global manufacturing PMI new orders index reached a new recovery high in March, consistent with a surge in six-month real narrow money growth into July / August 2020, allowing for the historical average 6-7 month lead time. More recent national surveys hint that March will mark a top – see chart 1.

Chart 1

The March real money growth estimate is based on information for the US, China, Japan, India and Brazil, together accounting for 70% of the G7 plus E7 aggregate tracked here. The US component is estimated from weekly data on currency in circulation and commercial bank deposits – official March money numbers are released next week and the Fed no longer provides weekly updates.

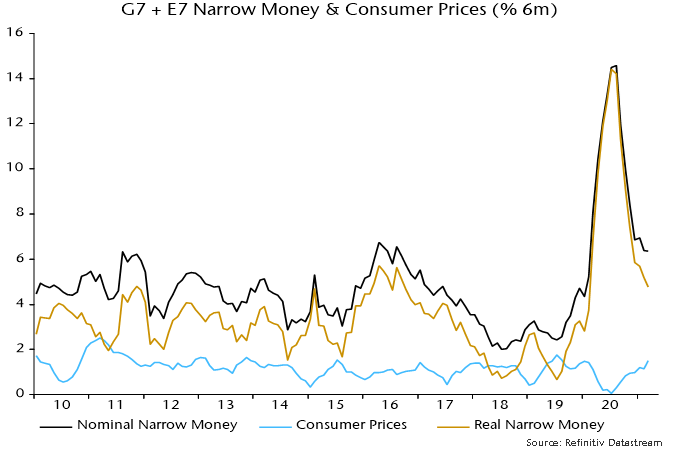

Global six-month real narrow money growth appears to have eased further to its lowest level since February 2020, reflecting stable nominal growth and another rise in six-month CPI inflation – charts 2 and 3.

Chart 2

Chart 3

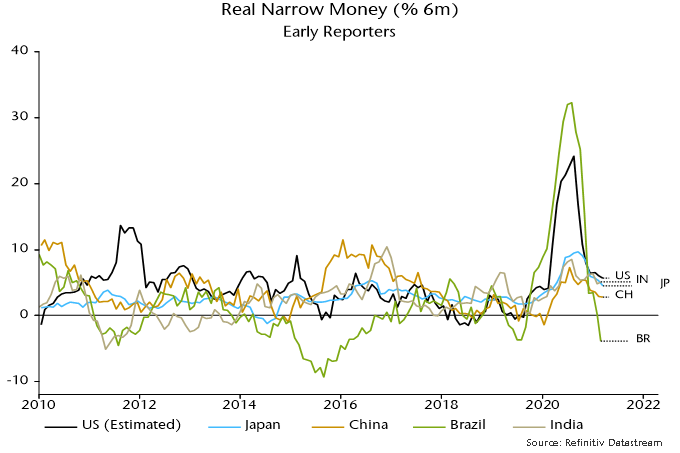

Chart 4 shows the early reporting countries individually. US six-month real narrow money growth is estimated to have edged lower despite disbursement of $318 bn of stimulus payments to households – these were made in the second half of the month and may have a larger impact in April (the money numbers are month averages).

Chart 4

Six-month growth also eased slightly further in Japan and China, with a small rise in India. Brazil moved into contraction although this needs to be placed in the context of an extraordinary surge last summer – 12-month growth is still strong.

Markets could be starting to offer corroboration of the scenario of a global manufacturing PMI new orders peak and pull-back, with Treasury yields stalling and equity market cyclical sectors no longer outperforming – chart 5.

Chart 5

Will global six-month real narrow money growth recover? Six-month CPI inflation is likely to rise slightly further in April / May but could fall back in H2 as commodity prices move sideways or correct.

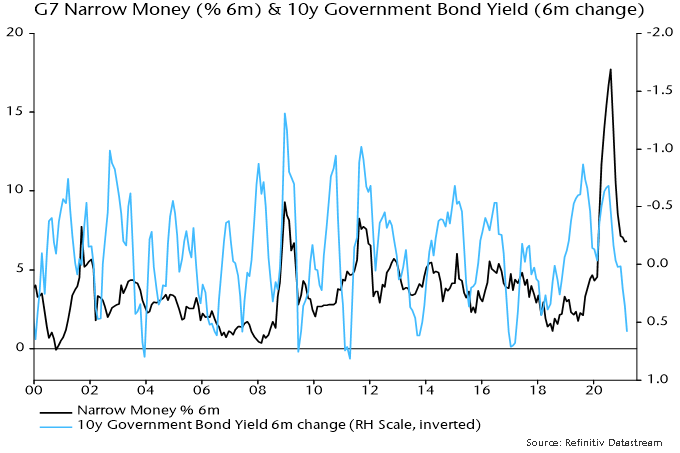

Fiscal stimulus is acting to push up US nominal money growth but there may be an offsetting drag across the G7 from recent bond yield rises – chart 6.

Chart 6

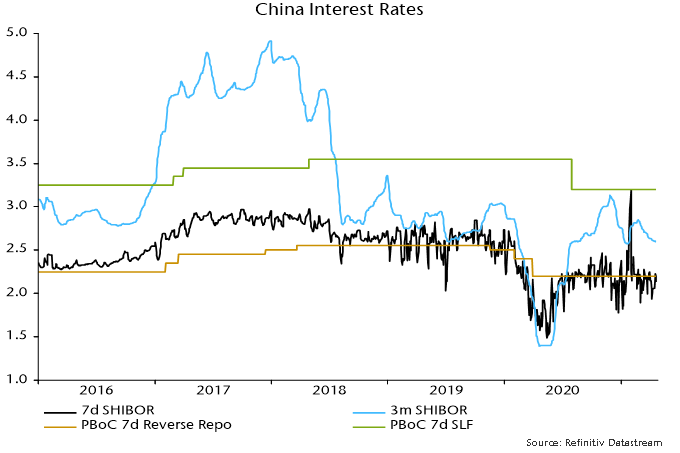

A revival in Chinese narrow money growth probably requires a PBoC policy shift. The view here has been that policy was overtightened in H2 2020 and the economy would slow in H1 2021. This scenario appears to be playing out, with Q1 GDP disappointing and industrial output falling in March. Core CPI inflation (i.e. ex. food and energy) is at 0.3% and a surge in PPI inflation reflects input cost rises that are squeezing downstream margins. The PBoC has allowed three-month SHIBOR to drift back to its January low, consistent with a switch to an easing bias – chart 7.

Chart 7