Global money trends inconsistent with recovery hopes

The global manufacturing PMI new orders index was little changed in November, the six-month rate of change of the OECD’s G7 leading indicator has hooked up and cyclical sectors have been outperforming defensive sectors in the recent equity market rally. Do these developments signal a bottoming of global economic momentum and a prospective H1 2023 recovery?

Monetary trends argue not. Global (i.e. G7 plus E7) six-month narrow money momentum rose slightly for a fourth month in October but remains in negative (i.e. recessionary) territory. All previous recoveries through the 50 level in global manufacturing PMI new orders were preceded by real money momentum rising above 2% – see chart 1.

Chart 1

The June low in real narrow money momentum will probably hold but a corresponding PMI new orders low is unlikely before Q1 2023. There was a 10-month lag between the most recent real money growth peak (July 2020) and the matching PMI top (May 2021).

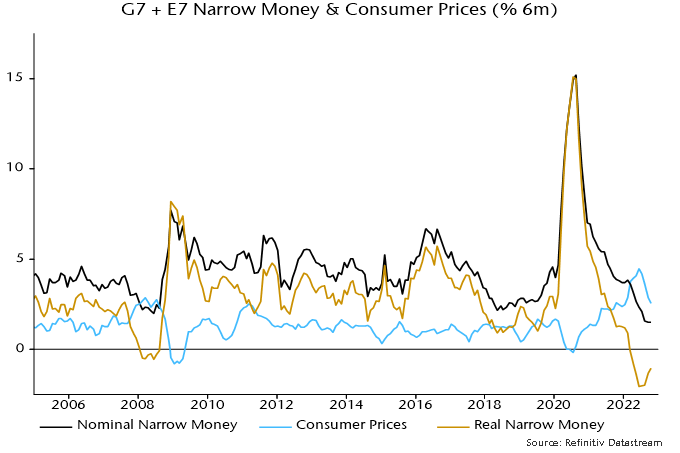

There are additional negative considerations. The rise in real money momentum since June has been due to an inflation slowdown, with nominal money growth weakening further – chart 2. Previous PMI recoveries were preceded by nominal as well as real money accelerations.

Chart 2

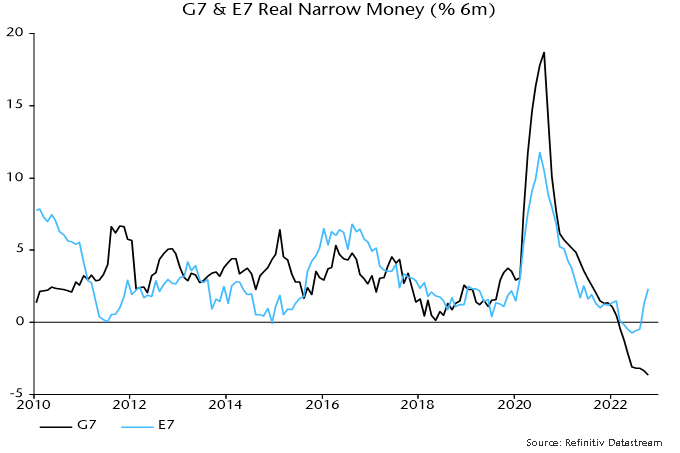

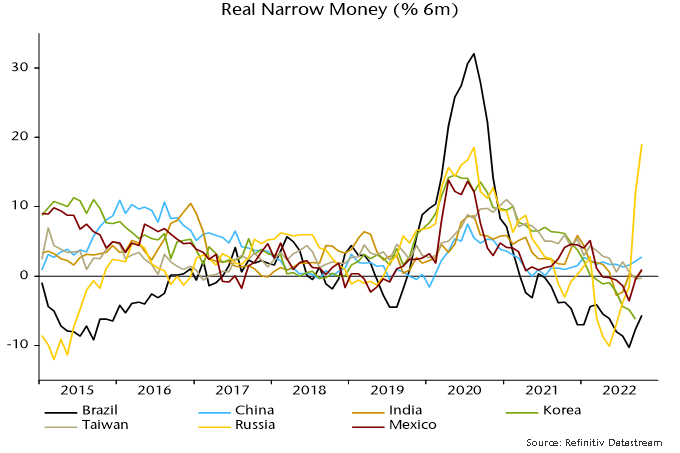

The rise in global real money momentum reflects the E7 component, with G7 momentum still weakening – chart 3. China, India, Mexico and Brazil have contributed to the E7 recovery but the increase has been exaggerated by a nominal money surge and inflation drop in Russia – chart 4. The latter may be of limited global relevance given Russia’s partial economic isolation.

Chart 3

Chart 4

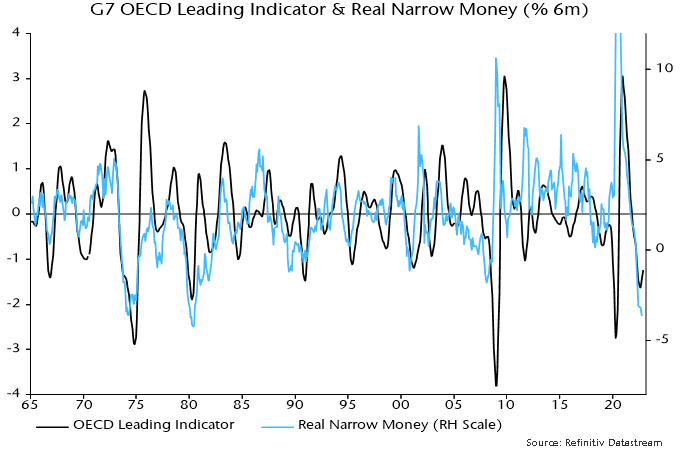

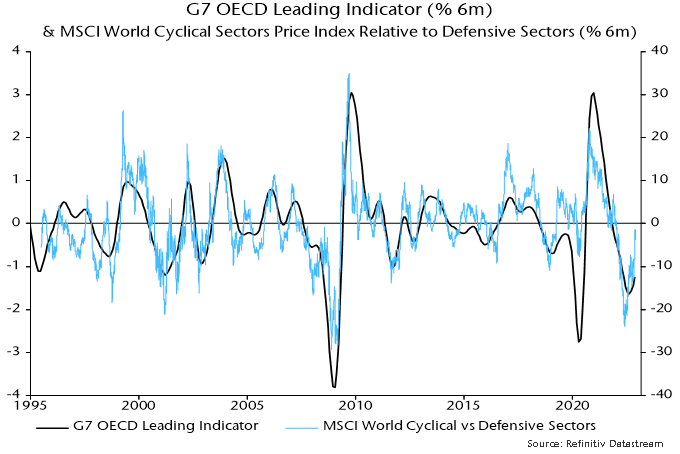

The six-month rate of change of the OECD’s G7 leading indicator rose slightly for a third month in November, according to calculations here. This appears to be a hopeful signal – bottomings historically have usually been followed by sustained recoveries, as chart 5 shows. The uptick is also consistent with recent better relative performance of cyclical equity market sectors.

Chart 5

Initial indicator readings, however, are often revised significantly and previous sustained recoveries in the six-month rate of change from negative territory were accompanied or more usually preceded by a revival in G7 real narrow money momentum – chart 6. With the latter yet to bottom, the uptick in indicator momentum may be either revised away or reversed.

Chart 6