Global monetary round-up

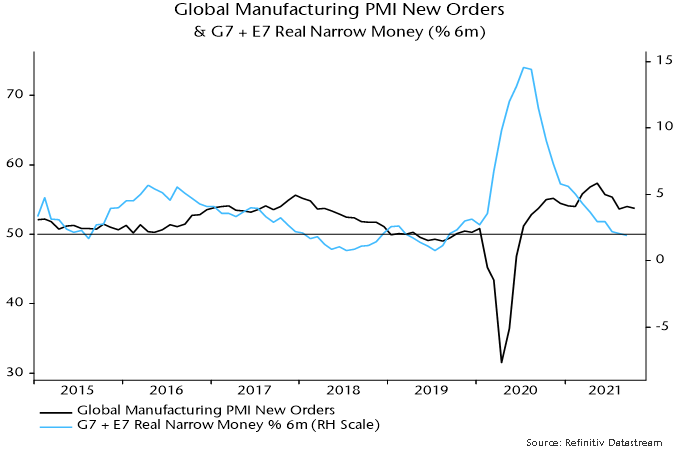

Additional monetary data confirm an earlier estimate here that global (i.e. G7 plus E7) six-month real narrow money growth fell slightly further in September, reaching its lowest level since August 2019 – chart 1. Allowing for the usual lead, the suggestion is that global industrial demand momentum – proxied by the manufacturing PMI new orders index – will weaken into end-Q1 2022 and possibly beyond.

Chart 1

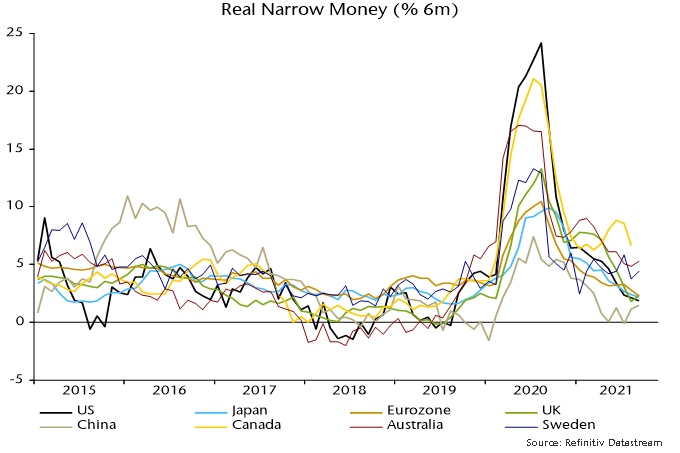

Real narrow money is growing at a similar pace in the US, Japan, Eurozone and UK, i.e. there is no longer a monetary case for expecting superior US economic and asset price performance – chart 2.

Chart 2

Real narrow money growth remains relatively strong in Canada (one month behind), Australia and Sweden. Economic and / or inflation data have been surprising positively in all three cases, triggering policy shifts by the BoC and RBA – will the currently dovish Riksbank be next to capitulate?

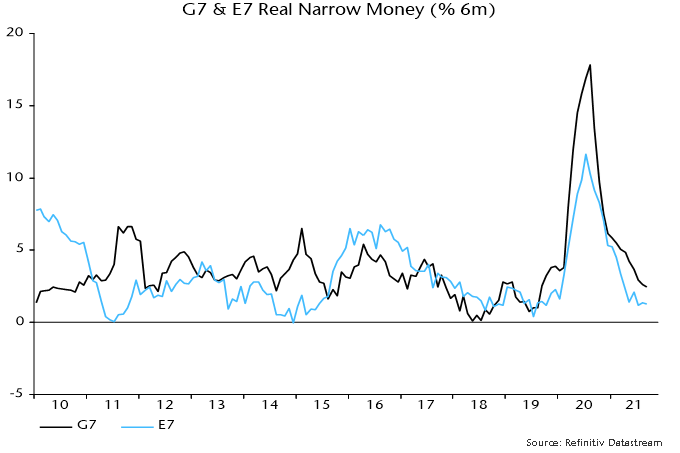

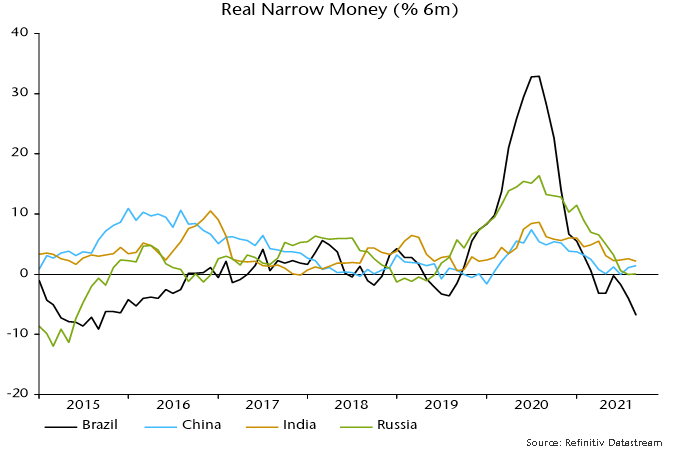

Real money growth remains lower in the E7 than the G7, partly reflecting drags from Russia and Brazil, where monetary policies may have been tightened excessively – charts 3 and 4.

Chart 3

Chart 4

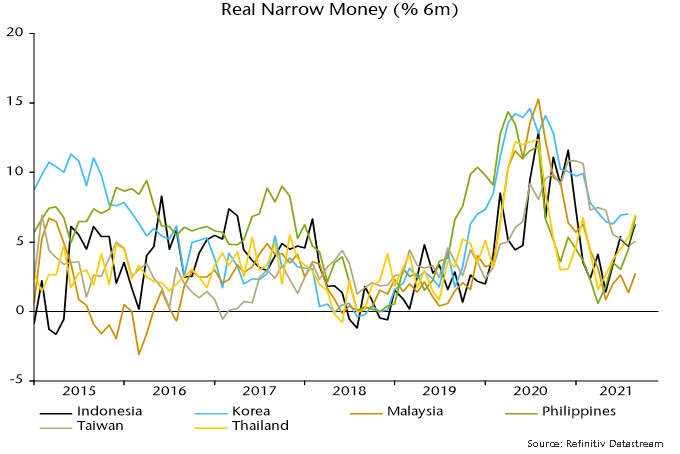

Money trends are perkier in EM Far East economies. Real narrow money growth remains relatively strong in Korea / Taiwan and has ticked up recently, while there have been notable rebounds in Indonesia, the Philippines and Thailand, partly reflecting reopenings – chart 5.

Chart 5

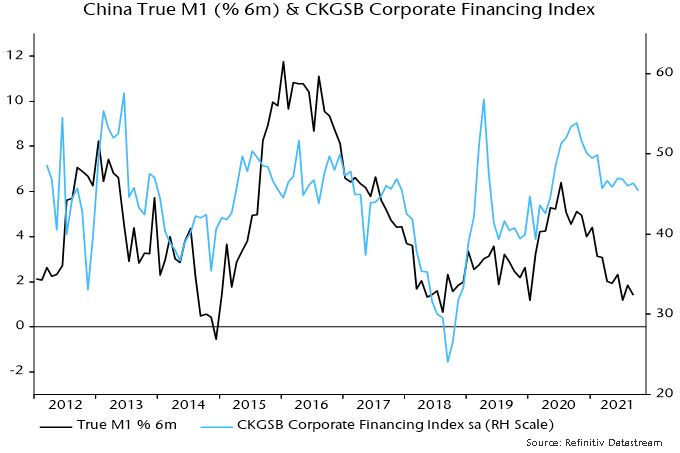

Will China be next? The worry has been that Evergrande fallout would lead to a tightening of credit conditions, aborting an incipient recovery in money growth due to modest policy easing since Q2. The October Cheung Kong business survey was hopeful in this regard: the corporate financing index (a gauge of ease of access to external funds) fell slightly but remains at a normal level – chart 6.

Chart 6

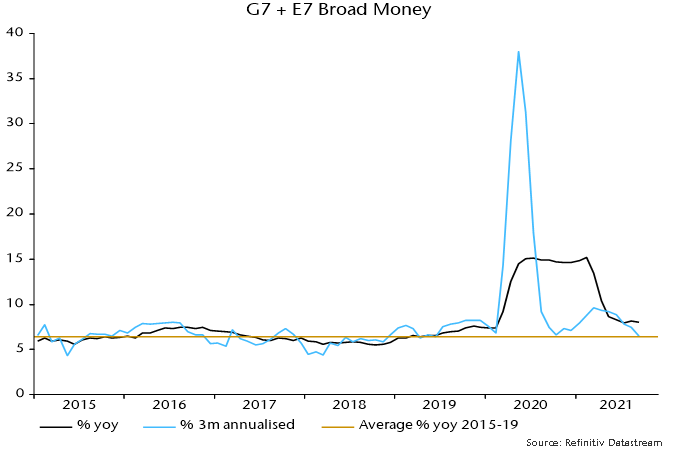

Monetarists have a straightforward response to the ongoing debate about whether global inflation is shifting to a permanently higher level: it won’t if global broad money growth reverts to its pre-covid norm.

While annual growth remains elevated, G7 plus E7 nominal broad money expanded at a 6.5% annualised rate in the three months to September, in line with the 2015-19 average – chart 7. Central banks won’t need to raise interest rates by much to contain inflation if this pace is sustained.

Chart 7

Money growth has slowed despite ongoing QE, suggesting a risk of an undershoot as these programmes wind down. The more likely scenario, however, is that a pick-up in bank lending provides offsetting support.

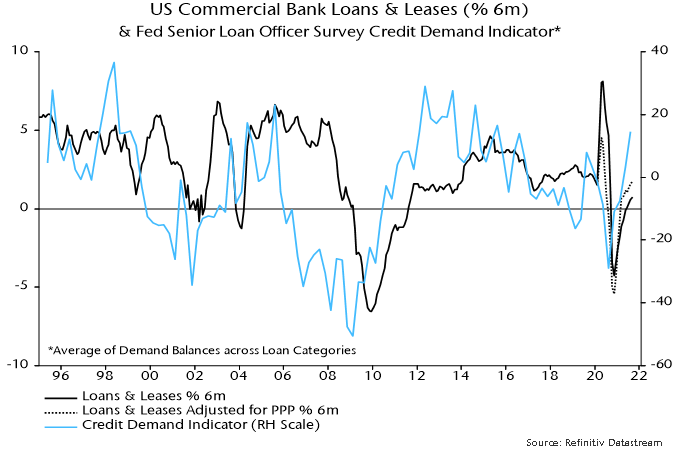

US commercial bank loan growth continues to firm, with the recovery underappreciated because of the distorting effect on headline data of PPP loan forgiveness – chart 8. The July Fed senior loan officer survey had signalled stronger credit demand; an October survey is due shortly.

Chart 8

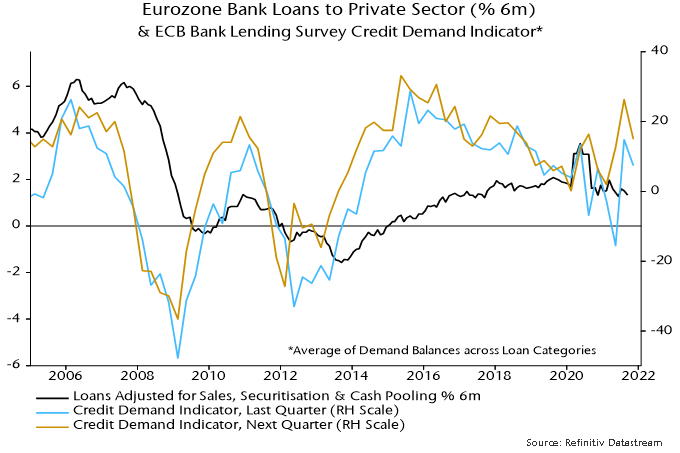

The corresponding ECB survey has already been released and showed a pull-back in credit demand indicators, although they remain in hopeful territory – chart 9. Actual loan growth, however, has remained modest / stable.

Chart 9