Global earnings momentum fading before Evergrande

The global industrial slowdown signalled by a fall in manufacturing PMI new orders over June-August is now being reflected in a loss of earnings momentum.

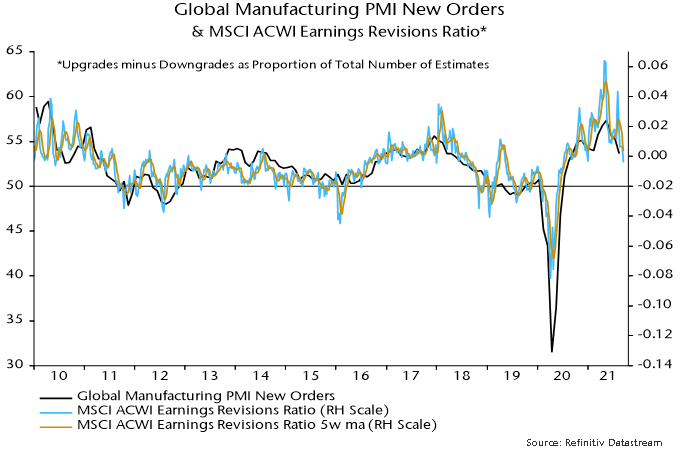

The MSCI All Country World Index (ACWI) weekly revisions ratio, seasonally adjusted, fell below zero last week to its lowest level for more than a year – see chart 1.

Chart 1

With global real narrow money trends suggesting a further decline in manufacturing PMI new orders through early 2022, the revisions ratio is likely to remain in negative territory for the foreseeable future.

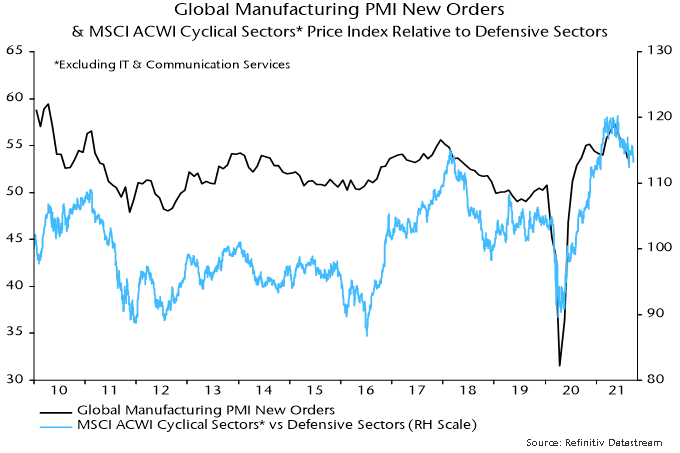

A falling PMI / weakening earnings momentum is typically associated with underperformance of non-tech cyclical equity market sectors (i.e. materials, industrials, consumer discretionary, financials and real estate) versus defensive sectors (consumer staples, health care, utilities and energy). The MSCI ACWI non-tech cyclical / defensive sector price relative has moved down in recent days, though remains above an August low – chart 2.

Chart 2

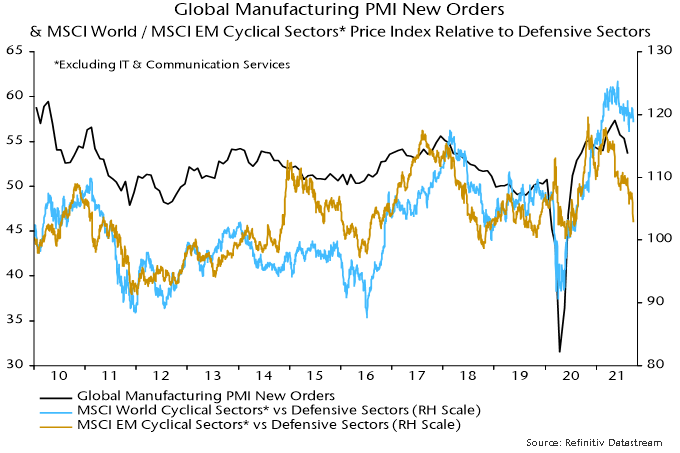

The latest decline, of course, reflects macro risk aversion due to the Evergrande crisis. The MSCI Emerging Markets non-tech cyclical / defensive sector price relative has crashed to a new low, with more modest weakness in the corresponding MSCI World (i.e. developed markets) relative – chart 3.

Chart 3

As the chart shows, the EM relative led moves down into lows in 2011-12, 2016 and 2018 (all associated with stockbuilding cycle downswings). The current wide divergence raises the possibility of a breakdown of the MSCI World relative; alternatively, the EM relative may have greater recovery potential.

Street research is discussing whether a looming Evergrande default represents a Minsky / Lehman moment (i.e. a tipping point into a financial crisis) or a Volcker moment (i.e. a policy decision to punish inflationary / speculative excess despite harsh macroeconomic consequences). The consensus is neither and that the authorities will be able and willing to contain the fallout.

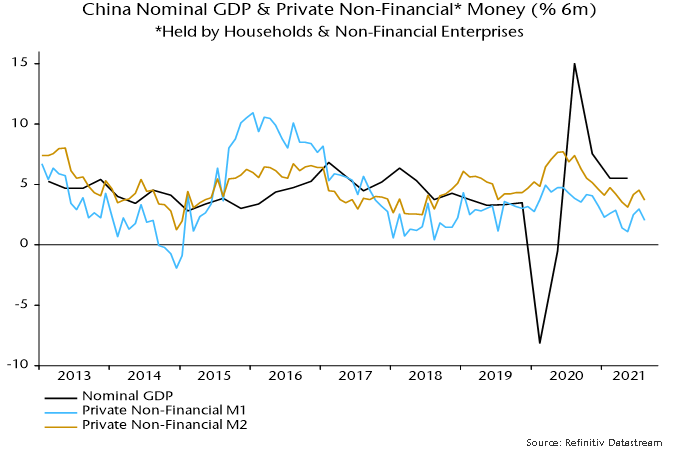

The key issue, from a monetarist perspective, is whether tighter financial conditions due to the crisis persist and invalidate the previous central case scenario of a recovery in monetary trends in response to recent and prospective policy easing. Six-month growth rates of the private sector money measures calculated here fell back in August but remain above May lows – chart 4.

Chart 4

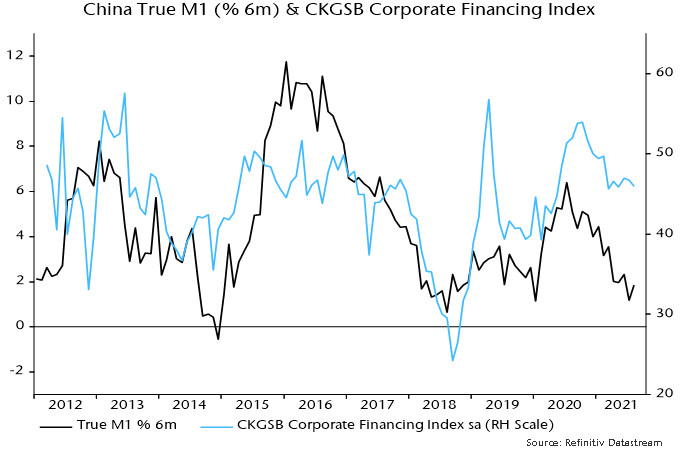

A useful indicator for assessing the potential monetary fallout is the corporate financing index from the Cheung Kong Graduate School of Business survey of private sector firms, a gauge of ease of access to credit. The index loosely correlates with money growth and has moved sideways (after seasonal adjustment) in recent months – chart 5. A sharp fall in the upcoming September survey would be a clear warning signal.

Chart 5