Eurozone slowdown on track, is real money growth bottoming?

Eurozone monetary trends have been suggesting an economic slowdown through end-2021. A recent moderation of consumer price momentum, however, has stabilised six-month real narrow money growth, hinting at a bottoming out of business surveys and other coincident indicators in early 2022.

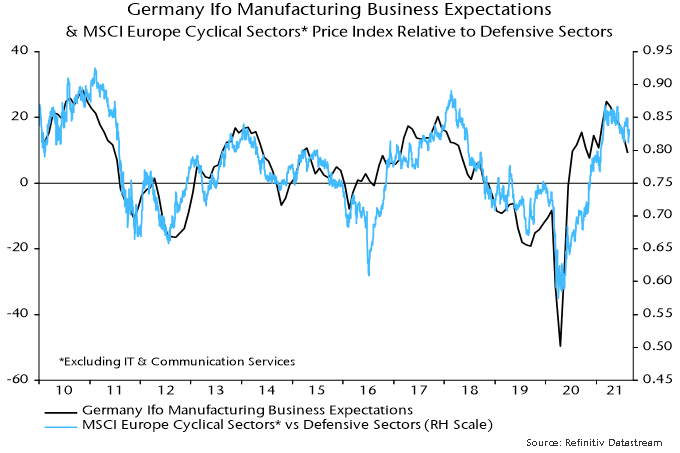

The Ifo manufacturing survey is a timely indicator of German / Eurozone industrial momentum, displaying a strong contemporaneous correlation with German / Eurozone manufacturing PMIs (but with a longer history). The business expectations component peaked in March, falling for a fifth month in August – see chart 1.

Chart 1

The March peak is consistent with an August 2020 peak in Eurozone six-month real narrow money growth. The implied seven-month lead is slightly shorter than the historical average – the correlation between Ifo business expectations and Eurozone real money growth is maximised by applying a nine month lag to the latter.

Real narrow money growth, however, has moved sideways since May (July money numbers were released yesterday). The suggestion is that the Ifo indicator – along with PMIs and other business surveys – will weaken further during H2 but bottom out in early 2022.

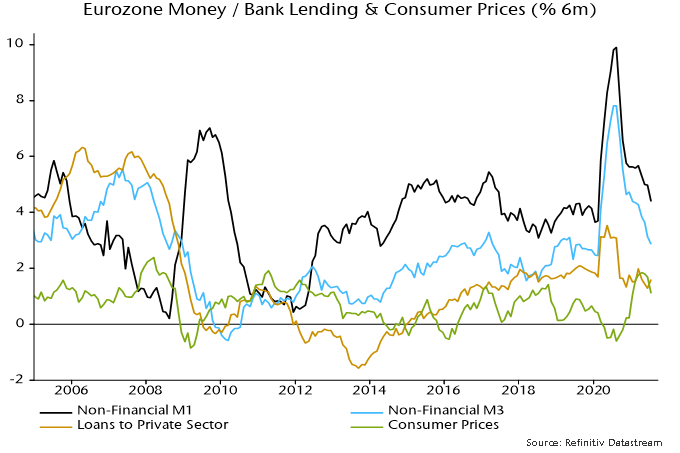

The recent stabilisation of real money growth is not entirely convincing: nominal money trends continued to weaken in June / July but this was offset by a slowdown in six-month consumer price momentum – chart 2.

Chart 2

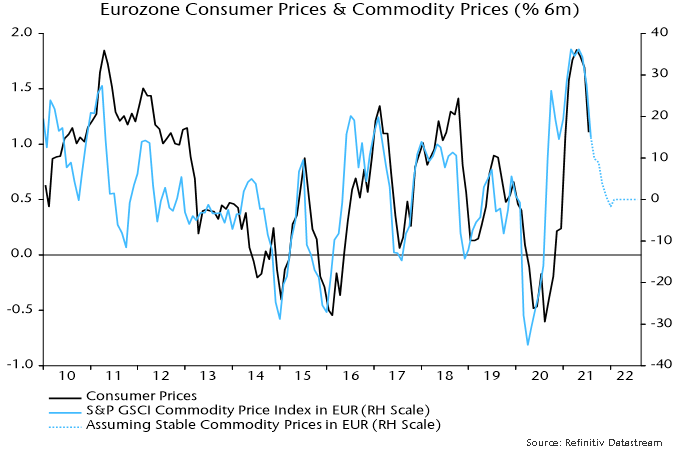

The inflation slowdown, however, could extend, assuming that commodity prices (in euro terms) stabilise at their current level – chart 3.

Chart 3

A recovery in nominal money growth is required to warrant shifting to a positive view of economic prospects. Such a signal would relate to H1 2022 – earlier real money weakness has “baked in” likely economic disappointment over the remainder of 2021.

What could lift money growth? The most likely candidate is a pick-up in bank lending. Six-month growth of loans to the private sector recovered in July – chart 2 – while the most recent ECB bank lending survey reported the strongest expectations for credit demand since 2016.

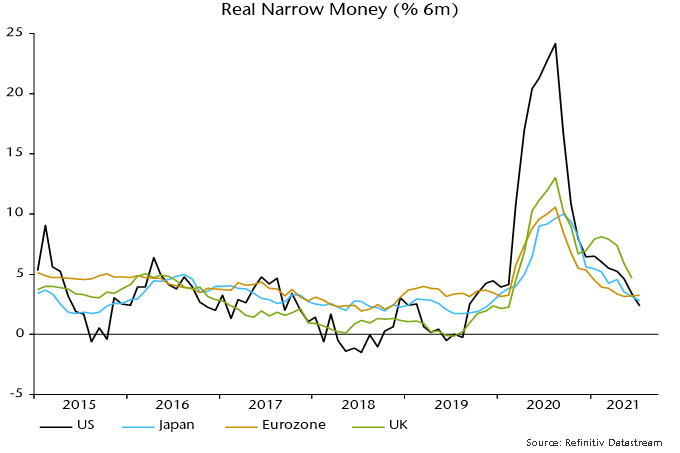

The recent stabilisation of Eurozone six-month real narrow money growth contrasts with a further slowdown in the US – chart 4. The divergence / cross-over suggests improving Eurozone relative economic and equity market prospects, although US real growth could benefit from a faster inflation slowdown over coming months.

Chart 4

A further fall in Ifo manufacturing business expectations and other survey indicators during H2 would probably be associated with underperformance of European non-tech cyclical sectors relative to defensive sectors – chart 5.

Chart 5