Eurozone money update: from bad to worse

There are three messages from Eurozone monetary data for May released yesterday.

- The region faces a major recession that is likely to extend into early 2023, at least.

- Economic prospects are at least as bad for core countries as for the periphery.

- Nominal monetary trends are consistent with inflation returning to – or falling below – the 2% target in 2023-24, arguing for an immediate suspension of ECB tightening plans.

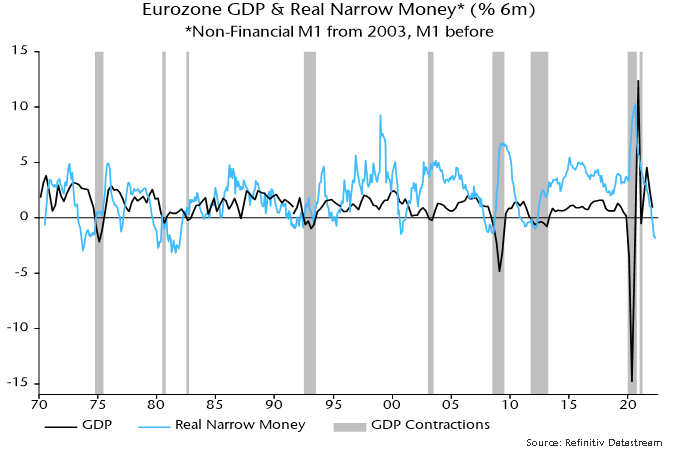

The “best” monetary leading indicator of Eurozone GDP, according to ECB research, is real non-financial M1, i.e. holdings of currency and overnight deposits by households and non-financial corporations deflated by consumer prices.

The six-month rate of change of real non-financial M1 turned negative in January and fell further to -1.9% (not annualised) in May, below the lows reached before / during the 2008-09 and 2011-12 recessions – see chart 1.

Chart 1

Based on longer-run data for real M1, the current rate of real narrow money contraction is the fastest since 1981.

All previous recessions ended only after the six-month rate of change turned positive. The ECB research, meanwhile, found that real narrow money led GDP by three to four quarters on average. The suggestion is that an incipient recession will extend into Q1 2023, at least.

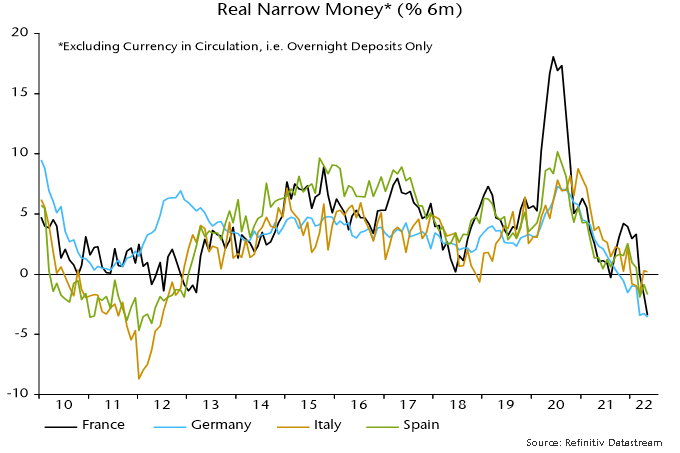

Chart 2 shows six-month rate of changes of real non-financial M1 deposits in the big four economies. (A country breakdown of currency holdings is unavailable.) In a reversal of the pattern before the 2011-12 recession, weakness is more pronounced in Germany and now France than in Spain and Italy. German divergence partly reflects higher inflation but nominal growth of deposits is also weaker in France / Germany than Spain / Italy.

Chart 2

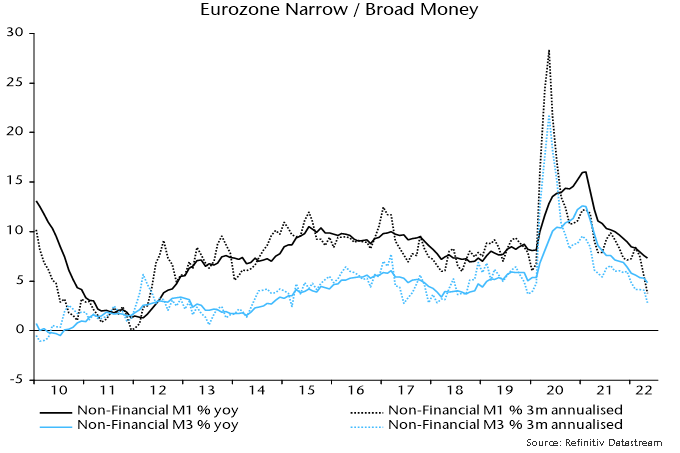

Eurozone nominal money trends, meanwhile, indicate rapidly improving medium-term inflation prospects. Annual growth of broad money, as measured by non-financial M3, slowed to 4.8% in May, with three-month momentum down to 2.8% annualised, the lowest since 2018 – chart 3.

Chart 3

The slowdown has occurred despite a rise in annual growth in bank loan to a post-GFC high of 5.3% in May. This pick-up does not contradict the negative monetary signal – lending is a coincident or lagging indicator of GDP (confirmed by the ECB research). The coincident / lagging relationship partly reflects a correlation of corporate credit growth with the stockbuilding cycle – demand for short-term loans is strongest as inventories swell at the peak of the cycle. Consistent with this explanation, loans to corporations with a maturity of up to a year grew by an annual 7.0% in May.

The counterparts analysis of M3 shows that the slowdown has been driven by the ending of QE but also a significant balance of payments outflow, reflected in a fall in banks’ net external assets. This outflow is the mirror-image of a basic balance deficit, which has widened as a current account surplus has been wiped out by high energy prices while the Ukraine crisis and other factors have triggered an exodus of capital from the region.