Eurozone money trends suggesting recession risk

Eurozone monetary trends were arguing against ECB policy tightening before the negative shock of Russia’s invasion of Ukraine.

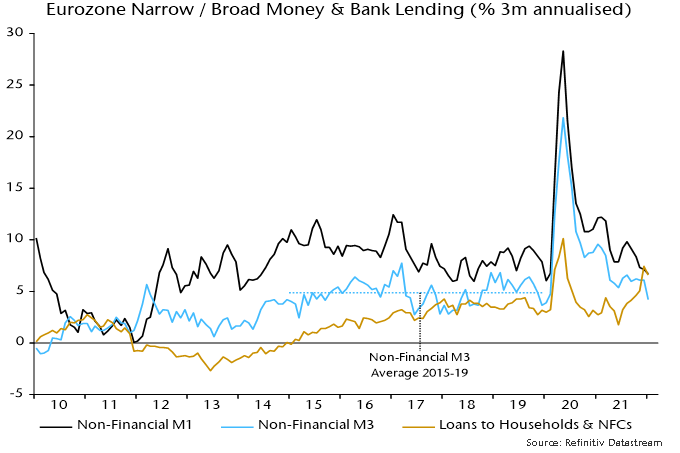

Three-month growth of non-financial M3* – the preferred broad money aggregate here – slowed further to 4.2% annualised in January, the lowest since January 2020 and below a mean of 4.9% over 2015-19, when CPI inflation averaged 1.0% – see chart 1.

Chart 1

Current high inflation reflects excessive money growth in 2020-21 and supply side disruption. It is too late for an ECB response. Any second-round effects will swiftly burn out if money growth maintains its recent subdued pace.

The broad money slowdown has occurred despite ongoing QE, raising the prospect of outright weakness when it stops. The hope is that money growth will be supported by private credit expansion, which has strengthened recently – chart 1. The suspicion here is that corporate loan demand has been boosted by restocking and will fade as this slows.

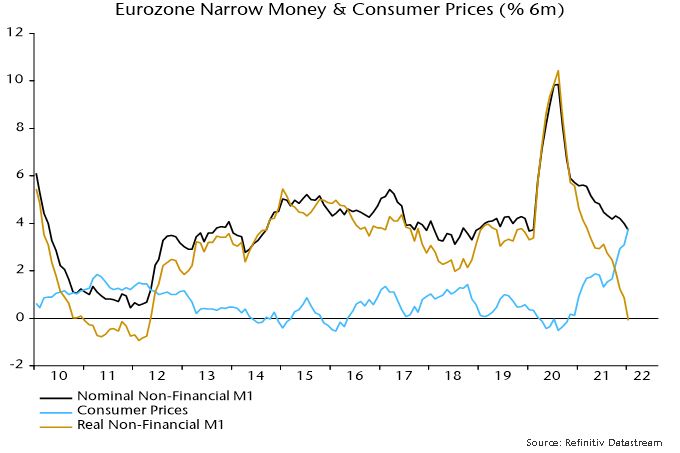

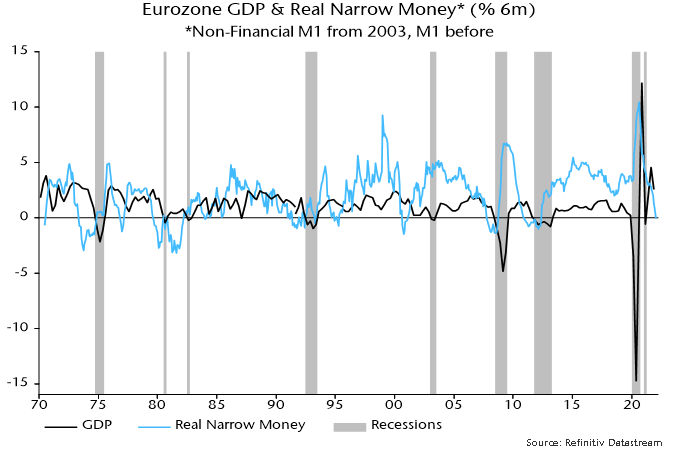

Growth of narrow money (non-financial M1) has also normalised while high inflation has pushed the six-month rate of change in real terms marginally into negative territory – chart 2. Negative readings preceded every recession over 1970-2019, although there were several false signals (e.g. 1994-95) – chart 3.

Chart 2

Chart 3

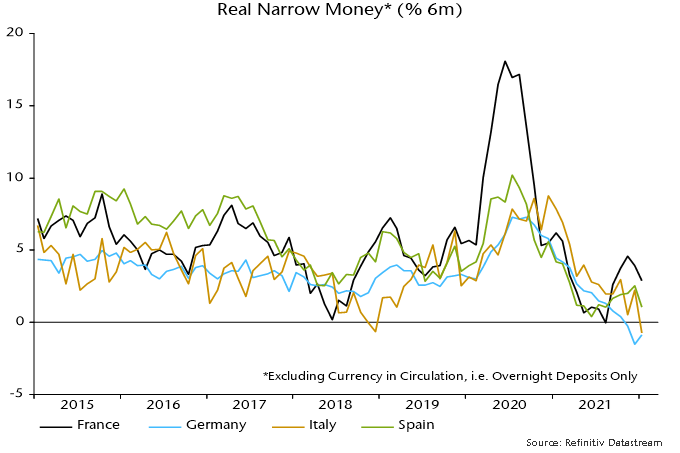

The six-month rate of change of real narrow money deposits is now negative in Italy as well as Germany, with France still showing relative resilience – chart 4.

Chart 4

*M3 holdings of households and non-financial corporations.