Chinese money update: net improvement

The assessment here a month ago was that Chinese monetary policy easing was gaining traction but that additional stimulus and a further recovery in narrow money momentum were required to adopt a positive view of economic prospects.

These conditions have been partially fulfilled: the PBoC has delivered additional easing and six-month narrow money growth picked up in July; however, a food-driven rise in CPI momentum held back real money expansion.

The news, on balance, warrants an upgrade to the assessment: economic momentum is judged likely to recover in late 2022 / H1 2023 barring further negative shocks.

This interpretation, of course, is at odds with deepening consensus gloom. According to the consensus, this week’s “surprise” rate cut was a panic response to worryingly weak July activity and credit data.

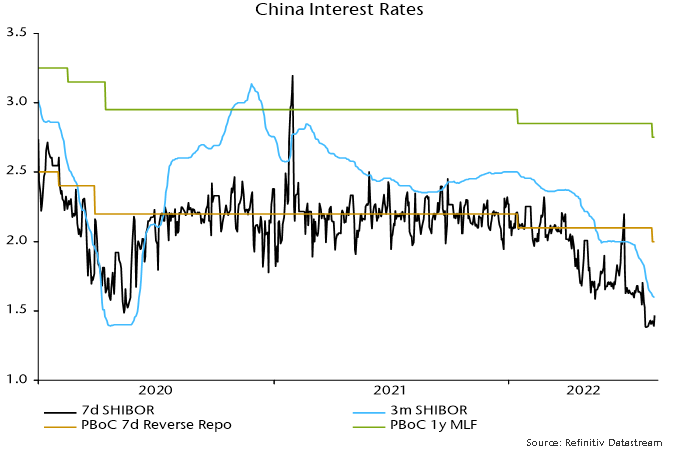

The PBoC, like other central banks, controls short-term money market rates by adjusting the supply of bank reserves relative to demand*. Money rates have fallen steeply since late July, signalling that the PBoC was stepping up easing – see chart 1. Rather than a panic move, the cut in official rates confirms a policy shift that began weeks ago.

Chart 1

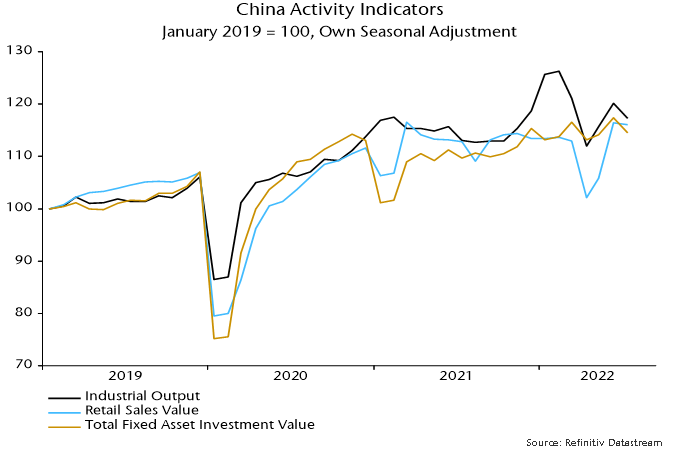

Weaker-than-expected July activity numbers probably reflect payback for May / June gains boosted by catch-up effects following covid disruption. Seasonally-adjusted levels of key series remained comfortably above April lows – chart 2.

Chart 2

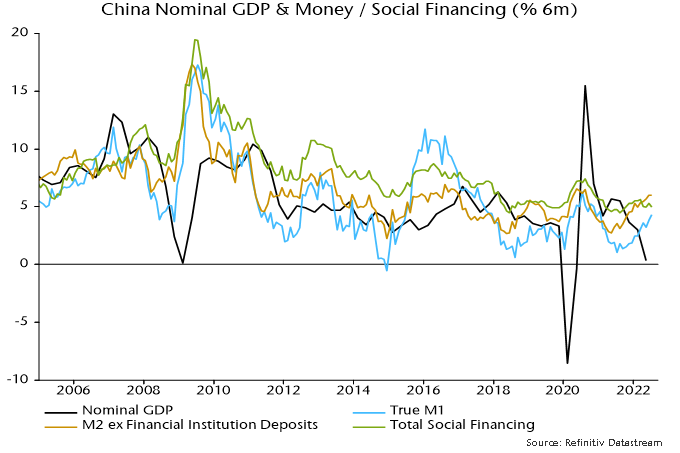

Talk of credit weakness is also exaggerated. The small rise in broad credit (total social financing) in July follows a larger-than-expected increase in June, with six-month growth the same as in April / May – chart 3.

Chart 3

The consensus view ignores better monetary data. Six-month broad money growth in July was stable at the highest level since August 2020. Narrow money growth rose further to its highest since January 2021.

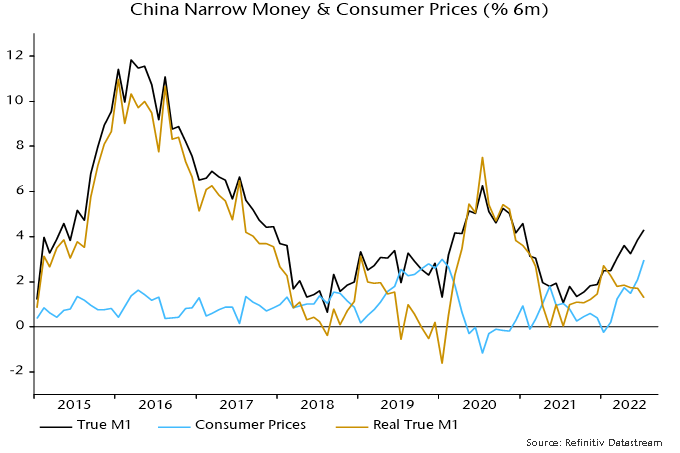

The disappointment in July data, from the perspective here, was a pick-up in six-month CPI momentum, which dragged real money growth lower despite the nominal acceleration – chart 4.

Chart 4

CPI strength was driven by food (pork) prices with annual core inflation still low (0.8%) and PPI inflation falling. Earlier monetary weakness argues for a benign near-term inflation outlook and base effects suggest a decline in six-month CPI momentum in September / October.

*The supply of reserves reflects factors such as flows into / out of government accounts at the central bank and foreign exchange intervention as well as open market operations, changes in reserve requirements etc. Estimates of net supply based only on observable OMOs and other interventions are liable to be misleading whereas movements in money rates reflect the balance of all supply / demand influences.