Chinese money trends still hopeful

Chinese May money numbers give a moderately positive message for economic prospects, suggesting that recent policy easing is gaining traction. Assuming that pandemic disruption is contained, domestic demand is expected here to recover during H2 2022 and into 2023, partially shielding the economy from export weakness due to G7 recessions.

Six-month broad money growth rose further in May and is around levels reached during previous successful monetary / fiscal stimulus campaigns since the GFC – see chart 1.

Chart 1

Narrow money growth, however, continues to lag*, suggesting that improving monetary conditions will take longer than usual to feed through to the economy.

The likely explanation, of course, is that pandemic disruption is holding back demand both directly and via reduced consumer / business confidence, with restraint reflected in a preference to hold additional money in the form of time / savings deposits (for now) rather than ready-to-spend demand deposits.

Still, narrow money growth has recovered significantly since late 2021.

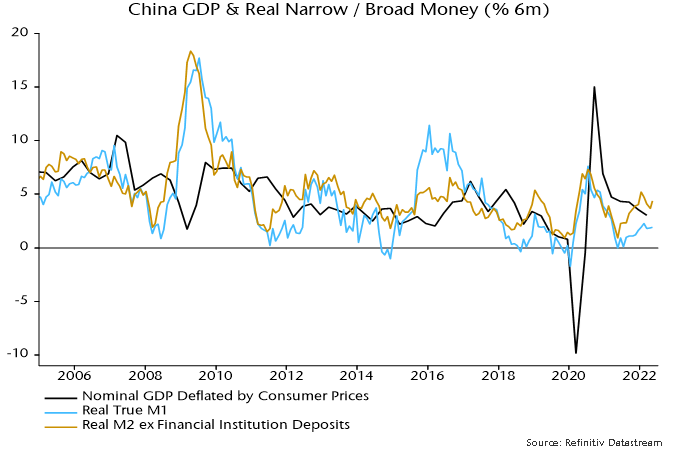

With Chinese CPI inflation contained within its post-GFC range, real as well as nominal money growth rates have improved – chart 2.

Chart 2

As an aside, the relative quiescence of Chinese CPI inflation blows apart US / European central bankers’ claims that current overshoots mainly reflect supply-side shocks. China has suffered the same shocks but pass-through to CPI inflation has been much smaller because of the PBoC’s monetary orthodoxy in 2020-21.

Information through April on the credit counterparts of broad money indicates that the recent growth pick-up has been driven by stronger net lending to government – consistent with expansionary fiscal policy – as well as banks increasing their reliance on monetary funding. Growth of lending to households and firms has moved sideways.

*”Narrow money “= “true” M1 = official M1 + household demand deposits. The May data point is estimated pending release (next week) of a sector breakdown of demand deposits.