Chinese money growth still sliding – PBoC policy shift ahead?

Chinese money trends continue to give a negative message for economic prospects. The PBoC could be moving towards easing policy despite a surge in producer price inflation.

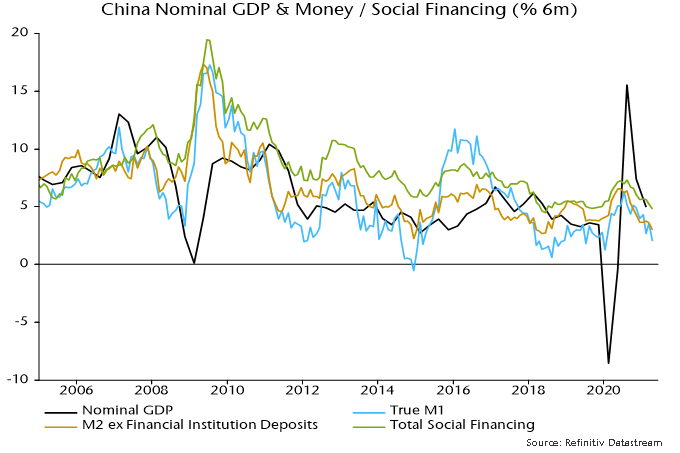

Monthly changes in money and lending aggregates were notably weak in April. Six-month growth rates of narrow money, broad money and broad credit fell again, sustaining a downward trend since Q3 2020 – see chart 1.

Chart 1

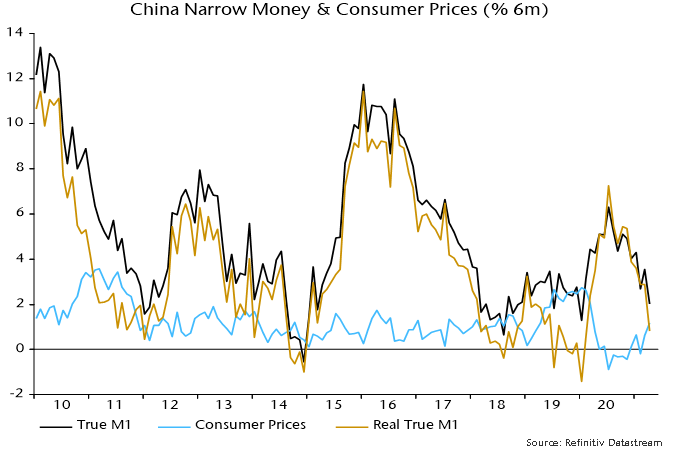

Trends are weaker in real terms because of a recovery in six-month consumer price inflation. Six-month real narrow money growth is the lowest since February last year – chart 2.

Chart 2

The monetary slowdown was the basis for a forecast that the economy would lose momentum in H1 2021. Q1 GDP growth was below consensus and PMIs have moderated since late 2020. Further monetary weakness suggests that that the slowdown will extend through Q3, at least.

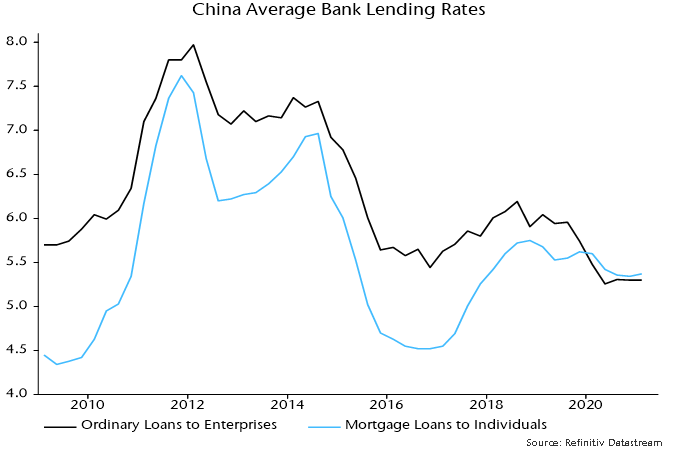

There is little reason to expect money / credit trends to revive. Average interest rates on bank loans have moved sideways since Q3 2020 – chart 3. The PBoC’s Q1 bankers’ survey reported a fall in loan approvals, consistent with a decline in the Cheung Kong Graduate School of Business corporate financing index – weaker readings imply less favourable credit conditions.

Chart 3

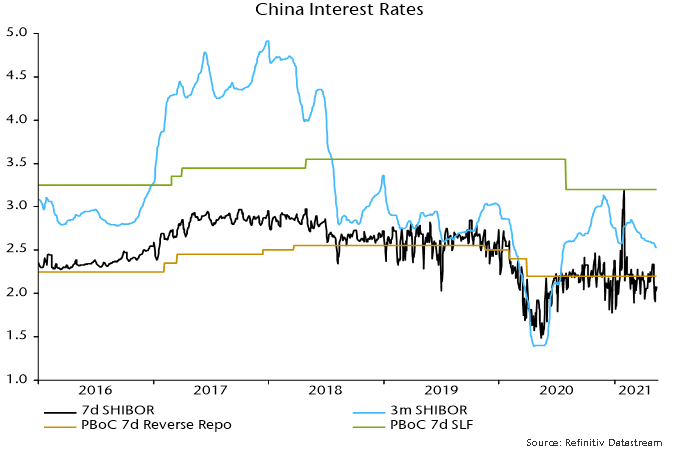

The expectation here was that the PBoC would reverse its H2 2020 policy tightening in response to softer economic data and an ongoing money / credit slowdown. The central bank, however, was concerned about housing market strength in early 2021 and withdrew liquidity to reverse a decline in money market rates into late January.

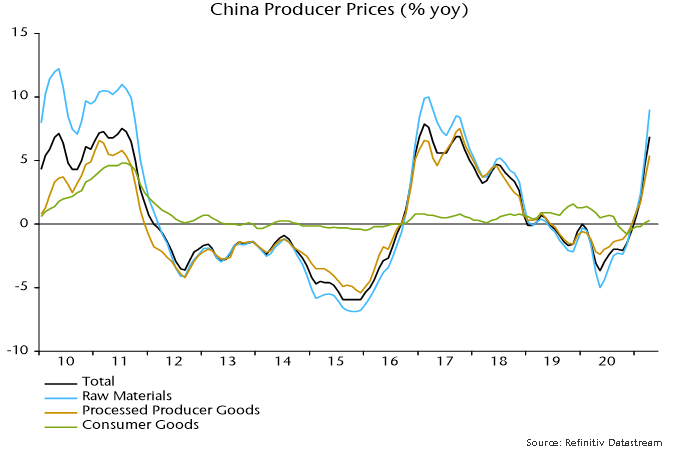

Many continue to expect the next PBoC move to be a tightening, a forecast seemingly supported by a recent surge in producer price inflation. The latter, however, has been driven by raw material costs, with little pass-through to date into producer prices of consumer goods – chart 4.

Chart 4

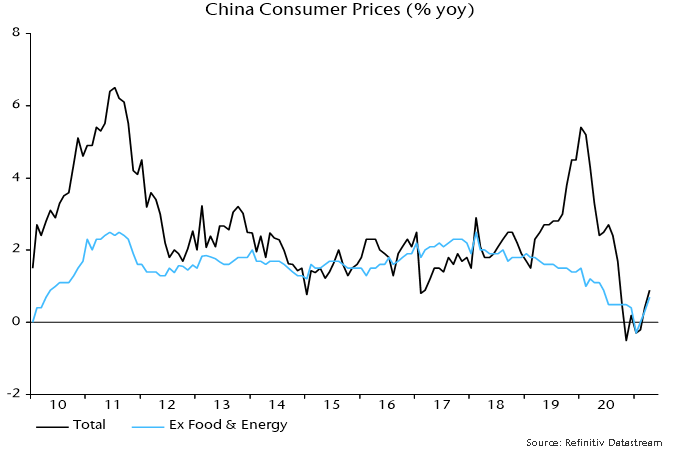

Core consumer price inflation has recovered from early year weakness but remains low – chart 5.

Chart 5

The weak April money / credit numbers could be the trigger for a PBoC rethink. Three-month SHIBOR has been allowed to drift slightly below its January low – chart 6. A further decline would support the view that a policy shift is under way.

Chart 6