China an outlier as global real money weakness intensifies

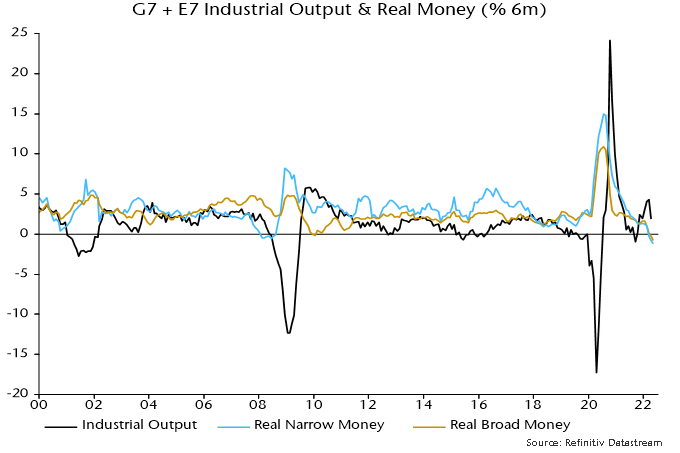

Global six-month real narrow money momentum – a key monetary leading indicator of the economy – is estimated to have moved deeper into negative territory in May, suggesting that a likely recession over the remainder of 2022 will extend into early 2023 – see chart 1.

Chart 1

The May estimate is based on monetary data for countries accounting for a combined 65% weight in the G7 plus E7 aggregate tracked here, along with 93% CPI coverage. Missing numbers are assumed to have maintained stable rates of change.

Real money momentum of an estimated -1.2% (not annualised) compares with lows of 0.4% and -0.5% associated with the 2001 and 2008-09 recessions respectively.

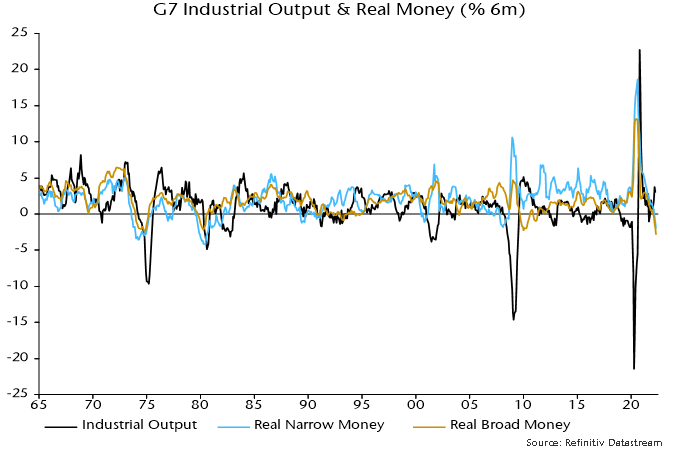

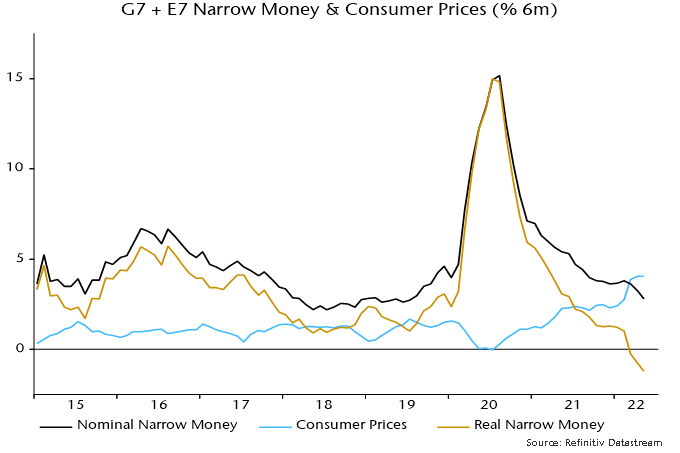

Chart 2 shows a longer-term history using G7-only data. The current rate of contraction of G7 real narrow money was reached only twice over the last 50+ years – in 1973 and 1979 before severe recessions. The rate of contraction of real broad money is faster than during those episodes.

Chart 2

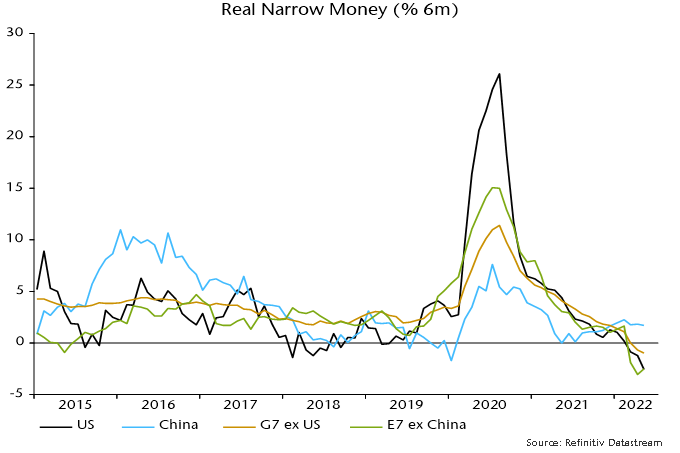

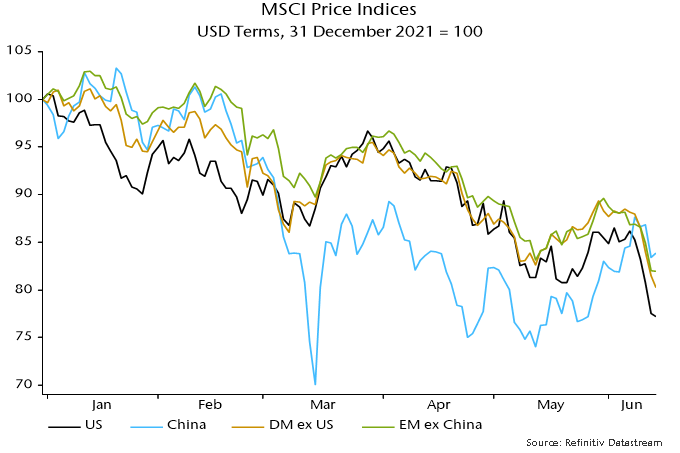

Global real narrow money weakness intensified in May despite stable growth in China, mainly because of faster US contraction – chart 3. China’s positive monetary divergence may explain recent better equity market performance, with the MSCI China index now outperforming global indices year-to-date – chart 4.

Chart 3

Chart 4

The fall in global six-month real money momentum in May was driven by a further slowdown in nominal money growth, with six-month CPI inflation stabilising after a January-April surge – chart 5.

Chart 5

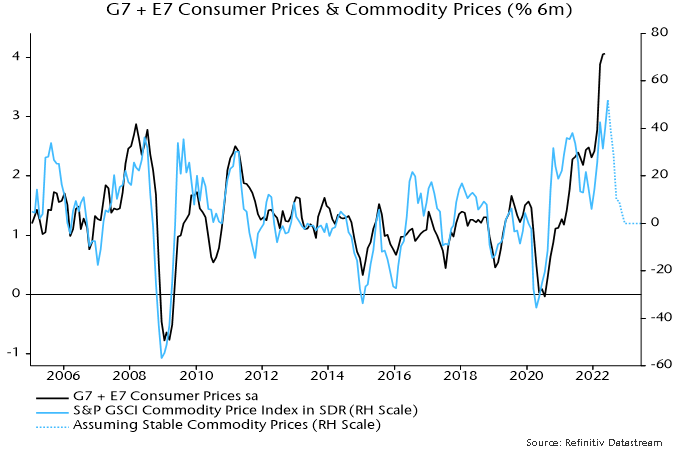

CPI momentum will almost certainly fall back in H2 – the relationship in chart 6 suggests that commodity prices would have to rise by a further 50% by December to prevent a decline.

Chart 6

A CPI slowdown, however, could be offset by further loss of nominal money momentum – unless rising growth in China (22% weight in the G7 plus E7 aggregate) offsets likely weakness in the US / Europe.