BoE policy overkill at least as extreme as Fed / ECB

Recent Bank of England signals have been deemed to be less hawkish than those of the Fed and ECB, contributing to a view that UK policy tightening is less likely to prove excessive, in the sense of causing greater economic damage than necessary to return inflation to target.

Monetary trends do not support this hope.

It should be remembered that the Bank embarked on rate hikes and QT before the Fed and has raised rates by 340bp versus the ECB’s 250 bp.

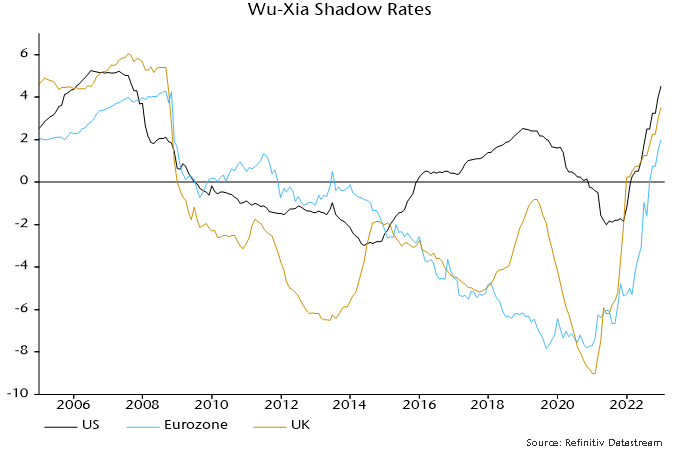

“Shadow” rate estimates attempt to incorporate the impact of unconventional monetary policy measures. The Wu-Xia shadow rate for the UK has risen by 1250 bp from its 2021 low versus increases of 650 bp and 980 bp respectively in the US and Eurozone – see chart 1.

Chart 1

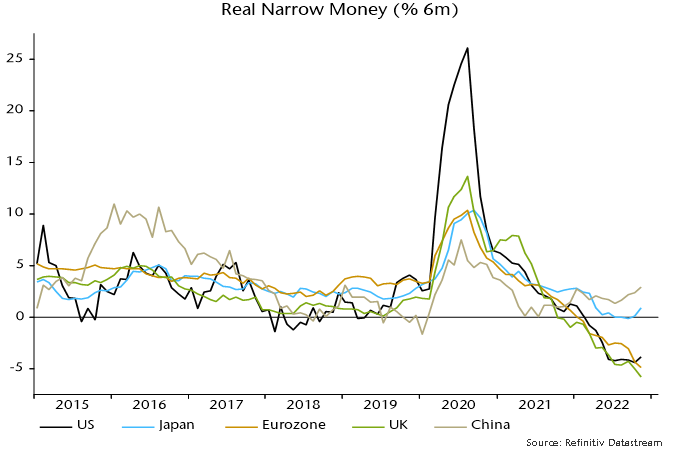

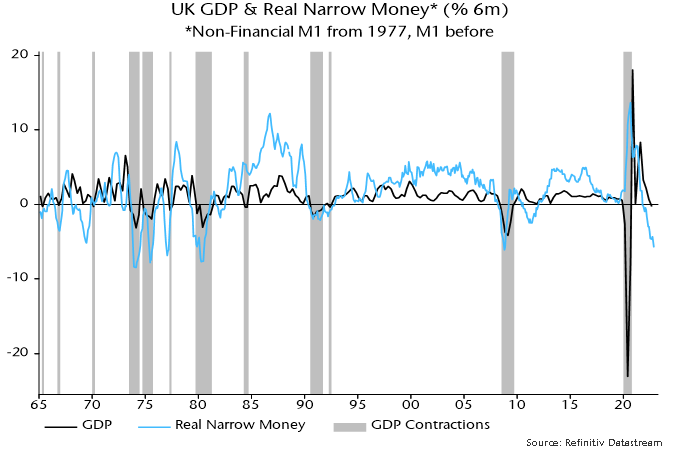

UK real narrow money (i.e. non-financial M1 deflated by consumer prices) contracted by more than comparable US / Eurozone measures in the six months to November – chart 2. The decline is historically extreme and suggests a severe recession – chart 3.

Chart 2

Chart 3

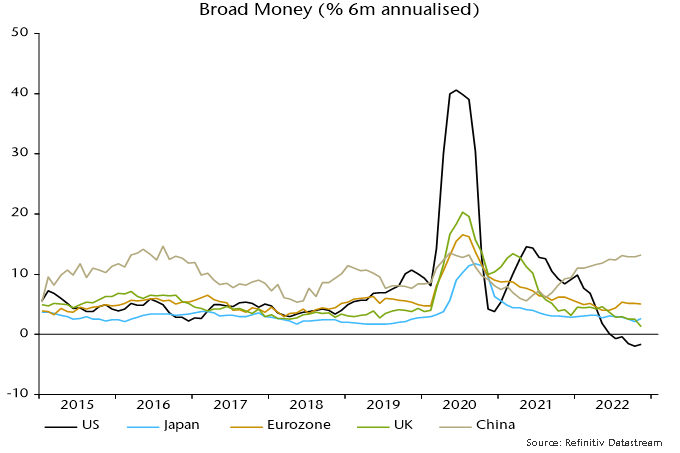

UK nominal broad money (non-financial M4) grew by just 1.3% at an annualised rate in the six months to November – chart 4. The comparable Eurozone measure rose at a 5.0% pace. US broad money contracted but is correcting a much larger increase in 2020-21.

Chart 4

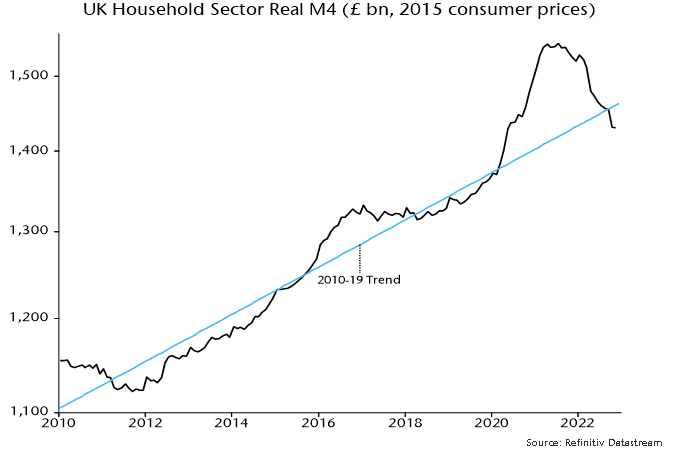

Real broad money holdings of UK households have retraced almost all of the pandemic-related surge, falling to the lowest level since May 2020 – chart 5. Far from “excess” money balances supporting spending, a real money squeeze is now likely to magnify consumption weakness.

Chart 5

Bank of England communications may be becoming less hawkish but the damage has been done. Officials ignored the monetary signal that a 2021-22 inflation spike would reverse with modest policy restraint. The economic consequences of overkill are likely to be at least as bad as in the US / Eurozone.