Are medium-term inflation risks receding?

The surge in global broad money last spring and summer was expected here to result in a major inflation rise in 2021-22. A post in September presented reasoning supporting a forecast of 4-5% average G7 inflation in the two years to Q4 2022.

Recent data appear consistent with this forecast but monetary developments suggest that medium-term inflation risks are diminishing.

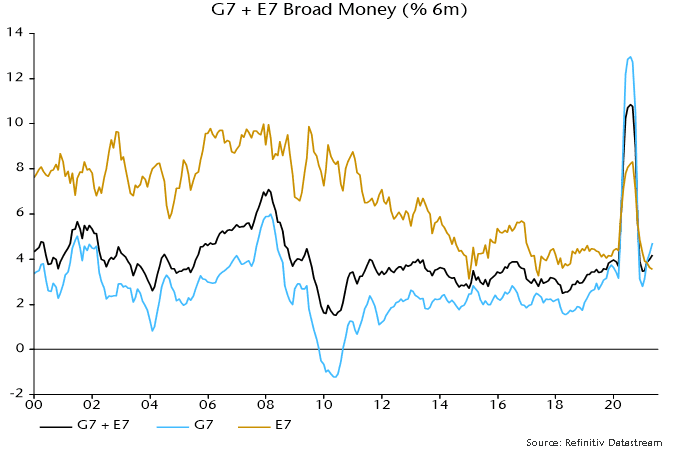

The latter assessment rests on three considerations. First, six-month growth of global (i.e. G7 plus E7) broad money has moved back towards its pre-pandemic pace. Growth was 4.2% in April, or 8.6% at an annualised rate, versus an average increase of 6.6% pa in the 10 years to end-2019.

G7 broad money growth remains elevated relative to the 2010s but E7 growth is at the bottom of its range, with Chinese weakness a key driver – see chart 1.

Chart 1

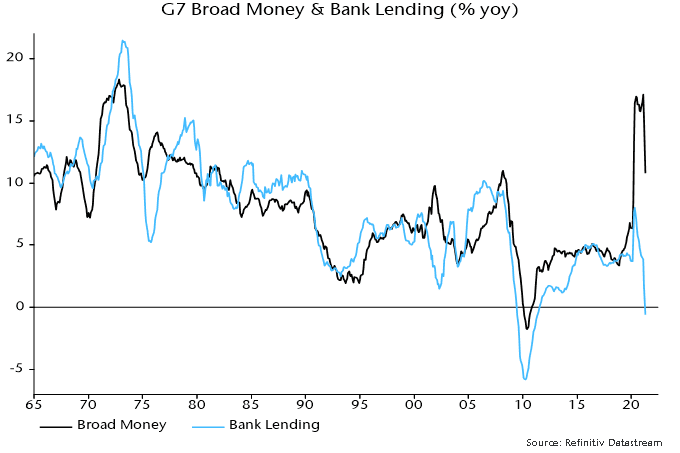

Secondly, G7 bank loans to the private sector have contracted following a brief spurt last spring, contrary to forecasts that government guarantee programmes and central bank incentives would spark a lending boom – chart 2.

Chart 2

Sustained high inflation in the 1970s reflected strong broad money growth driven by bank lending. Last year’s money surge, by contrast, was due to monetary financing of ballooning fiscal deficits and additional QE.

Bank lending is a coincident / lagging economic indicator and is likely to revive as economic activity continues to recover. “Excess” household and corporate liquidity, however, may delay and / or damp a pick-up in credit demand, while the impact on broad money may be neutralised by reduced monetary deficit financing / QE as fiscal positions improve and central banks taper.

A third reason for thinking that monetary inflation risks may have diminished is that a portion of the excess liquidity created last year has been absorbed – at least for the moment – by higher asset prices.

A simplistic quantity theory approach posits that the demand to hold money varies proportionately with nominal GDP. Money, however, is held as a store of wealth as well as to support transactions in goods and services.

Posts here last year described a modified quantity theory model in which nominal GDP and gross wealth have equal roles in driving broad money demand, with an additional impact from real bond yields. This model is consistent with G7 data over the last 50+ years and explains the secular decline in conventionally-defined broad money velocity as a consequence of a rising trend in the ratio of wealth to GDP and a fall in real bond yields.

The current stock of G7 broad money is 20% higher than at end-2019. G7 gross wealth – i.e. the aggregate value of equities, bonds and stocks – is also up by about 20% since then, while real bond yields, on the measure calculated here, are little changed. According to the model, the rise in wealth will have boosted broad money demand by 10%. So markets may have “absorbed” about half of the additional liquidity created since end-2019, implying a smaller excess to be reflected in goods and services prices.

The implication of the model that buoyant asset prices are disinflationary is controversial – it suggests, for example, that inflation prospects would worsen if markets were to crash. That was, however, the experience following the GFC – G7 inflation rose sharply in 2010-11 after the 2008-09 collapse in asset prices. High inflation in the 1970s was associated with weak markets, with equities volatile but directionless and a trend decline in bond prices.

The suggestion that the medium-term inflation outlook has improved at the margin is based on current information and will be revised if any of the inputs discussed above change.

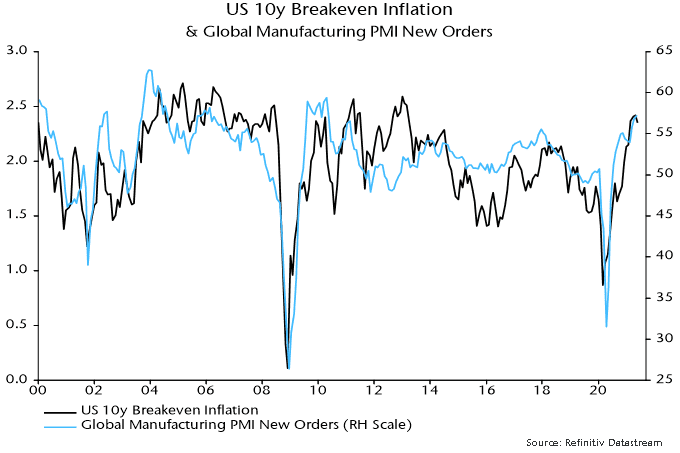

Medium-term inflation expectations in markets are correlated with swings in global industrial momentum – chart 3. The forecast here that the global manufacturing PMI new orders index will decline through late 2021 suggests that expectations will stabilise or moderate near term.

Chart 3

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.