The BoJ’s new Keynesian gamble – third time unlucky?

Will the Bank of Japan’s latest attempt to exit ZIRP prove any more successful than its previous two efforts, in 2000 and 2006?

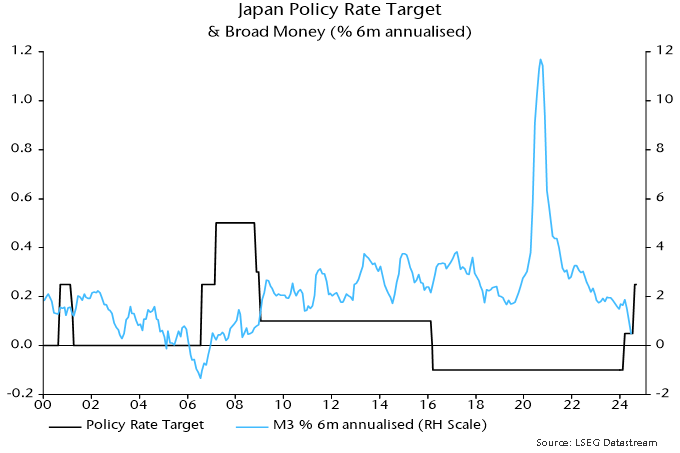

The monetary backdrop is no more promising. The six-month rate of change of broad money M3 was 0.5% annualised in June compared with 1.3% and -1.1% respectively before the August 2000 and July 2006 rate hikes – see chart 1.

Chart 1

Money growth, admittedly, has been depressed by recent record intervention to support the yen. The judgement here is that the authorities have marked out a major low in the currency – see previous post – so f/x sales are likely to slow / end.

A reduced intervention drag, however, will be offset by a contractionary monetary influence from QT. The announced phased reduction in monthly purchases implies that the BoJ’s JGB holdings will fall by about ¥8 trn during H2 2024, equivalent to an annualised 1.0% of M3.

Credit developments are superficially more supportive of policy tightening. The six-month rate of change of commercial banks’ loans and leases was 3.5% annualised in June compared with -1.9% and 2.8% before the 2000 / 2006 hikes.

Bank lending, however, is usually a lagging indicator of economic momentum, suggesting a slowdown ahead in response to recent activity weakness.

The BoJ “will … continue to raise the policy interest rate” if its outlook for economic activity and prices is realised. Headline and core CPI inflation are projected to be close to the 2% target in fiscal years 2025 and 2026 based on the output gap turning positive and a “virtuous cycle between prices and wages continuing to intensify”.

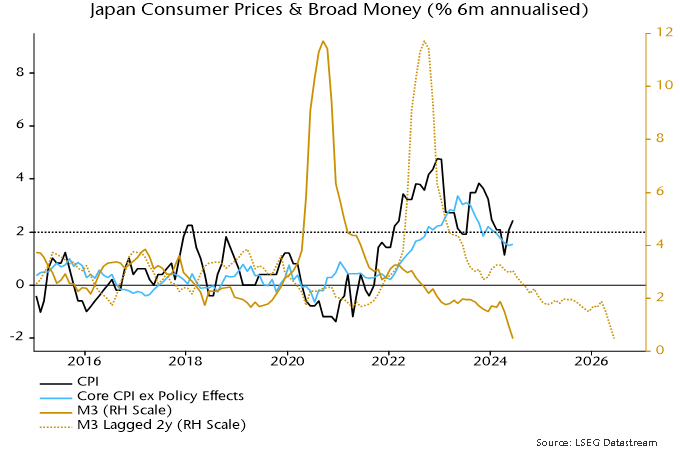

The “monetarist” forecast, by contrast, is that inflation is heading for a big undershoot. Six-month core CPI momentum was 1.5% annualised in June*, with lagged broad money growth suggesting a further decline into 2025 – chart 2.

Chart 2

Coming Japanese inflation experience will be another test of forecasting approaches. Simplistic monetarism has trounced new Keynesian orthodoxy so far this decade. Another win for monetarist simpletons will spell third time unlucky for the BoJ.

*Own estimate adjusting for policy effects and seasonals.